Converting life insurance to annuities is a financial strategy that involves transforming the death benefit of a life insurance policy into a stream of income through an annuity contract. This conversion allows policyholders to access the accumulated cash value of their life insurance policy and convert it into a guaranteed income stream for retirement. The process typically involves surrendering the life insurance policy, receiving a lump sum payout, and using that amount to purchase an annuity. Converting life insurance to annuities can provide individuals with a reliable income source and help meet their retirement goals. However, it is essential to understand the terms, costs, and potential tax implications associated with this conversion before making a decision. As people age, their financial needs often shift. Life insurance is crucial for individuals who have dependents relying on their income. However, as children become independent or a mortgage gets paid off, the need for life insurance may decrease. Instead, the focus often shifts towards income stability in retirement, a need that annuities can fulfill. Annuities can be a key component of retirement planning. They offer a way to receive a steady income stream in retirement, providing financial security when regular employment income ceases. Depending on the annuity, this income can be guaranteed for life, regardless of how long the annuitant lives. While life insurance provides financial security for your loved ones in the event of your death, annuities are designed to provide a steady income during retirement. The decision to convert a life insurance policy into an annuity should be based on factors such as current financial situation, future income requirements, and the existing life insurance and annuity market conditions. The following are key points to consider for the conversion of life insurance to annuities: 1. Type of Insurance Policy: The type of life insurance policy is the primary determinant of whether or not a policy can be converted to an annuity. As previously mentioned, term life insurance policies do not possess a cash value and are ineligible for conversion. On the other hand, whole life and universal life insurance policies build cash value over time and are generally convertible. 2. Policy Value: The cash value of the policy is another critical factor. Policies with higher cash values will yield larger annuities than those with lower ones. Remember, the cash value of a policy grows over time, so a policy that's been in effect for several years will likely have a larger cash value than a newer policy. 3. Policyholder's Age and Health: These are significant considerations as well. Older policyholders or those with serious health conditions may find it more beneficial to retain their life insurance policies to benefit their beneficiaries. However, individuals in good health with a longer life expectancy might find the guaranteed income stream of an annuity more appealing. 4. Surrender Charges: The insurance company charges fees when a policy is surrendered before its term ends. These charges can significantly reduce the cash value that's available for conversion into an annuity. Therefore, it's important to understand any surrender charges associated with your policy. 5. Financial Goals and Needs: Lastly, your personal financial goals and needs play a vital role in determining whether a conversion is suitable. If you require a steady income stream during retirement and don't have a high need for leaving a substantial death benefit to your beneficiaries, converting your life insurance policy to an annuity might be an excellent option. Insurance companies and insurance brokers play significant roles in the process of turning insurance into an annuity. Insurance companies are responsible for offering annuity products and facilitating the conversion of life insurance policies into annuities. They provide the necessary paperwork, guidance, and support throughout the conversion process. Insurance brokers, on the other hand, act as intermediaries between policyholders and insurance companies. They help policyholders explore their options, compare different annuity products, and find the most suitable annuity for their specific needs and financial goals. Insurance brokers can provide valuable insights, explain the terms and conditions of various annuity contracts, and assist policyholders in making informed decisions. Their expertise and market knowledge can help policyholders navigate the complexities of the conversion process and ensure they make the right choice when turning insurance into an annuity. The decision to convert a life insurance policy to an annuity should be based on a comprehensive review of your current financial situation. This involves examining your income, expenditures, savings, debts, and other financial commitments. It's also important to factor in your future financial goals. Are you aiming for a secure, steady income in your retirement years? Do you have substantial debts that need to be taken care of? Will your beneficiaries be financially secure without the death benefit of your life insurance policy? Answering these questions will help assess whether a conversion is viable for your particular circumstances. The conversion process can be complex and requires expert knowledge. A financial advisor or insurance broker can help guide you through this process. They can assess the feasibility of conversion, considering your specific situation and long-term financial goals. They can also help select the right type of annuity that suits your needs and preferences. The guidance of these professionals is invaluable in making an informed decision. The actual process of converting your life insurance policy to an annuity involves several steps, and you must understand these steps before proceeding. You should be aware of the potential costs, including any surrender charges associated with your life insurance policy and the tax implications of the conversion. Additionally, it's crucial to understand that conversion is generally a permanent process. Once you surrender your life insurance policy and purchase an annuity, you may not revert to the original life insurance policy. As such, make sure you clearly understand what conversion entails and how it will impact your financial future. After careful consideration and planning, the last step is to execute the conversion. This involves surrendering your life insurance policy to the insurance company in exchange for its cash value. Once you receive these funds, you can then use them to purchase an annuity. The exact process and timing will depend on the terms and conditions set by your insurance company and the specific annuity product you choose. There can be costs and penalties associated with the conversion process. For example, surrender charges may apply when cashing in a life insurance policy, particularly if it’s done during the policy's early years. Additionally, the acquisition costs for annuities can also be high. Converting a life insurance policy into an annuity can affect your beneficiaries. The death benefit provided by the life insurance policy will be lost upon conversion, which could impact your beneficiaries' financial security, especially if they are still dependent on your income. The conversion process can have tax implications. While life insurance death benefits are generally tax-free, distributions from annuities can be subject to tax. Therefore, understanding the tax implications before proceeding with conversion is crucial. The primary advantage of converting a life insurance policy into an annuity is the creation of a reliable income stream during retirement. When employment income ceases, an annuity can provide a steady inflow of funds, making it easier to manage expenses and maintain your lifestyle. Annuities can be structured to provide income for the rest of your life, offering peace of mind. This guarantee remains regardless of market fluctuations or how long you live, providing financial security. Depending on the specifics of the life insurance policy and the annuity, the return on investment from an annuity can be higher than the cash value accumulation in a life insurance policy. One significant disadvantage of converting a life insurance policy into an annuity is that it involves surrendering the death benefit. This benefit provides financial protection to your beneficiaries upon your death. Giving up this benefit can impact your family's financial security, especially if they rely heavily on this prospective fund. The conversion process may involve costs such as surrender charges, which can eat into the cash value received from the life insurance policy. Also, the tax implications of conversion can be complex. While life insurance proceeds are generally tax-free, annuity payments are typically taxed as ordinary income. Therefore, it's important to consult a tax professional before deciding. Annuities provide a fixed income, which can be a double-edged sword. While stability can be comforting, the purchasing power of fixed-income payments can decrease over time due to inflation. Some annuities offer inflation protection, but these typically come at a higher cost. Unlike life insurance policies that may allow for loans or withdrawals, annuities are not as flexible. If you unexpectedly need a large sum of money, accessing funds from an annuity without incurring penalties can be more difficult. Converting a life insurance policy into an annuity involves careful consideration of various factors, including the need for a steady income stream in retirement, current and future financial goals, and the impact on beneficiaries. Insurance companies and insurance brokers play crucial roles in facilitating this conversion process, providing guidance and support throughout. The steps to convert involve evaluating the current financial situation, consulting professionals, understanding the process, and executing the conversion. However, there are considerations to keep in mind, such as costs, penalties, the loss of the death benefit, tax implications, inflation risk, and potential lack of liquidity. It's essential to weigh the advantages of a steady income, lifetime income, and the possibility of higher returns against the drawbacks before making a decision. Seeking advice from financial professionals and tax experts is highly recommended to make an informed choice that aligns with individual financial needs and goals.Overview of Converting Life Insurance to Annuities

Understanding the Need to Convert Life Insurance to Annuity

Changing Financial Needs With Age

Retirement Planning and Annuities

Analyzing the Benefits of Life Insurance and Annuity

Process of Turning Life Insurance Into Annuity

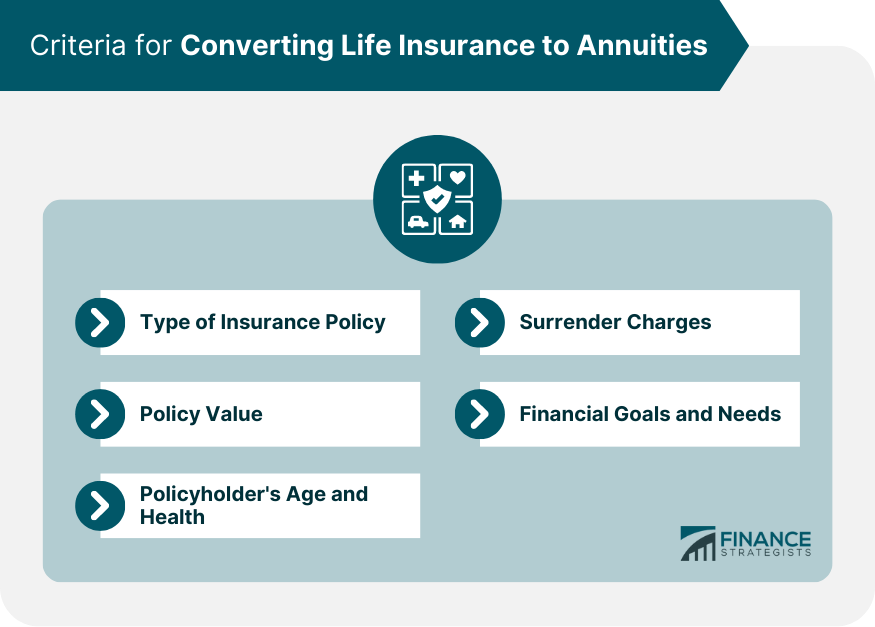

Criteria for Conversion

Role of Insurance Companies and Insurance Brokers in the Process

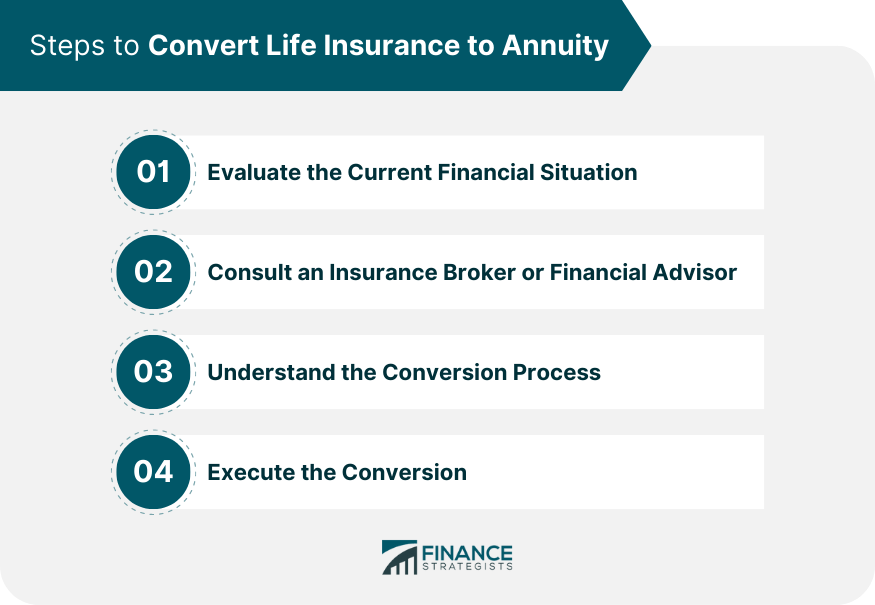

Steps to Convert Life Insurance to Annuity

Evaluating the Current Financial Situation

Consulting an Insurance Broker or Financial Advisor

Understanding the Conversion Process

Executing the Conversion

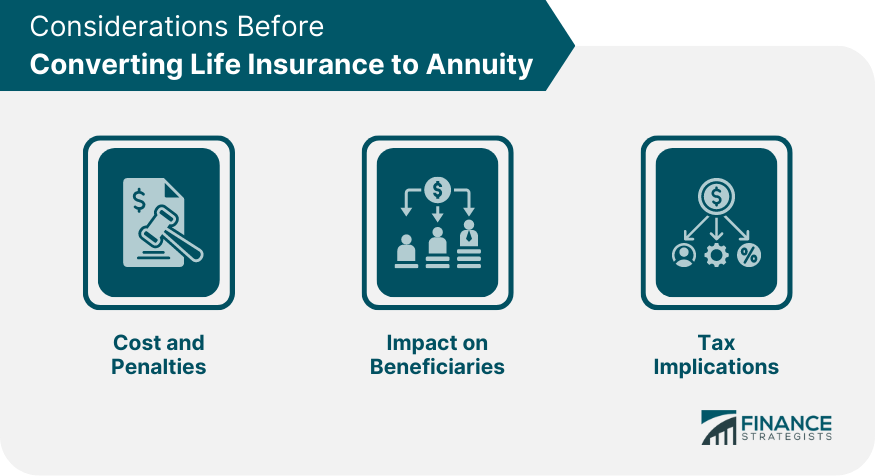

Considerations Before Converting Life Insurance to Annuity

Cost and Penalties of Conversion

Impact on Beneficiaries

Tax Implications

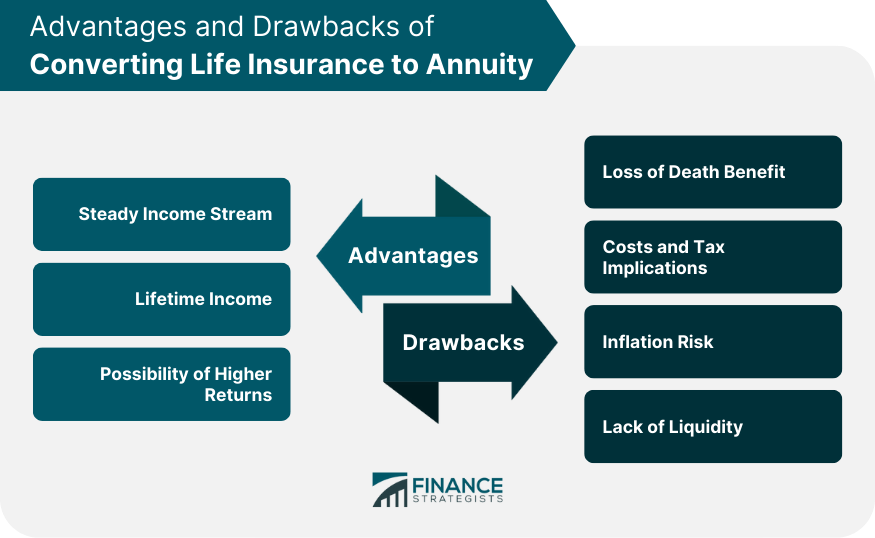

Advantages of Converting Life Insurance to Annuity

Steady Income Stream

Lifetime Income

Possibility of Higher Returns

Drawbacks of Converting Life Insurance to Annuity

Loss of Death Benefit

Costs and Tax Implications

Inflation Risk

Lack of Liquidity

Conclusion

Convert Life Insurance to Annuity FAQs

No, only life insurance policies with a cash value component, such as whole life or universal life insurance, can be converted into annuities.

Unlike life insurance death benefits, which are generally tax-free, distributions from annuities can be subject to tax.

The primary benefit is the creation of a steady income stream during retirement. This can provide financial security when employment income ceases. This income could be guaranteed for life, depending on the type of annuity chosen.

The conversion process can result in the loss of the life insurance policy's death benefit, which may impact beneficiaries' financial security. Additionally, there could be surrender charges and tax implications associated with conversion.

While not mandatory, consulting a financial advisor is highly recommended due to the complexity of the conversion process and the potential financial implications. They can provide personalized advice based on your unique financial situation and goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.