An annuity is a financial contract between an individual and an insurance company, designed to provide a regular income stream in exchange for a lump sum or series of payments. This contract is often used as a strategy for securing income during retirement. Annuities serve as a safety net that reduces the risk of outliving one's savings. Moreover, the predictable income can offer peace of mind, helping retirees budget effectively without worrying about fluctuations in the financial markets. Annuities offer a plethora of benefits, including tax-deferred growth, guaranteed income for life, and the potential for a death benefit to beneficiaries. Additionally, they can be customized to meet individual needs, such as increasing payouts to account for inflation. The terms of a fixed annuity contract guarantee a specified interest rate over a defined period. This type of annuity is relatively low risk because the investor is assured of a fixed return regardless of market fluctuations. The payout can be for a certain period or last for the lifetime of the annuitant, offering a predictable and secure source of income. Fixed annuities are particularly suitable for risk-averse individuals who prioritize capital preservation and a stable income over potential higher returns. While the minimum initial investment required for a fixed annuity can vary significantly based on the insurance company's policies, it generally starts from as low as $2,500. It can go up to $10,000 or more. These annuities allow investors to distribute their money across various investment options like mutual funds. This means the return from a variable annuity depends on the performance of these underlying investments. While variable annuities can potentially provide higher returns, they also come with higher risk. The return is not guaranteed, and the value of the annuity contract can rise or fall with the success of the chosen investments. These annuities might be a good fit for individuals with higher risk tolerance and a longer time horizon, which allows more time to recover from possible market downturns. Variable annuities usually necessitate a larger initial investment, typically starting around $5,000 to $10,000, depending on the provider. This larger initial outlay might be offset by potentially higher returns over the long term, provided the chosen investments perform well. Indexed annuities combine elements of both fixed and variable annuities. The return of an indexed annuity is tied to the performance of a specific market index, such as the S&P 500. Unlike a variable annuity, an indexed annuity usually provides a minimum guaranteed return, protecting the investor from a total loss. However, gains are typically capped, meaning investors might not fully benefit from strong market performance. This structure can be appealing to individuals who seek market-linked growth potential but with a level of downside protection. Indexed annuities usually have initial investment requirements similar to variable annuities, generally starting at around $5,000 to $10,000 or more. Nevertheless, this can vary between insurance companies and specific products, so potential investors should thoroughly research or consult with a financial advisor before making a decision. The timing of when payouts begin distinguishes immediate and deferred annuities. With an immediate annuity, the annuitant receives income shortly after making the initial investment, typically within a year. This can be a good option for those already in retirement who need an income stream immediately. On the other hand, a deferred annuity delays income payments until a future date chosen by the annuitant, potentially allowing for a larger accumulation of value. This could be suitable for individuals still in their earning phase, looking to build a large nest egg for retirement. The initial investment for immediate annuities can start at $25,000, while deferred annuities can be started with a smaller initial investment as there's more time for the investment to grow before payouts begin. Age plays a pivotal role in determining the initial investment in annuities. This is primarily because the annuity payments you receive, and the period over which you receive them, are closely related to your life expectancy. Younger investors have the advantage of time, which allows for a longer accumulation period. In such cases, a smaller initial investment might suffice because the amount has more time to grow before payouts begin. The time between the initial investment and when you start receiving payouts also influences the amount needed to start an annuity. If you desire to start receiving payouts soon after your investment, you will need a larger upfront amount. However, if you can afford to wait for a longer duration, your money has more time to grow, reducing the initial amount you need to put in. The higher the desired monthly income, the larger will be the initial amount needed to ensure that the annuity can provide this level of income. It's crucial to have a realistic understanding of your future income needs to accurately determine the initial investment for the annuity. The impact of market interest rates on the initial investment for an annuity is substantial. When interest rates are high, insurance companies can generate more income from their general investment funds. This means you'd need to put less money into the annuity to receive a certain amount of future income. Conversely, in a low-interest rate environment, you may need a larger initial investment to secure the same level of income. Insurance companies often impose specific terms and conditions on their annuity contracts. These include surrender charges (penalties for withdrawing funds early), fees, and minimum investment requirements. These can influence the initial amount needed to establish an annuity. For instance, if the company has high surrender charges, it might offer more attractive terms such as a higher interest rate or lower initial investment. Alternatively, if the company has a high minimum investment requirement, you will need a larger sum to purchase the annuity. Understanding these terms is crucial in choosing the right annuity contract and determining the initial investment. The sooner you start investing, the more time your money has to grow. Starting early allows you to take advantage of compounding interest, reducing the initial investment needed to achieve your desired retirement income. If possible, consider lowering your desired monthly income from the annuity. A smaller monthly payout results in a smaller required initial investment. This requires careful planning to ensure the lower income will still meet your needs in retirement. Some annuities allow for contributions over time rather than a large lump sum upfront. Regular contributions can make an annuity more attainable for those with limited initial investment funds. Different insurance companies have different terms, conditions, and fees. Research various options and choose an insurance company that offers favorable terms and a lower minimum initial investment requirement. Establishing good saving habits and a disciplined budget can help you accumulate the funds needed to start an annuity. Even small regular contributions can add up over time due to compound interest. Instead of putting all your money into an annuity, consider diversifying your investment portfolio. Investments in stocks, bonds, and other assets could potentially yield higher returns, reducing the amount you need to invest in your annuity. Some employers offer annuity options as part of their retirement plans, sometimes matching a portion of employee contributions. These can lower the amount you need to contribute, thereby reducing your initial investment. Financial advisors can provide personalized advice based on your unique financial situation and goals. They can help you navigate the world of annuities, tailor strategies, and create a plan to meet your retirement income goals. Annuities can be a valuable financial tool for individuals seeking a secure and predictable income stream during retirement. Different types of annuities have varying initial investment requirements, with fixed annuities typically starting from as low as $2,500 and variable and indexed annuities requiring a larger initial investment, usually starting around $5,000 or more. Choosing between immediate and deferred annuities depends on an individual's specific retirement needs, with deferred annuities often requiring a smaller initial investment. Immediate annuities can start at $25,000. Other factors include investor age, duration until payout, desired monthly income, current market interest rates, and insurance company terms and conditions. Minimizing the initial investment amount can be achieved by starting early, lowering desired monthly income, contributing regularly, shopping around, saving and budgeting, diversifying investments, exploring employer-sponsored annuities, and seeking advice from a financial advisor.Overview of Annuities

Annuity Types and Their Initial Investment Requirements

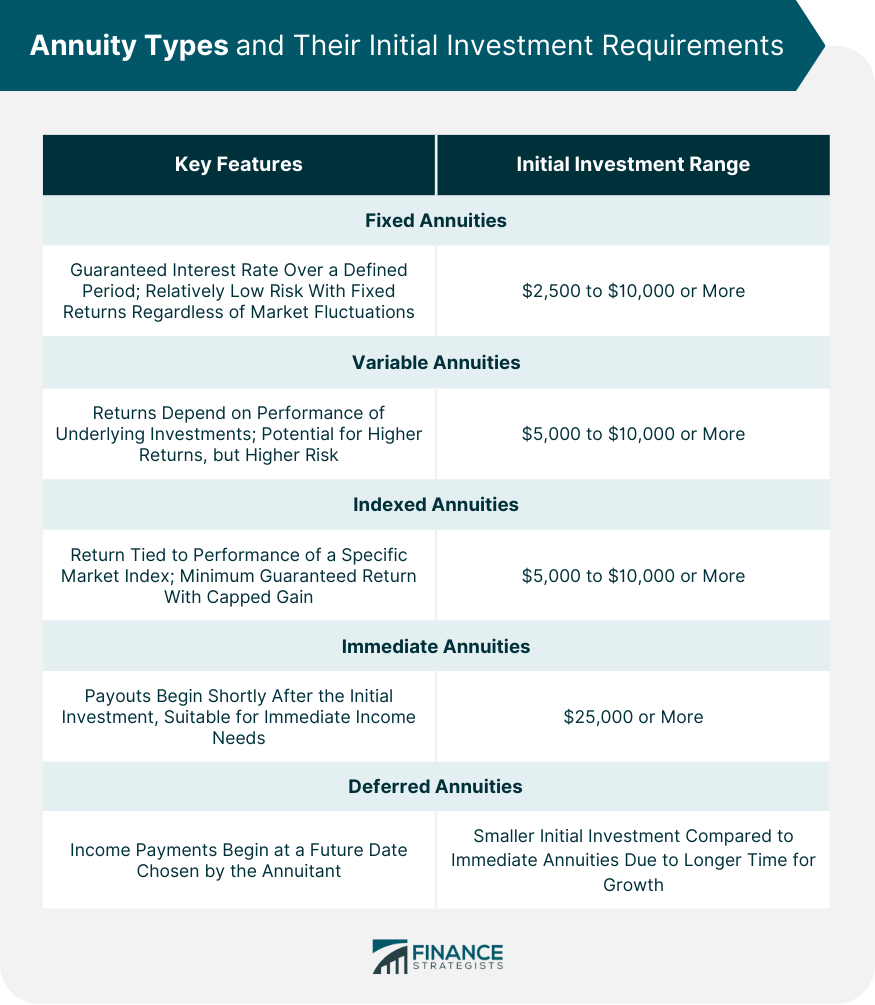

Fixed Annuities

Variable Annuities

Indexed Annuities

Immediate vs Deferred Annuities

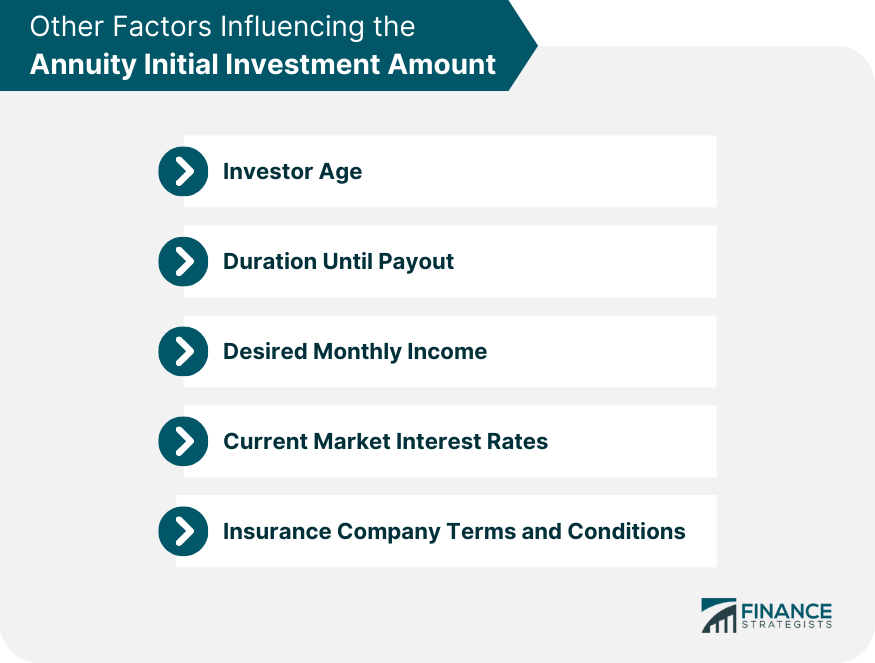

Other Factors Influencing the Annuity Initial Investment Amount

Investor Age

Duration Until Payout

Desired Monthly Income

Current Market Interest Rates

Insurance Company Terms and Conditions

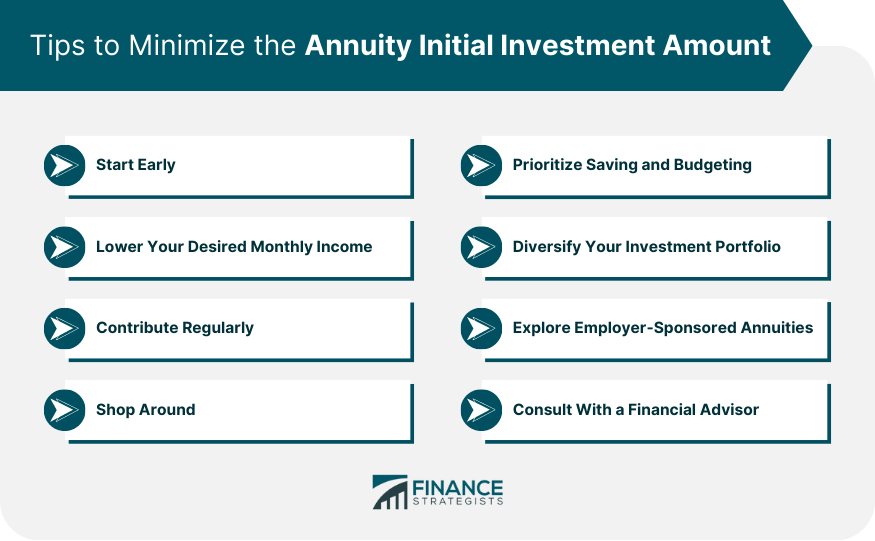

Tips to Minimize the Annuity Initial Investment Amount

Start Early

Lower Your Desired Monthly Income

Contribute Regularly

Shop Around

Prioritize Saving and Budgeting

Diversify Your Investment Portfolio

Explore Employer-Sponsored Annuities

Consult With a Financial Advisor

Final Thoughts

How Much Money Do You Need to Start an Annuity? FAQs

The minimum initial investment required for an annuity can vary significantly based on the insurance company and the type of annuity. For a fixed annuity, it often starts as low as $2,500 and can go up to $10,000 or more. For variable or indexed annuities, the initial investment typically starts around $5,000 to $10,000.

Yes, it's possible to start an annuity with a relatively small amount of money, particularly in the case of fixed annuities which often have lower initial investment requirements. However, the desired monthly income you wish to receive from your annuity in retirement will determine the size of the necessary initial investment.

Yes, market interest rates play a significant role in determining the initial investment needed for an annuity. When interest rates are high, insurance companies can generate more income from their general investment funds. As a result, you'd need to invest less money to receive a specific amount of future income. However, in a low-interest-rate environment, a larger initial investment may be necessary to secure the same level of income.

Your age can significantly influence the initial investment required for an annuity. Younger investors have a longer time horizon for their money to grow, which means they may need a smaller initial investment. On the other hand, if you are older and want to start receiving payouts soon, you will likely need a larger upfront amount.

Yes, there are several strategies to minimize the initial investment for an annuity. Starting to invest early, lowering your desired monthly income, contributing regularly over time, researching and comparing terms from different insurance companies, and leveraging employer-sponsored annuity options can all help reduce the initial investment required.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.