An annuitant is an individual who is entitled to receive benefits from an annuity, which is a financial product issued by an insurance company. The primary purpose of an annuitant is to enjoy a regular stream of income from an annuity. By being an annuitant, individuals can secure a stable and predictable source of funds for their retirement or financial goals. Additionally, annuitants may benefit from potential tax advantages and the ability to customize their annuity to meet their specific needs, such as lifetime income or survivorship options. Typically, the annuitant is the person who owns the annuity contract, although this is not always the case. The annuity payments are determined by several factors, including the annuitant’s age, life expectancy, and the terms of the annuity contract. The primary annuitant, typically the contract owner, is fundamental to the structure of the annuity. It is this individual's life expectancy that shapes the calculation of annuity payments. As the main recipient of the annuity income, their lifespan significantly influences the distribution phase. The primary annuitant's age and life expectancy can affect the payout rate, ultimately determining the regular income during their retirement years. A joint annuitant, often a spouse or life partner, offers an additional layer of financial security. Should the primary annuitant pass away, the joint annuitant steps in to continue receiving the annuity income. This continuation of benefits offers a financial safety net, ensuring a steady flow of income even after the primary annuitant's demise. This arrangement can contribute to a more secure financial future for surviving spouses or partners. The role of the contingent annuitant becomes active in scenarios where both the primary and joint annuitants pass away before the exhaustion of benefits. This individual, acting as a secondary backup, steps in to receive the remaining annuity income. This arrangement adds another level of security, ensuring that the benefits of the annuity extend beyond the lives of the primary and joint annuitants. Involving a revocable annuitant introduces flexibility into the annuity contract. In this case, the contract owner reserves the right to change the annuitant. This feature can be particularly beneficial when the owner's circumstances or intentions evolve over time, such as changes in family dynamics or estate planning objectives. On the other hand, an irrevocable annuitant provides certainty and permanence. Once the annuity contract is in place, the identity of the irrevocable annuitant cannot be altered. This arrangement is beneficial when the owner wishes to guarantee a specific individual will benefit from the annuity, ensuring the income stream remains directed as initially intended. This can be particularly important in cases involving specific long-term financial commitments or legacy planning. Annuity payments are often part tax-free return of investment and part taxable income. The taxable portion is considered ordinary income and is taxed at the annuitant’s regular income tax rate. One of the key benefits of annuities is that they offer tax-deferred growth. This means that the money within the annuity can grow without being taxed until it is withdrawn. Unlike other tax-deferred retirement accounts, annuities do not have required minimum distributions (RMDs). This allows the annuitant to defer taking income from the annuity, allowing the investment to grow tax-deferred for a longer period. Upon the death of an annuitant, the value of the annuity may be included in the annuitant's estate for estate tax purposes. However, the specific tax implications can vary based on the type of annuity and the annuitant’s overall estate. Annuity payments are backed by the financial strength of the insurance company that issues them. Therefore, there is a risk that the company could default. This is known as credit risk. Inflation risk is the risk that the purchasing power of annuity payments will decrease over time due to inflation. Interest rate risk refers to the potential impact of interest rate changes on the value of an annuity. When interest rates rise, the value of a fixed annuity may decrease. Variable annuities expose the annuitant to market risk because the payments are tied to the performance of an investment portfolio. Longevity risk is the possibility that the annuitant will outlive the income from the annuity. This is a significant risk, especially for individuals who do not have other sources of retirement income. Choosing the right annuity begins with a clear understanding of the annuitant’s financial goals and risk tolerance. This involves considering factors such as the need for income, desire for wealth preservation, and comfort with market fluctuations. Different annuity products offer different features, such as varying rates of return, optional riders for additional protection, and different payout options. Comparing these features can help the annuitant choose an annuity that best fits their needs. Annuities can come with various fees and expenses, such as surrender charges, management fees, and insurance charges. Understanding these costs is crucial in making an informed decision. Given the credit risk associated with annuities, it’s important to review the ratings and financial strength of the insurance companies offering these products. Companies with higher ratings are generally considered more reliable and less likely to default on their obligations. Many annuities come with certain provisions and guarantees, such as death benefits or guaranteed minimum income benefits. These can provide added security for the annuitant. In the event an insurance company defaults, state guaranty associations can provide a level of protection to annuitants. Each state has its own guaranty association and coverage limits. Annuities are regulated by state insurance departments, and annuitants are protected by various consumer protection laws. These regulations aim to ensure that insurance companies operate in a financially sound and ethical manner. An annuitant is an integral component of the annuity contract, with various types, such as primary, joint, contingent, revocable, and irrevocable. Each kind has unique implications on the flow of annuity income, thereby influencing financial planning strategies. Moreover, understanding the risks associated with becoming an annuitant is essential. These considerations encompass credit risk, inflation, interest rate fluctuations, market volatility, and longevity risk. By recognizing these factors, prospective annuitants can make informed decisions about whether an annuity aligns with their financial goals and risk tolerance. Therefore, knowledge of the annuitant role, its many forms, and the associated considerations is crucial for anyone contemplating an annuity investment.Definition of Annuitant

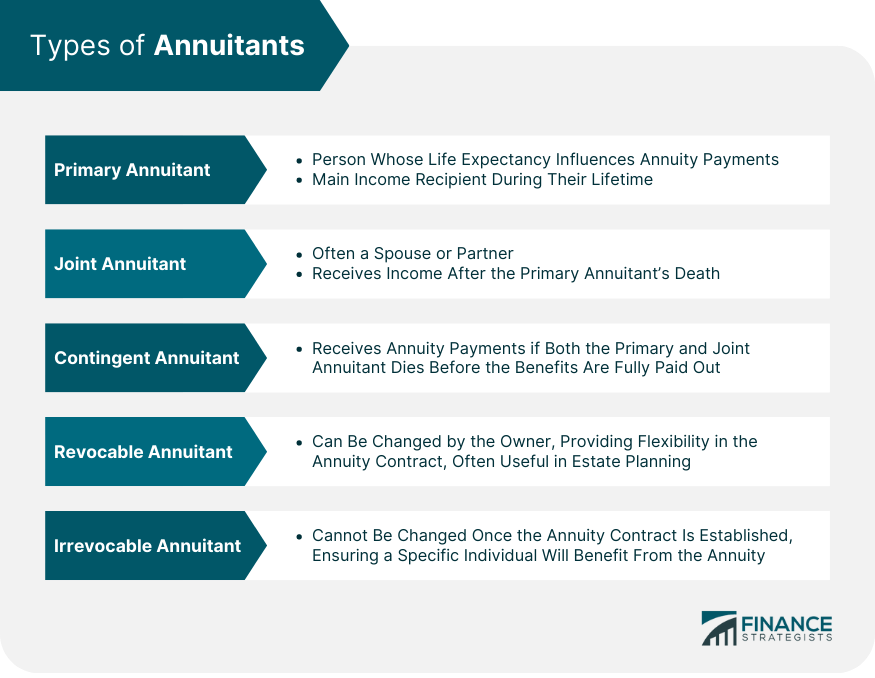

Types of Annuitants

Primary Annuitant

Joint Annuitant

Contingent Annuitant

Revocable Annuitant

Irrevocable Annuitant

Tax Implications for Annuitants

Tax Treatment of Annuity Income

Tax-Deferred Growth in Annuities

Required Minimum Distributions (RMDs)

Estate Tax Considerations for Annuitants

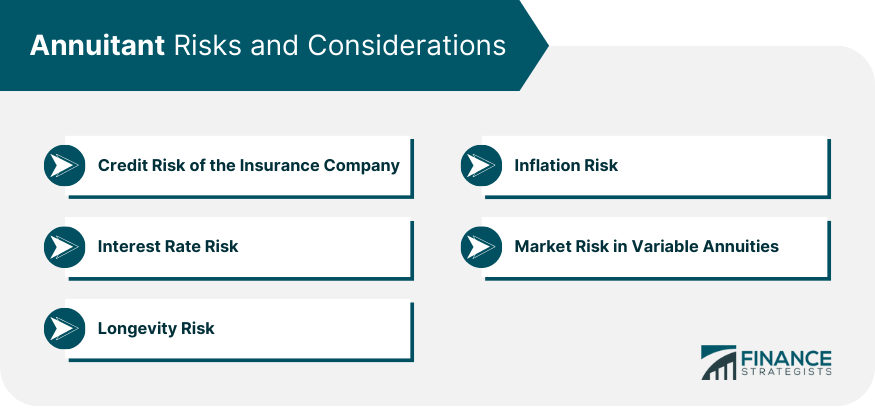

Annuitant Risks and Considerations

Credit Risk of the Insurance Company

Inflation Risk

Interest Rate Risk

Market Risk in Variable Annuities

Longevity Risk

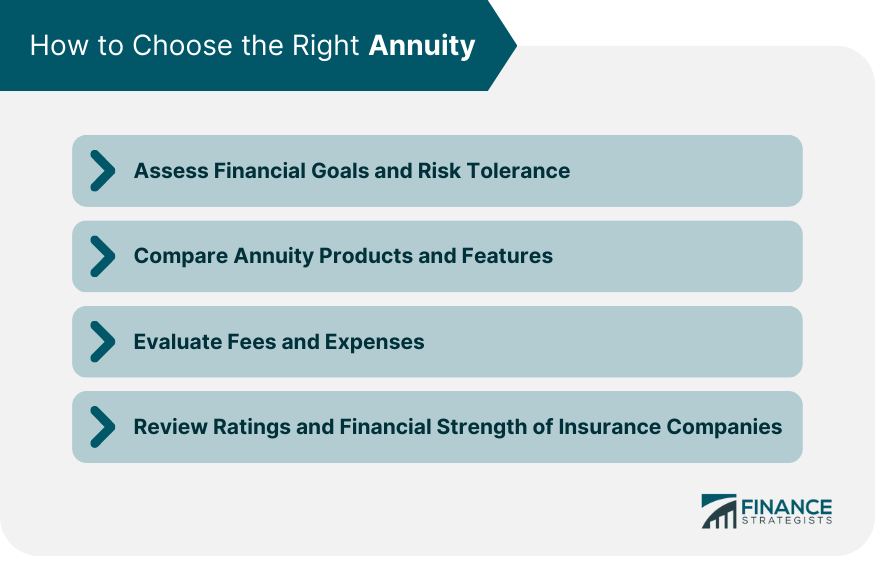

Choosing the Right Annuity

Assessing Financial Goals and Risk Tolerance

Comparing Annuity Products and Features

Evaluating Fees and Expenses

Reviewing Ratings and Financial Strength of Insurance Companies

Annuitant Rights and Protections

Contract Provisions and Guarantees

State Guaranty Associations

Regulatory Oversight and Consumer Protection

Conclusion

Annuitant FAQs

An annuitant is an individual who is entitled to receive benefits from an annuity.

There are several types of annuitants, including primary, joint, contingent, revocable, and irrevocable annuitants.

An annuitant should consider credit risk, inflation risk, interest rate risk, market risk, and longevity risk.

An annuitant should assess their financial goals and risk tolerance, compare annuity products and features, evaluate fees and expenses, and review the financial strength of insurance companies.

An annuitant has various rights and protections, including contract provisions and guarantees, protection from state guaranty associations, and regulatory oversight and consumer protections.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.