Whether you should put your 401(k) into an annuity is a decision that depends on your personal circumstances, financial goals, and risk tolerance. Annuities can provide a guaranteed income stream in retirement, which can offer financial stability. However, they often come with high fees, surrender charges, and certain tax implications. They also limit your access to funds, which could be an issue during financial emergencies. Your health and anticipated life expectancy play a significant role, as annuities can be beneficial if you expect to live a long life. It's also crucial to consider the reputation and financial strength of the annuity provider. Given the complex nature of this decision, it's highly recommended to consult with a trusted financial advisor to understand how this choice aligns with your overall retirement income plan. The choice to transition your 401(k) to an annuity should reflect your overarching financial targets and risk comfort level. It's imperative to deliberate how the annuity integrates with your comprehensive retirement strategy. While an annuity can offer a dependable revenue flow, it shouldn't stand as your sole source of retirement income. Diversifying income sources is fundamental to managing retirement-associated risks. Your current health condition and estimated life span significantly impact the benefits you might receive from an annuity. If longevity is anticipated, the secured lifetime disbursements from an annuity could be advantageous. The trustworthiness and fiscal robustness of the annuity provider are crucial elements to bear in mind. You want to ensure that the insurance firm will sustain its responsibilities in the long run. Retirement-related financial decisions can be intricate. Collaborating with a dependable financial consultant can enable you to traverse these decisions with increased assurance. A compelling aspect of an annuity is the certainty it brings by offering a stable income for life or a determined duration. This assurance gives retirees stability and peace of mind, knowing they have a reliable income source. The chosen annuity type influences the prospect of income growth. Specifically, variable and indexed annuities present the potential for income payments to increase, anchored on market performance. This aspect of growth is an added advantage for many retirees. Annuities have a unique protective feature that shields against exhausting one's savings, a prevalent worry for many retirees. As life expectancy rises, this feature becomes increasingly pivotal. Certain annuity types extend a death benefit to beneficiaries. This provision introduces another level of financial security for loved ones following the annuity holder's demise, making annuities a potentially valuable component of estate planning. Annuities often come with high fees, which can eat into retirement savings. Additionally, early withdrawal from an annuity contract may lead to substantial surrender charges, which can be a disadvantage if you need to access your funds early. While transferring your 401(k) into an annuity can avoid immediate tax implications, future withdrawals from the annuity will be subject to income tax. Also, unlike 401(k) or IRAs, annuities do not offer any additional tax advantages. Annuities often have restrictions on withdrawals, especially during the early years of the contract. This limited access can be problematic in case of unexpected financial needs or emergencies. Fixed annuities do not usually adjust for inflation. This could mean that the purchasing power of the annuity payments could decrease over time, especially in a high-inflation environment. Instead of transferring your complete 401(k) into an annuity, retaining it and devising a tactical withdrawal scheme might be a viable alternative. This approach offers enhanced flexibility and accessibility to your savings. Another viable alternative could be transferring your 401(k) into an Individual Retirement Account (IRA). This provides more possibilities for investments and possibly lower charges, which can maximize your retirement income. You may also consider converting only a segment of your 401(k) balance into an annuity rather than the entire sum. This strategy could enable you to buy an immediate annuity, ensuring a consistent income flow. The leftover funds can be invested for potential growth or allocated for emergency expenses, providing both security and flexibility in your financial planning. The decision to roll your 401(k) into an annuity requires a careful evaluation of several factors, including your financial goals, risk tolerance, health, and anticipated life expectancy. While annuities can provide a guaranteed income stream and offer protection against outliving your savings, they may also carry high fees and surrender charges, along with potential tax implications. There is also a need to consider the reputation and financial health of the annuity provider, as well as other alternatives, such as retaining your 401(k) and implementing a strategic withdrawal plan or transferring it into an IRA. As such, it's vital to seek professional advice before making this significant decision. This will ensure that your retirement savings strategy aligns with your needs, expectations, and long-term financial health.Should You Put Your 401(k) Into an Annuity?

Key Considerations Whether You Should Put Your 401(k) Into an Annuity

Financial Goals and Risk Tolerance

Retirement Income Plan

Health and Life Expectancy

Annuity Provider

Seek Expert Advice

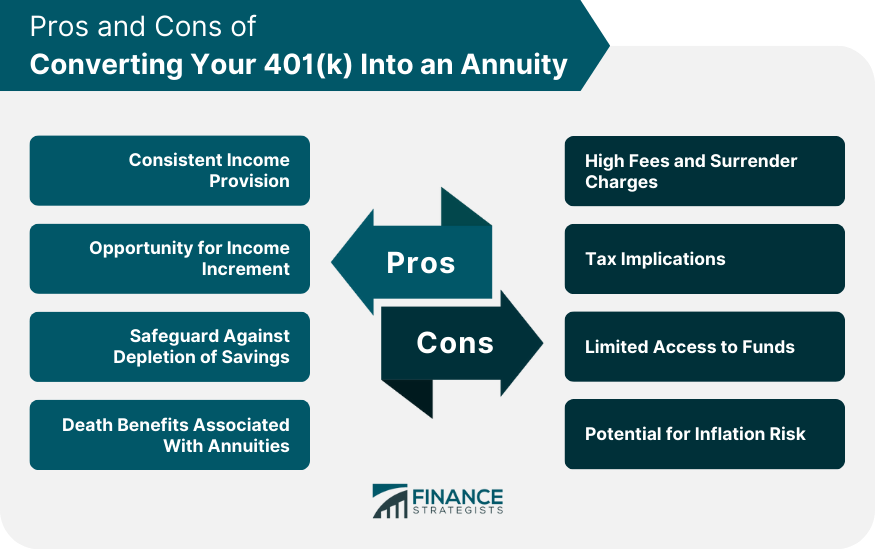

Pros of Converting Your 401(k) Into an Annuity

Consistent Income Provision

Opportunity for Income Increment

Safeguard Against Depletion of Savings

Death Benefits Associated With Annuities

Cons of Converting Your 401(k) Into an Annuity

High Fees and Surrender Charges

Tax Implications

Limited Access to Funds

Potential for Inflation Risk

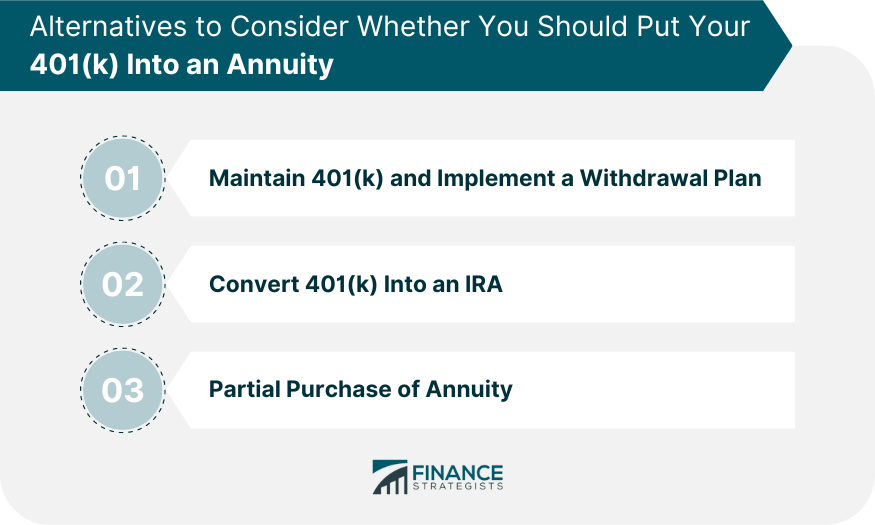

Alternatives to Consider Whether You Should Put Your 401(k) Into an Annuity

Maintain 401(k) and Implement a Withdrawal Plan

Convert 401(k) Into an IRA

Partial Purchase of Annuity

Bottom Line

Should You Put Your 401(k) Into an Annuity? FAQs

An annuity is a financial product offered by an insurance company that provides a steady income stream for a specified period or for life. Transferring a 401(k) into an annuity involves a rollover, where funds from the 401(k) are moved to an annuity contract without triggering a taxable event.

The main advantages include a guaranteed income stream for life or a specified period, potential for income growth with certain types of annuities, protection against outliving your savings, and some annuities offer a death benefit to beneficiaries.

Risks include high fees and surrender charges, tax implications on future withdrawals, limited access to funds in case of emergencies, and potential losses due to inflation if the annuity doesn't adjust for the cost of living.

Key factors include your financial goals and risk tolerance, overall retirement income plan, health and life expectancy, reputation and financial strength of the annuity provider, and advice from financial advisors.

Yes, alternatives include keeping your 401(k) and developing a strategic withdrawal plan, rolling your 401(k) into an Individual Retirement Account (IRA), or using a portion of your 401(k) to purchase an immediate annuity for income diversification while keeping the remainder for growth or emergencies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.