Life insurance with long-term care is a hybrid policy that incorporates the benefits of life insurance and long-term care coverage. The principal advantage of this arrangement is that it ensures the policyholder benefits from the coverage, whether they require long-term care or not. If long-term care is needed, the policy will cover the expenses, usually deducted from the death benefit. If not, the death benefit will go to the policyholder's beneficiaries upon their passing. Combining the two is crucial as it provides a safety net for both the policyholder and their loved ones, ensuring they are covered in any eventuality. As the average life expectancy increases, so does the potential need for long-term care, a factor often not accounted for in standard life insurance policies. At its core, life insurance is a tool for risk management. It provides individuals with the means to safeguard their dependents from financial hardship in the event of their untimely demise. The policyholder pays regular premiums to the insurer, and in return, the insurer commits to paying a predetermined sum to the named beneficiaries when the policyholder dies. There are several types of life insurance, each with its own features, pros, and cons. Term life insurance provides coverage for a specific period, or term (typically 10, 20, or 30 years). If the policyholder dies during this term, the beneficiaries receive the death benefit. It's the most affordable type of life insurance, but it doesn't build cash value. As a type of permanent life insurance, whole life insurance provides lifelong coverage and also includes a cash value component that grows over time. The policyholder can borrow against the cash value or even surrender the policy for the cash. However, these policies are usually more expensive than term life insurance. Universal life insurance is another type of permanent life insurance that provides more flexibility. It allows the policyholder to adjust the premium and death benefit amounts over time. Like whole life insurance, it also has a cash value component. Variable life insurance is similar to universal life insurance but has an investment component. The policyholder can allocate a portion of the premium dollars to a separate account comprised of various investment funds within the insurance company's portfolio. Integrating long-term care into life insurance usually entails the addition of a policy rider, an endorsement that broadens the scope of coverage to include such services. Most permanent life insurance policies, such as whole, universal, and variable life insurance, offer the option to add a long-term care rider. The specifics of how this works can vary. Typically, if the policyholder requires long-term care, a portion of the death benefit is used to cover these costs. For term life insurance, it's quite rare to see these policies offering a long-term care rider. The reason lies in its nature as a temporary form of coverage. Since long-term care benefits are usually associated with later stages of life, they are often beyond the term of such policies. Long-term care refers to a variety of services designed to meet a person's health or personal care needs during a short or long period. These services help people live as independently and safely as possible when they can no longer perform everyday activities on their own. Long-term care can take many forms, from home health care and adult day care to assisted living and nursing homes. The level and type of care will depend on an individual's specific needs. The cost of such services can be substantial and depends on the type and duration of care needed, the location, and the specific service provider. In many cases, these expenses can quickly deplete an individual's savings, hence the importance of incorporating them with life insurance or purchasing separate long-term care insurance. Whether it's whole, universal, or variable life insurance, you'll need a permanent policy to add a long-term care rider. When selecting a policy, you should consider several factors, including the death benefit, premium amounts, cash value component, and the flexibility of the policy. Your choice should reflect your personal financial goals, budget, and risk tolerance. The key considerations include the amount of death benefit that can be used for long-term care, the specific conditions that need to be met for the benefits to be triggered, any waiting periods that apply, and the additional costs for the rider. Some insurers may allow a large portion of the death benefit to be used for long-term care, while others may limit it to a smaller percentage. It is crucial to review these specifics and decide which rider best suits your needs. This typically involves underwriting for both the life insurance and the long-term care components, which may require a medical exam and a comprehensive review of your health history. During this step, be prepared to provide detailed information about your health, lifestyle, and financial situation. It's important to be truthful and thorough in your responses, as any discrepancies can affect your coverage or even lead to policy cancellation. These premiums typically include the cost for both the life insurance policy and the long-term care rider. The frequency and amount of payments can vary, depending on the specifics of your policy. Some policies may allow for flexibility in premium payments, while others require fixed payments. Be sure to understand your payment schedule. You'll need to pay your premiums regularly to keep the policy and rider in effect. This helps alleviate the "use-it-or-lose-it" risk commonly associated with standalone long-term care insurance. With this combined product, if you don't end up needing long-term care, your beneficiaries will receive the full death benefit. If you do require such services, you can tap into the death benefit while still alive to cover these costs. Long-term care can be expensive, and having access to these benefits can save you from exhausting your savings or other financial resources. Moreover, premiums for combined products are often less expensive than buying separate life insurance and long-term care insurance policies. Having one combined policy is easier to manage than two separate ones. You have one premium payment, one policy to review and understand, and one point of contact if you have questions or need to file a claim. If activated, the long-term care rider can substantially reduce the amount left for your beneficiaries upon your death. Depending on the length and cost of care, it's possible that you might exhaust your death benefit entirely. Including this rider can significantly increase your insurance premiums. It's important to consider whether the additional cost fits into your budget and financial plan. Because the insurer is taking on more risk by providing two types of coverage, they may require a more detailed medical exam and health history. Long-term care often becomes a necessity as you age or when you have chronic health conditions. If you're young and healthy, the immediate need for this combined coverage might not seem evident. However, planning for potential future needs is essential. Moreover, buying policies when you're younger and healthier can also mean lower premiums. Genetics can play a role in your health as you age. If your family has a history of chronic illnesses that necessitate long-term care (like Alzheimer's, Parkinson's, or stroke), you might have a higher risk and could benefit from combined coverage. Consider your current financial situation and future income. Can you afford the premiums for a combined policy? It's crucial to balance the cost with the potential benefits. On the other hand, if you can comfortably cover potential long-term care costs out of pocket, you might not need the additional coverage. If your goal is to leave a substantial financial legacy for your heirs, remember that utilizing the death benefit for long-term care expenses could significantly reduce the amount your beneficiaries receive. You'll need to weigh the importance of providing for long-term care costs versus preserving the full death benefit for your heirs. Lastly, consider the emotional aspect. Having a policy that covers both life and long-term care insurance can offer peace of mind, knowing that you and your loved ones are protected financially, regardless of what the future brings. Standalone policies can offer broader coverage and more significant benefits for long-term care compared to a rider on a life insurance policy. If you anticipate needing extensive long-term care, a standalone policy might offer more robust coverage. However, it's important to note that these policies often come with the "use-it-or-lose-it" risk. If you never need long-term care, all the premiums you've paid into the policy will not benefit you or your heirs. Also, the cost of standalone long-term care insurance can be high and increases as you age. It means saving enough to pay for any potential long-term care costs out-of-pocket. If you have substantial savings or investments, this could be a viable strategy. It allows you to retain control over your funds, and if you never need long-term care, those assets remain part of your estate. The major risk with self-insuring is the potential for long-term care costs to outpace your savings. The cost of long-term care can be high and increase over time, and there's always the risk of needing more care than anticipated. Medicaid, a joint federal and state program, can help cover long-term care costs for individuals with limited income and assets. Unlike Medicare, which primarily covers medical care for those aged 65 and over, Medicaid can pay for a variety of long-term care services, including both nursing home care and home and community-based services. However, Medicaid is a needs-based program with strict income and asset requirements. Many people have to spend down their assets to qualify, and not all services are covered in all states. There can also be long waiting lists for certain services. Life insurance with long-term care is a valuable hybrid policy that combines the benefits of life insurance and long-term care coverage. This combination addresses the often overlooked need for long-term care as life expectancy continues to rise, providing a well-rounded solution within a single insurance policy. While this hybrid policy offers advantages like guaranteed payouts, financial savings, and simplicity, it also posts drawbacks, such as potentially reduced death benefits, additional costs for the rider, and a stringent underwriting process. Therefore, individuals should thoroughly evaluate their health, age, family medical history, financial situation, estate planning objectives, and the peace of mind that comprehensive coverage can provide. Exploring alternative options, such as standalone long-term care insurance, self-insuring, or availing government programs is also advisable. Consult a financial advisor or insurance professional. They can provide a detailed analysis of your situation and help determine whether life insurance with long-term care is the right choice for you.Life Insurance With Long-Term Care: An Overview

Understanding Life Insurance

Definition and Types

Term Life Insurance

Whole Life Insurance

Universal Life Insurance

Variable Life Insurance

How These Insurance Types Can Incorporate Long-Term Care

Exploring Long-Term Care

How to Combine Life Insurance and Long-Term Care

Step 1: Choose a Permanent Life Insurance Policy

Step 2: Understand the Long Term Care Rider Options

Step 3: Apply for the Policy and Rider

Step 4: Pay Your Premiums

Pros and Cons of Life Insurance With Long-Term Care

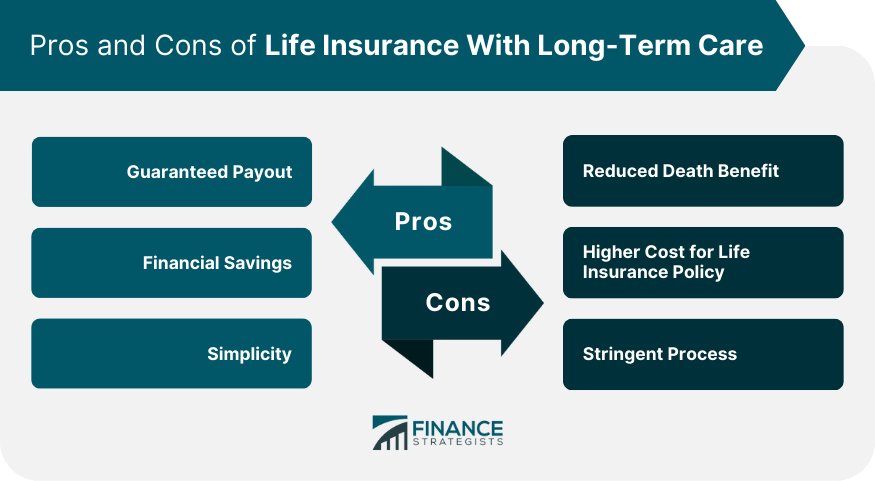

Pros

Guaranteed Payout

Financial Savings

Simplicity

Cons

Reduced Death Benefit

Higher Cost for Life Insurance Policy

Stringent Process

Is Life Insurance With Long-Term Care Right for You?

Health and Age

Family History

Financial Situation

Estate Planning

Peace of Mind

Alternatives to Life Insurance With Long-Term Care

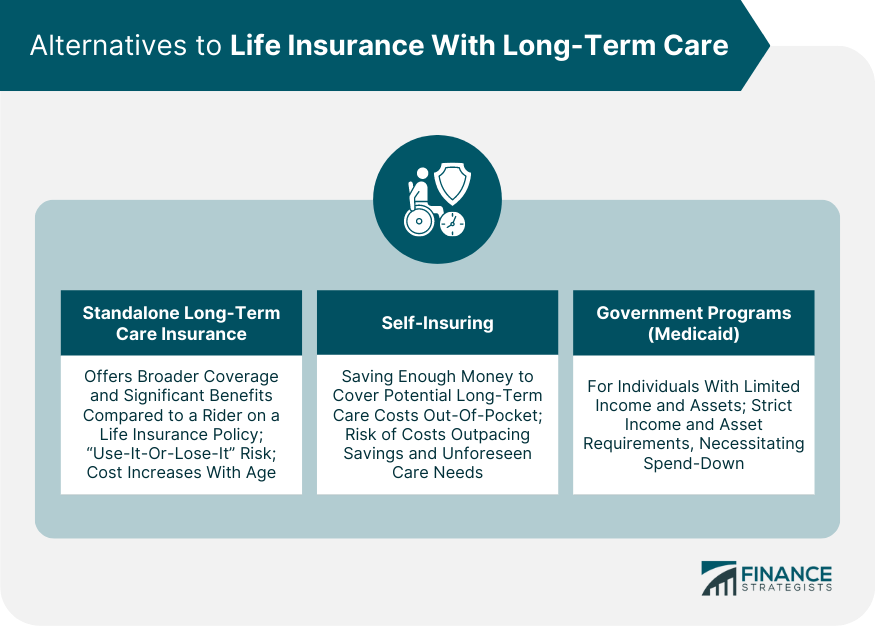

Standalone Long-Term Care Insurance

Self-Insuring

Government Programs Like Medicaid

Final Thoughts

Life Insurance With Long-Term Care FAQs

Life insurance with long-term care is a hybrid insurance policy that combines the death benefit of a traditional life insurance policy with the practical benefits of long-term care insurance. If you require long-term care, this policy allows you to access a portion of your death benefit while still alive to cover these costs. If you don't end up needing long-term care, the full death benefit is paid out to your beneficiaries upon your death.

This type of policy works by allowing you to tap into your death benefit for long-term care costs if needed. The amount used for long-term care is subtracted from the death benefit. Any remaining death benefit is then passed on to your beneficiaries when you die. If you don't use any of the death benefit for long-term care, then the full amount goes to your beneficiaries.

Life insurance with long-term care can be a good option for individuals who want the security of life insurance and are concerned about the potential need for long-term care in the future. This might include individuals with a family history of chronic illnesses that require long-term care, those who want to protect their assets from the high cost of long-term care, or those who want to ensure a guaranteed payout from their insurance policy.

Yes, the premiums for life insurance with long-term care are typically more expensive than for a standard life insurance policy. This is because the insurer is taking on additional risk by providing coverage for potential long-term care costs. However, this combined policy can often be less expensive than buying separate life insurance and long-term care policies.

Getting life insurance with long-term care if you have pre-existing conditions can be more challenging and potentially more expensive. However, it's not necessarily impossible. The underwriting process will consider your overall health, including any pre-existing conditions. Some insurers may still offer you coverage, although at a higher premium. It's crucial to shop around and speak with a knowledgeable insurance professional to explore your options.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.