Life insurance premiums are regular payments that policyholders make to their life insurance companies to maintain coverage. These premiums are typically based on factors like the insured's age, health, lifestyle, and the amount of the death benefit. The purpose of these premiums is to provide a financial safety net for the policyholder's dependents or beneficiaries in case of the insured's untimely demise. Life insurance premiums have a significant impact on policyholders as they represent a recurring cost that needs to be managed carefully. In the context of personal financial planning, they play a critical role in providing financial security for loved ones, covering costs like funeral expenses, debts, or providing a living allowance. However, while these premiums can represent a considerable expenditure, it's important to remember that they are generally not tax-deductible, except for certain specific circumstances. In most cases, you cannot deduct life insurance premiums on your taxes. The Internal Revenue Service (IRS) generally views life insurance as a personal expense, and thus it's not typically tax-deductible from an individual's gross income. However, there are a few exceptions. For instance, if you're a business owner and you have a life insurance policy on a key employee for business purposes, you may be able to deduct the premiums as a business expense. But the business cannot be a direct or indirect beneficiary of the policy. Additionally, if you're legally required to maintain life insurance as part of a divorce decree or alimony agreement, with the former spouse as the beneficiary, the premiums might be deductible. If a life insurance policy is irrevocably donated to a qualifying non-profit organization or a charity is named as the policy's irrevocable beneficiary, then the premiums paid might be considered charitable contributions and thus could be tax-deductible. Remember, these are specific cases, and tax laws can be complex. Therefore, it's always best to consult with a tax professional to understand what applies to your situation. Despite this overarching rule, there are specific instances where life insurance premiums may be deductible. If a business entity owns a life insurance policy on a key employee for business purposes, the premiums may be deductible as a business expense. However, there are strict regulations regarding when these circumstances apply, and the business cannot be a direct or indirect beneficiary of the policy. In unique scenarios where an individual is legally required to maintain a life insurance policy as part of a divorce decree or alimony agreement, with the former spouse as the beneficiary, the premiums may potentially be deductible. This rule, however, is subject to change, and it's crucial to seek professional advice before claiming such deductions. If a life insurance policy is irrevocably donated to a qualifying non-profit organization, or if a charity is named as the policy's irrevocable beneficiary, then the premiums paid might be considered charitable contributions and thus could be deductible. Special Cases: Accrued Interest on Life Insurance Loans: In cases where a policyholder borrows from their life insurance policy, the interest accrued on the loan may be deductible, given certain specific circumstances. Misconceptions surrounding life insurance and taxes often lead to confusion. It's essential to clarify these misconceptions for better understanding. Generally, beneficiaries do not have to pay income taxes on the death benefits they receive from a life insurance policy. The IRS considers these payments as reimbursement for a personal loss, thus generally tax-free. However, the death benefit could potentially be subject to estate taxes if the deceased's estate exceeds the federal estate tax exemption. For permanent life insurance policies (like whole or universal life), the cash value component grows over time and is not subject to income taxes while it remains within the policy. It's only when the policyholder surrenders the policy or otherwise withdraws more than their basis in the policy that taxes may be due. Loans taken from a life insurance policy's cash value are typically not considered taxable income, provided the policy stays in force until the policyholder's death. While life insurance premiums themselves aren't usually tax-deductible, several life insurance products come with tax advantages, serving as efficient tax planning tools. Whole Life Insurance: With this policy, the cash value grows on a tax-deferred basis, which means the policyholder won't pay taxes on any earnings as long as the policy remains in force. Universal Life Insurance: Like whole life insurance, universal life insurance also offers a cash value component that grows tax-deferred. Variable Life Insurance: This policy allows the policyholder to invest the cash value into subaccounts (much like mutual funds), with any growth or earnings also generally accumulating on a tax-deferred basis. Due to the intricacies of tax law and insurance, professional advice is paramount to maximize the benefits and ensure compliance with all rules and regulations. Tax laws are complex and ever-changing. To navigate these complexities, it's recommended to consult a tax advisor or professional who's familiar with both life insurance and taxation. Life insurance can play a significant role in estate planning. However, if not correctly structured, the death benefit may be subject to estate taxes. A knowledgeable estate planning attorney or financial advisor can provide guidance. Regular policy reviews can help identify any changes in the law that might affect tax liability or policy performance. Life insurance serves as an essential financial safety net, albeit premiums for these policies generally aren't tax-deductible. However, exceptions exist, such as in the cases of business-owned policies, divorce or alimony agreements, and donations to charities. Life insurance products, like whole, universal, and variable life insurance, can also offer tax benefits due to their cash value component. Beneficiaries typically don't have to pay income tax on the death benefits they receive. The rules surrounding taxes and life insurance are complex and multifaceted, making it essential to understand them for sound financial planning. Regular reviews of life insurance policies and consulting with tax professionals can help navigate this intricate landscape. Therefore, it's always recommended to seek professional advice to maximize the benefits of life insurance and to ensure compliance with all tax rules and regulations.Life Insurance Premiums Overview

Can You Deduct Life Insurance Premiums on Taxes?

Life Insurance Premiums Exceptions and Possible Deductions

Business-Related Life Insurance Premiums

Situations of Alimony or Divorce Settlement

Deductibility of Premiums for Life Insurance as a Charitable Gift

Clarifying Common Misconceptions

Life Insurance, Death, Benefits, and Taxes

Cash Value Growth and Taxes

Life Insurance Loans and Taxes

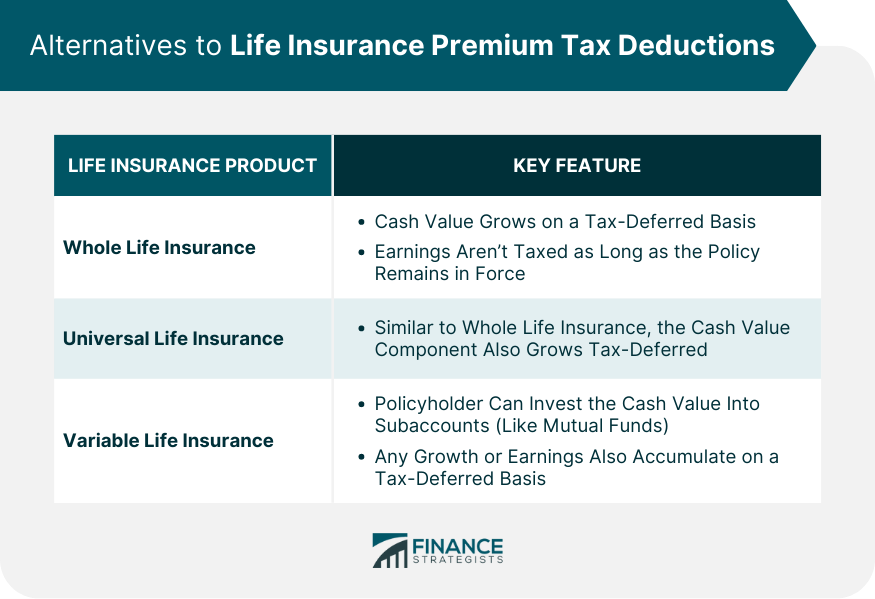

Alternatives to Life Insurance Premium Tax Deductions

Tax Planning and Life Insurance: Best Practices

Consulting With a Tax Professional

Considerations for Life Insurance as Part of an Estate Plan

Regularly Reviewing Life Insurance Policies

The Bottom Line

Can You Deduct Life Insurance Premiums on Taxes? FAQs

No, you generally cannot deduct life insurance premiums as a personal expense on your taxes. The IRS considers life insurance as a personal benefit, and premiums are not typically tax-deductible from an individual's gross income.

Yes, but only under specific circumstances. If a business owns a life insurance policy on a key employee for valid business purposes, the premiums may be deductible as a business expense. However, the business cannot be a direct or indirect beneficiary of the policy.

Potentially, if an individual is legally mandated to maintain a life insurance policy as part of a divorce decree or alimony agreement, with the former spouse as the beneficiary, the premiums may be deductible. However, this rule is subject to change, so it's crucial to consult with a tax professional before claiming such deductions.

Yes, if you irrevocably donate a life insurance policy to a qualifying non-profit organization, or if a charity is named as the policy's irrevocable beneficiary, then the premiums paid might be considered charitable contributions and could be tax-deductible.

Yes, while life insurance premiums typically aren't tax-deductible, several life insurance products come with tax advantages. For instance, whole life, universal life, and variable life insurance policies offer a cash value component that grows on a tax-deferred basis. Also, death benefits received from a life insurance policy are typically not subject to income taxes.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.