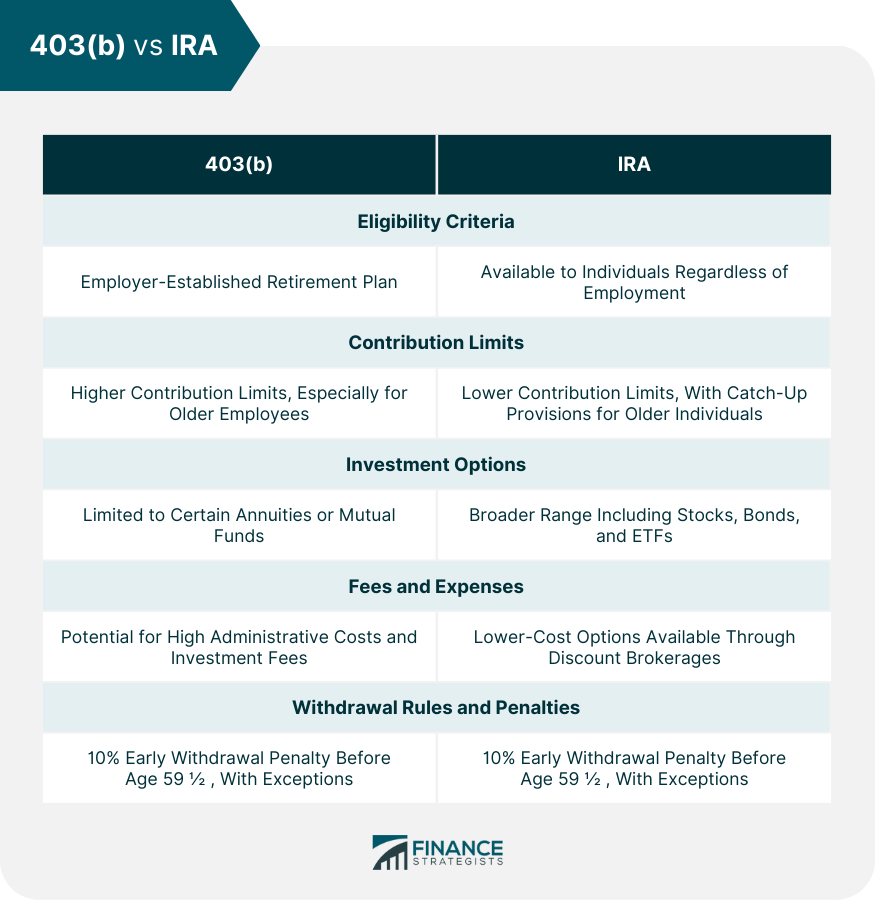

A 403(b) annuity is a type of tax-sheltered retirement plan, often utilized by public schools and certain tax-exempt organizations. Also known as a tax-sheltered annuity (TSA) plan, this retirement vehicle allows employees to make pre-tax contributions, which can grow tax-free until withdrawal at retirement. An Individual Retirement Account (IRA) is another form of retirement savings plan, which offers various tax advantages to encourage individuals to save for their retirement. Two primary types of IRAs are Traditional IRAs and Roth IRAs, each having distinct tax benefits and eligibility requirements. A rollover involves transferring funds from one retirement account to another, usually without incurring tax penalties. Upon leaving a job or retiring, it's crucial to decide what to do with your retirement savings. Rolling your 403(b) annuity into an IRA can be an excellent way to maintain the tax-advantaged status of these funds, while possibly gaining access to a broader range of investment options. A major advantage of IRAs over 403(b) plans is the broader access to a wider array of investment options. While 403(b) plans typically restrict you to a select group of annuities or mutual funds, IRAs generally offer a much wider range of investments, including individual stocks, bonds, ETFs, and even real estate in certain types of IRAs. If you've accumulated multiple 403(b) accounts over your career, consolidating these accounts into a single IRA can simplify your financial life. It's easier to manage and keep track of your savings and investments when they're held in one place. An IRA often offers more flexibility and control over your retirement savings compared to a 403(b) plan. With an IRA, you're free to choose the financial institution, decide on the specific investments, and have greater flexibility on withdrawal rules. In most cases, you're eligible to roll over your 403(b) annuity into an IRA if you've experienced a separation from service - meaning you've left the employer that established the 403(b) plan. While there are no specific age requirements for a 403(b) to IRA rollover, it's essential to be aware of other age-related rules. For instance, starting at age 73, account owners must begin taking Required Minimum Distributions (RMDs) from both 403(b) plans and Traditional IRAs. It's worth noting that you cannot roll over hardship distributions, which are immediate and heavy financial needs. Understanding the IRS guidelines around such distributions is crucial to avoid potential tax penalties. First, decide whether to roll over your 403(b) funds into a Traditional IRA or a Roth IRA. A Traditional IRA offers tax-deferred growth, meaning you'll pay taxes upon withdrawal, while a Roth IRA offers tax-free growth, meaning you pay taxes upfront, but withdrawals in retirement are tax-free. Once you've decided on the type of IRA, you'll need to open an account with a financial institution. This could be a bank, brokerage firm, or any financial services company that offers IRA services. After your new IRA is set up, contact your 403(b) plan provider to start the rollover process. They will guide you through their specific process and provide the necessary paperwork. Ensure that you conduct a direct rollover, also known as a trustee-to-trustee transfer, to avoid any tax withholdings. In this type of transfer, the funds move directly from your 403(b) account to your new IRA, without you ever touching the money. Finally, once the rollover is initiated, ensure to confirm the completion of the process. This usually involves checking with both your 403(b) provider and your new IRA provider to ensure the funds have been correctly transferred. Transferring your 403(b) annuity to an IRA is a significant financial decision. Understanding the whys and hows of this process can help you make a more informed choice and potentially lead to greater control over your retirement savings and broader investment opportunities. The most common scenario involves rolling over a 403(b) annuity to a traditional IRA. It offers a straightforward rollover since both accounts are tax-deferred. This means you contribute pre-tax dollars, and then pay taxes on withdrawals in retirement. It's a popular choice due to its simplicity and the fact that it typically doesn't trigger any immediate tax consequences. Conversely, you may opt for a rollover to a Roth IRA. This scenario involves a conversion process commonly known as a "Roth conversion." Since Roth IRAs are funded with post-tax dollars, you will owe income taxes on the amount converted. However, this can be beneficial if you expect to be in a higher tax bracket in retirement, as withdrawals from Roth IRAs are tax-free. If your new job offers a 401(k) plan and the plan allows it, you can opt to roll over your 403(b) into your new employer's 401(k) plan. This decision could make sense if you prefer to keep your retirement savings consolidated in one account and if the 401(k) plan offers attractive investment options. Rollovers from a 403(b) to a traditional IRA are typically tax-free, provided they are done correctly. To maintain the tax-free status, ensure you conduct a direct rollover where funds are transferred directly between financial institutions. An indirect rollover, where you receive the distribution from your 403(b) and then deposit it into your IRA within 60 days, can trigger mandatory tax withholding of 20%. If you fail to complete the rollover within 60 days, the entire distribution may be considered taxable income and may also be subject to a 10% early withdrawal penalty if you're under 59½ years of age. Rolling over a 403(b) into a Roth IRA requires you to pay income taxes on the amount converted. This tax is due in the year you make the conversion. If you opt for an indirect rollover, ensure to deposit the funds into your IRA within 60 days to avoid taxes and potential early withdrawal penalties. The pro-rata rule comes into play when you have pre-tax and after-tax amounts in your 403(b). It stipulates that each distribution (or rollover) from your 403(b) is considered to include both pre-tax and after-tax amounts in the same proportion as they exist within your account. Ensure to be aware of any fees associated with rolling over your 403(b) to an IRA. These may include administrative fees or charges related to the sale of investments in your 403(b). Starting at age 73, you must take Required Minimum Distributions (RMDs) from your traditional IRA. Failing to do so can result in hefty penalties. However, Roth IRAs are not subject to RMDs during the owner's lifetime. While both 403(b) and IRA are designed to help individuals save for retirement, they differ in their eligibility criteria, contribution limits, investment options, and withdrawal rules. IRAs typically offer a broader range of investment options compared to 403(b) plans. While 403(b) plans may restrict you to certain annuities or mutual funds, IRAs allow you to invest in individual stocks, bonds, and ETFs. Fees and expenses can also differ between the two accounts. Some 403(b) plans may have high administrative costs and investment fees, while IRAs offered by discount brokerages can provide low-cost investment options. While both 403(b) plans and traditional IRAs impose a 10% early withdrawal penalty if you take distributions before age 59½, there are certain exceptions to this rule for each account type. It's important to understand these rules before deciding to roll over your 403(b) to an IRA. Navigating retirement finances is complex, but understanding tools like a 403(b) annuity rollover to an IRA can make a difference in achieving financial goals. Rolling over a 403(b) to an IRA offers advantages such as diverse investment options, potentially lower fees, and streamlined financial management. It also provides more control over retirement savings for customized planning. Eligibility for the rollover usually occurs after leaving the job that established the 403(b) plan, although individual circumstances like hardship distributions may affect the process. Rolling over involves steps like choosing the right IRA type, establishing the account, initiating the rollover with the 403(b) provider, ensuring direct transfer, and confirming completion. Engaging a knowledgeable insurance broker or financial advisor is crucial for guidance and aligning the rollover with overall retirement strategy. Seeking professional advice ensures informed decisions for a secure financial future.Overview of 403(b) Annuity Rollover to IRA

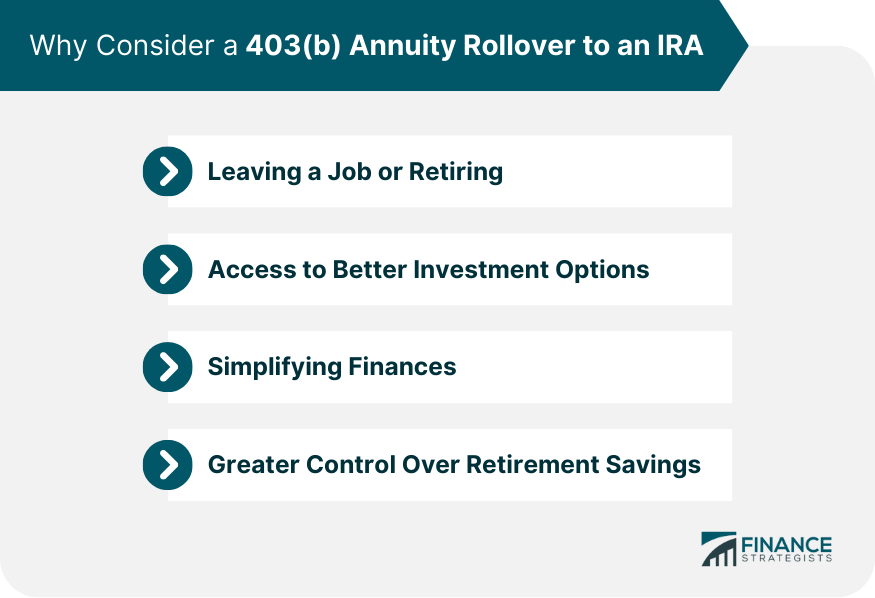

Why Consider a 403(b) Annuity Rollover to an IRA

Leaving a Job or Retiring

Access to Better Investment Options

Simplifying Your Finances

Greater Control Over Retirement Savings

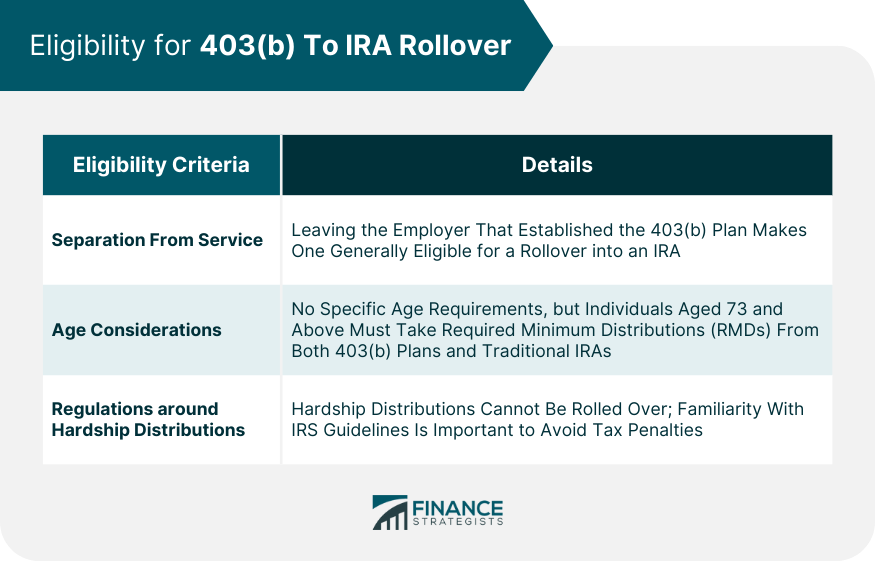

Eligibility for 403(b) To IRA Rollover

Separation From Service

Age Considerations

Regulations Around Hardship Distributions

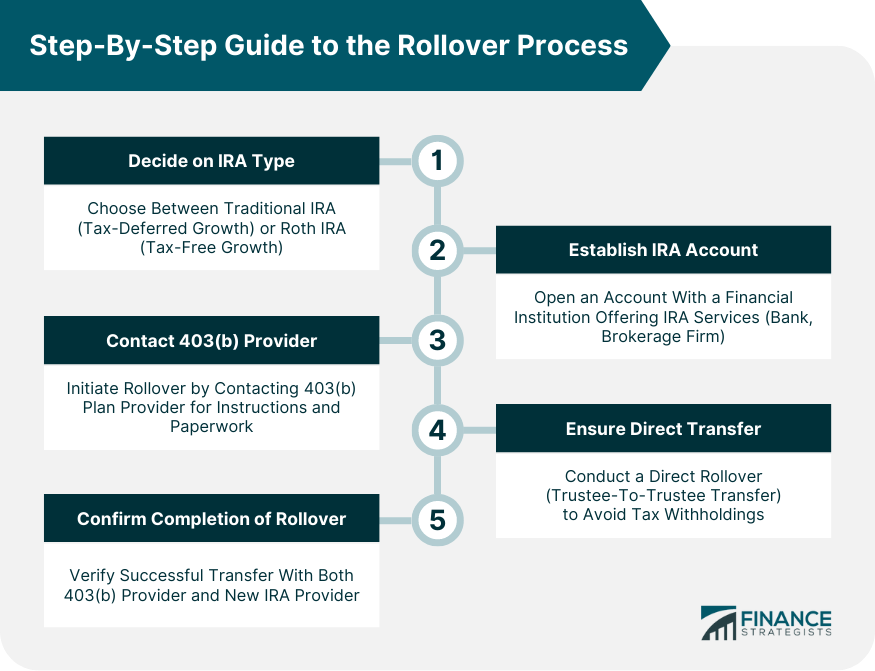

Step-By-Step Guide to the Rollover Process

Decide on the Type of IRA (Traditional or Roth)

Establish the IRA Account

Contact 403(b) Provider to Initiate Rollover

Ensure Direct Transfer (Rollover) to Avoid Withholding Tax

Confirm Completion of Rollover

Different Scenarios for 403(b) to IRA Rollover

Rollover to a Traditional IRA

Rollover to a Roth IRA

Rollover to a New Employer's 401(k)

Tax Considerations of a 403(b) to IRA Rollover

Tax-Free Rollovers

Withholding and Penalties for Indirect Rollovers

Roth Conversions and Tax Implications

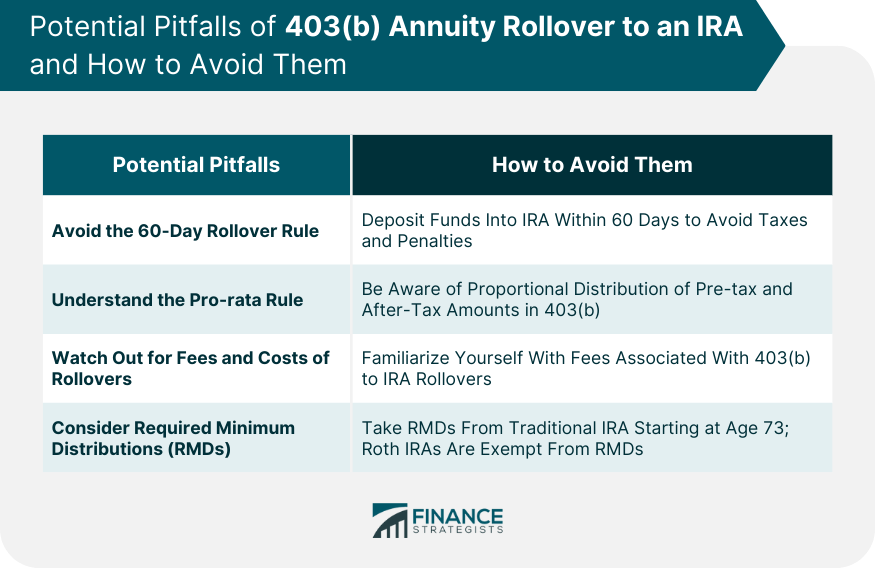

Potential Pitfalls and How to Avoid Them

Avoiding the 60-Day Rollover Rule

Understanding the Pro-Rata Rule

Watch Out for Fees and Costs of Rollovers

Considering Required Minimum Distributions (RMDs)

Comparison of 403(b) and IRA

Similarities and Differences

Investment Options

Fees and Expenses

Withdrawal Rules and Penalties

Bottom Line

403(b) Annuity Rollover to IRA FAQs

A rollover from a 403(b) to an IRA often gives you access to a broader range of investment options, potentially lower fees, greater control over your retirement funds, and can simplify your finances by consolidating multiple accounts.

Generally, you're eligible for a rollover when you've left the employer that established your 403(b) plan. However, rules can vary, and certain distributions like hardship distributions may not be eligible.

To initiate a rollover, you first need to establish an IRA account, then contact your 403(b) provider to begin the process. It's recommended to do a direct rollover to avoid taxes and penalties.

If you roll over your 403(b) to a traditional IRA, the rollover is typically tax-free. If you roll over to a Roth IRA, you will owe taxes on the amount converted.

Potential pitfalls include failing to complete an indirect rollover within 60 days, not understanding the pro-rata rule, incurring high fees, and neglecting Required Minimum Distributions (RMDs) if you're 73 or older.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.