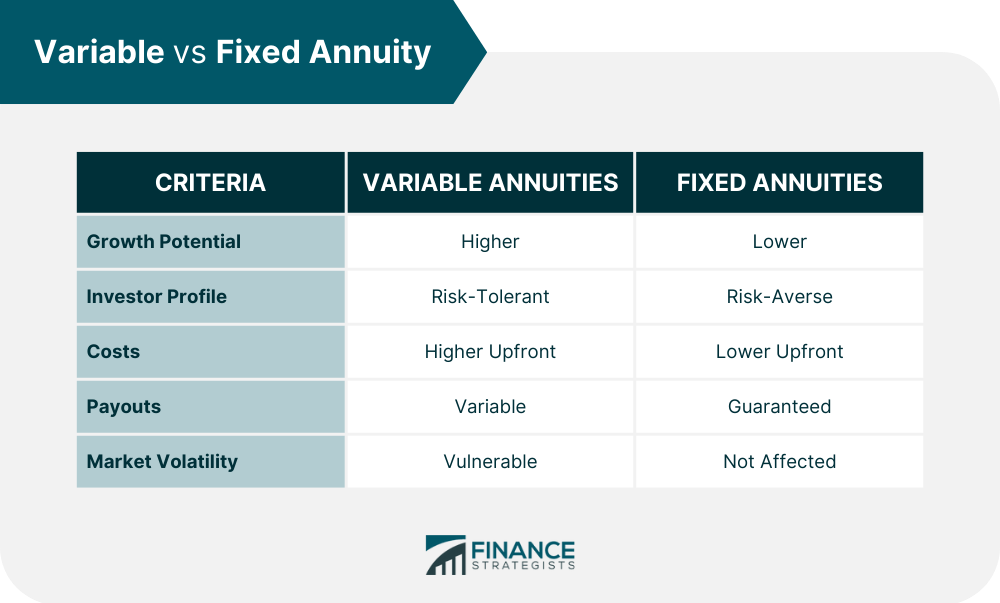

Annuities are an insurance product used as an income stream during retirement. They typically involve an accumulation phase, when you make a lump sum or series of payments to an insurance company, and a distribution phase, when you receive income payouts over time. Fixed annuities guarantee a set rate of return. In contrast, variable annuities allow investors to put their money into different underlying portfolios or subaccounts that may yield higher returns at greater levels of risk. Although both variable and fixed annuities can help investors save for their future, they differ significantly in terms of their structure, costs, and potential benefits. Deciding between Variable and Fixed Annuities? Click here. Variable annuities allow you to invest in various underlying portfolios, such as stocks, bonds, and mutual funds. These subaccounts can increase or decrease in value over time, subject to market performance. The amount of income you receive depends on the principal and the success of your investment portfolio selections and will fluctuate accordingly. As such, variable annuities are considered higher-risk investments with the potential to generate higher returns. Variable annuities also offer tax-deferred growth potential and death benefit protection. Fixed annuities are insurance contracts that provide a guaranteed income stream for a specified period. The income you receive is determined at the beginning of the contract. The value of a fixed annuity grows over time based on the set interest rate, which is typically higher than a traditional bank account and is guaranteed by the insurer. You can also benefit from tax-deferred growth and death benefit protection with a fixed annuity contract. Fixed a-nnuities are best for risk-averse investors who want to secure their financial future without taking on market volatility. Costs associated with variable and fixed annuities vary depending on the insurance company. Premiums, commissions, administrative fees, and surrender charges are all ordinary expenses: the more intricate the annuity, the greater the consumer costs. Variable annuities generally charge higher upfront costs than fixed annuities. These are the first investment when you buy an annuity, and they can be paid in a single lump sum or installments, depending on the type. The more premium you put into an annuity, the higher your retirement income will pay out. For example, a single-premium or lump sum annuity can get you started with at least $25,000. At the same time, installment-type premiums can start for as low as $2,500. These are levied annually to cover management, recordkeeping, and customer services. Companies can charge a flat fee of $30 annually or up to 0.3% of the total annuity cost. These are charged on withdrawals before the surrender period ends. While surrender fees vary per company, they are generally 10% of the total value of the annuity in its first year. The closer the surrender period ends, the lesser these fees are. Variable annuities have higher surrender fees and extended surrender periods than fixed annuities. Insurance companies also charge commissions to the agent who sold you the annuity. They can range from 1% to 10% of the total value, depending on the type and complexity of the particular annuity. In most cases, fixed annuities translate to a higher commission. The insurance company charges these to cover losses in case of unexpected events like the death of an annuitant. Depending on factors such as age and health, it ranges from 0.5% to 1.5% of the total annuity value. Variable annuities also include investment management fees that cover portfolio management expenses. Insurance companies can charge up to 3% of the total variable annuity cost for these fees per year. These are extra costs depending on the provisions or added benefits you may want to include in your annuity contract, like guaranteed minimum withdrawal or death benefits. Riders can cost up to 1.15% of the total annuity value. To help you decide on which annuity to get, consider the following advantages and disadvantages of variable annuities: The benefits of variable annuities include tax deferral, lifetime income stream, and protected funds. Variable annuities offer tax deferral, meaning you only pay taxes on your investment gains once you withdraw money. You can keep more of your earnings in the short term and potentially receive a larger payout over the long term. Variable annuities offer a lifetime income stream. You may receive an income stream over your retirement that may last longer than if you had invested in a fixed annuity. Variable annuities also offer capital protection. Your initial investment is safe from market fluctuations and will remain intact regardless of how the stock market performs. These include high fees, risk charges, the potential of low returns, and inaccessibility. The downside of variable annuities is that they often come with higher costs than fixed annuities. These fees can range from a one-time payment to ongoing annual charges, depending on the type of annuity you purchase. Variable annuities also come with risk charges, which you pay to cover the insurance company’s costs of managing your account. These charges can be substantial and may significantly reduce your potential return on investment. Variable annuities also have the potential to produce low returns. Since they are subject to market fluctuations, you could end up with lower income payouts than if you bought a fixed annuity. Variable annuities also have a downside: your money is locked away and not easily accessible, especially since they have more extended surrender periods. You will incur higher surrender charges if you need to access funds before retirement. You may also consider the following benefits and drawbacks when choosing a fixed annuity: Fixed annuities are predictable, tax-deferred, simple, and guaranteed. This is the primary advantage of a fixed annuity. Since annuitants receive guaranteed returns, they can count on money coming in each month as long as they live and would not have to worry about the market. A fixed annuity has the same tax deferral benefits as a variable annuity. Invested money does not have to be declared as income until withdrawals are made, allowing for additional growth. A fixed annuity is often easier to understand than a variable annuity since the returns are predetermined and not dependent on market conditions. It does not need constant monitoring and makes it simpler for investors to plan their retirement income. Since the principal earns based on a fixed interest rate, the returns are guaranteed upfront. A fixed annuity is ideal for those who prefer more consistency in their investments. Fixed annuities charge early withdrawal penalties and are exposed to inflation. One of the drawbacks of a fixed annuity is that returns are not always able to keep up with inflation. As the cost of living increases, an annuitant could see their purchasing power decreasing as their fixed payments remain the same. A fixed annuity also usually comes with a surrender fee for early withdrawals. Investors must commit to the length of the annuity contract to receive all their returns or face a steep penalty if they wish to take out their money early. Both variable and fixed annuities assure a steady income stream during your retirement. However, one may be more beneficial depending on your unique preferences, risk tolerance, needs, and goals. Variable annuities offer you greater growth potential each year in exchange for a higher risk. Your money will be invested in stocks, bonds, or mutual funds, which can provide both capital protection and market appreciation over time. However, there is no guarantee of how much money you could make or lose with these investments. If you consider yourself risk-tolerant, consider variable annuities. Fixed annuities are more conservative than variable annuities since they do not involve any stock market risk. Instead, your money is pooled with other investors and invested by the insurance company in fixed-income securities and will earn interest rates. Your principal will be protected, but your growth potential may be lower. Fixed annuities are suitable if you are a risk-averse investor. Whether variable or fixed, annuities are a great way to ensure financial security during your retirement years. However, depending on your financial situation, risk tolerance, and financial goals, one type of annuity may be more suitable for you than the other. Consider all the factors above before making a decision. It is also recommended that you speak with a professional about your retirement planning needs and get guidance on various available annuities. Doing so may help avoid any costly mistakes down the road.Variable vs Fixed Annuities: An Overview

What Are Variable Annuities?

What Are Fixed Annuities?

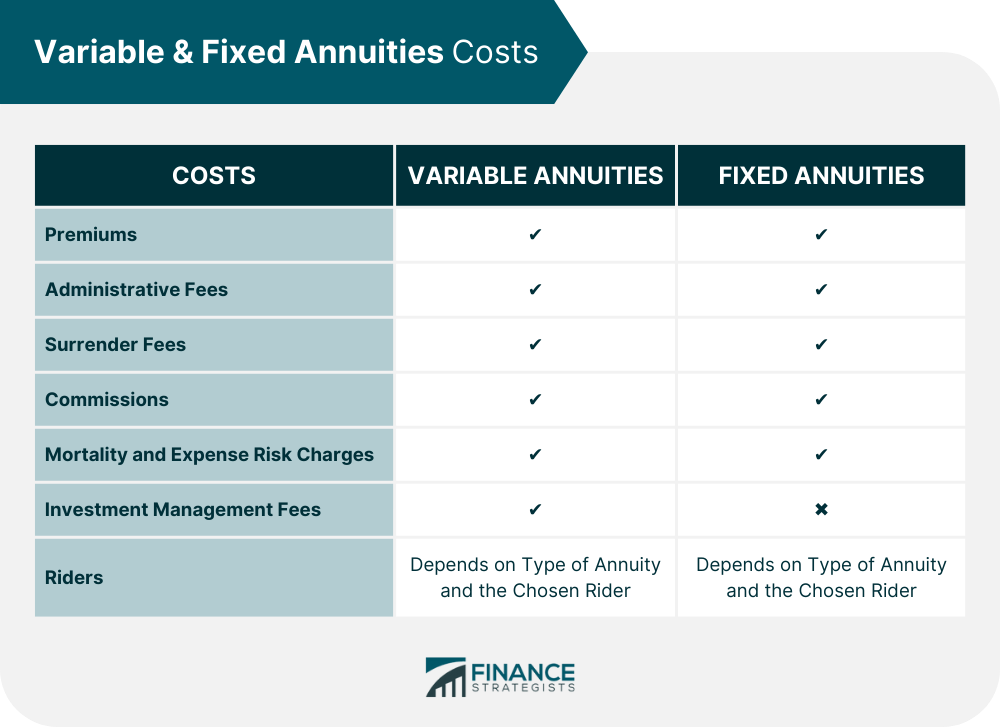

Variable & Fixed Annuities Costs

Premiums

Administrative Fees

Surrender Fees

Commissions

Mortality and Expense Risk Charges

Investment Management Fees

Riders

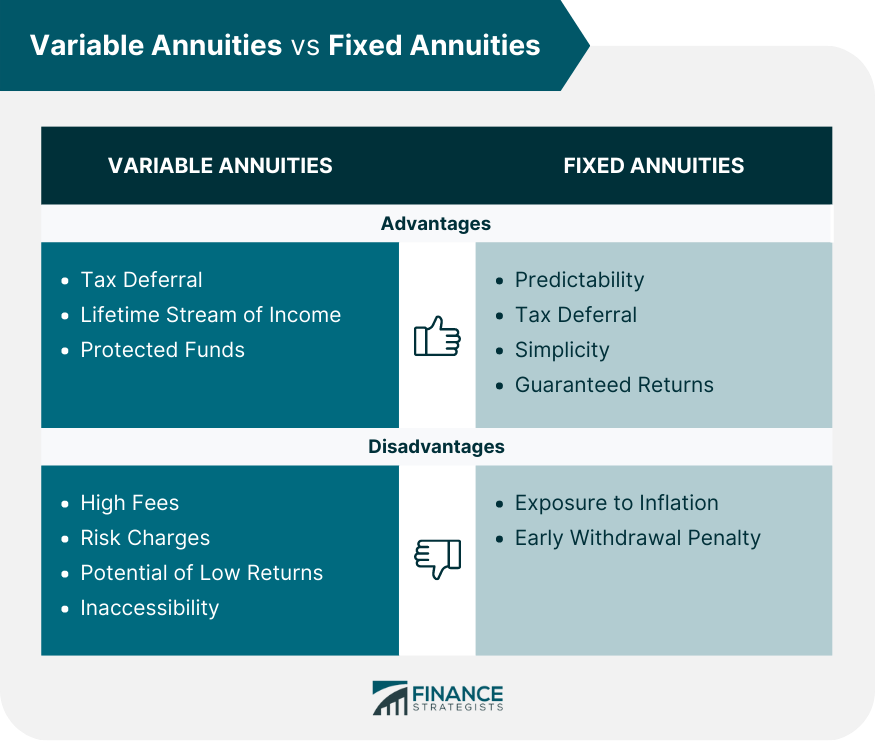

Variable Annuity Pros & Cons

Pros

Tax Deferral

Lifetime Stream of Income

Protected Funds

Cons

High Fees

Risk Charges

Potential of Low Returns

Inaccessibility

Fixed Annuity Pros & Cons

Pros

Predictability

Tax Deferral

Simplicity

Guaranteed Returns

Cons

Exposure to Inflation

Early Withdrawal Penalty

The Bottom Line

Variable vs Fixed Annuities FAQs

The main differences between variable and fixed annuities are the type of investment, associated risks, fees, and returns. Variable annuities offer a wide range of assets that can provide higher potential growth but also come with more risk. With fixed annuities, you get a guaranteed rate of return for a certain period with no stock market exposure.

Although fixed annuities generally offer low risk, there is still a chance of losing money if the insurance company holding your annuity goes out of business. Also, depending on the type of fixed annuity, there may be surrender charges for withdrawals before maturity.

An annuity is a contract between an individual and an insurance company. The individual pays money into it, either in one lump sum or multiple payments over time. In exchange, the insurance company agrees to provide income for a predetermined period or a lifetime. There are two types of annuities: variable and fixed.

A variable annuity typically pays out to a beneficiary upon the annuitant's death. It can be based on either the current market value or an agreed-upon guaranteed value. The proceeds are paid to their estate if the insured has not named a beneficiary.

Generally, the beneficiary of a variable annuity will be taxed on any distributions received from it. The taxable amount depends on the amount of money withdrawn. Your tax advisor can provide more information on reporting income from inherited variable annuities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.