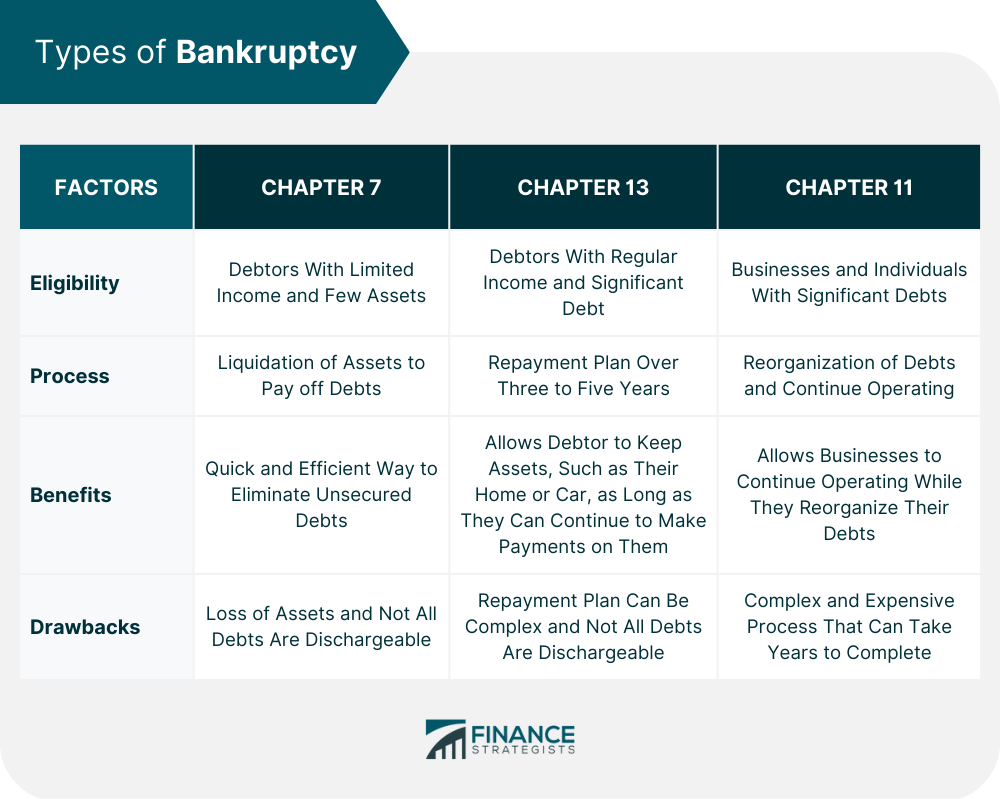

Bankruptcy is a federal court process designed to help individuals or businesses struggling with debt. It allows them to eliminate or reorganize their debts and get a fresh start. Bankruptcy is governed by federal law, and the proceedings occur in a bankruptcy court. The process involves a trustee appointed by the court to oversee the case, and creditors, who are the parties owed money. The purpose of bankruptcy is to provide relief to those overwhelmed by debt and unable to pay their creditors. It is not a way to escape financial obligations or avoid responsibility for one's debts. Instead, it is a way to provide a fresh start and a second chance to those who have fallen in hard times. There are three common types of bankruptcy: Chapter 7, Chapter 13, and Chapter 11. Each type of bankruptcy has its own eligibility requirements, process, benefits, and drawbacks. This is the most common type of bankruptcy for individuals. It is also known as a "liquidation" bankruptcy because it involves liquidating assets to pay off debts. In a Chapter 7 bankruptcy, the trustee sells the debtor's non-exempt assets, and the proceeds are used to pay off creditors. To be eligible for Chapter 7 bankruptcy, it involves a “means test,” which compares the debtor's income to the median income in their state. If the debtor's income is below the median, they are eligible for Chapter 7 bankruptcy. If their income is above the median, they may still be eligible if they can demonstrate that they do not have enough disposable income to pay off their debts. Filing for Chapter 7 bankruptcy takes several steps. The debtor must file a petition with the bankruptcy court, along with a schedule of their assets and liabilities, income and expenses, and other financial information. They must also attend a meeting of creditors, where they will be asked questions about their financial situation. If the debtor has non-exempt assets, the trustee will sell them and distribute the proceeds to the creditors. Most debts are discharged or eliminated at the end of the process. One of the benefits of Chapter 7 bankruptcy is that it provides a quick and efficient way to eliminate most types of unsecured debts, including credit card debt and medical bills. However, it has several drawbacks. One of the primary drawbacks is that it involves liquidating assets, which can be a significant loss for the debtor. Additionally, not all debts are dischargeable in Chapter 7 bankruptcy such as student loans and taxes. This type of bankruptcy allows individuals to reorganize their debts and repay them over a period of three to five years. It is also known as a "wage earner's" bankruptcy because it is designed for individuals who have a regular income but struggle to keep up with their debts. To qualify for Chapter 13 bankruptcy, the debtor must have a regular income, and their debts must be within certain limits. Specifically, the debtor's unsecured debts and secured debts cannot exceed $2,750,000 as of the date of filing for bankruptcy relief. Additionally, the debtor must create a repayment plan that outlines how they will repay their debts over the course of three to five years. The process of filing for Chapter 13 bankruptcy involves several steps. The debtor must file a petition with the bankruptcy court, along with a repayment plan that outlines how they will repay their debts. They must also attend a meeting of creditors, where they will be asked questions about their financial situation. Once the court approves the repayment plan, the debtor will make regular payments to a trustee, who will then distribute the payments to the creditors. At the end of the repayment period, most remaining debts will be discharged. One of the benefits of Chapter 13 bankruptcy is that it allows the debtor to keep their assets, such as their home or car, as long as they can continue to make payments on them. It also provides a way to repay debts over a more extended period of time, which can make it more manageable for some debtors. However, it has several drawbacks as well. One of the biggest drawbacks is that the debtor must have a regular income to qualify for Chapter 13 bankruptcy. Additionally, the repayment plan can be complex and difficult to manage, and not all debts are dischargeable. It is a type of bankruptcy that is designed for businesses and individuals with significant debts. It allows the debtor to reorganize their debts and continue operating while they repay their creditors. Chapter 11 bankruptcy is a complex and expensive process, and it is usually only used by larger businesses or individuals with substantial assets. To be eligible for this type of bankruptcy, the debtor must be able to demonstrate that they can reorganize their debts and continue operating. The process of filing for Chapter 11 bankruptcy is complex and involves several steps. The debtor must file a petition with the bankruptcy court, along with a reorganization plan that outlines how they will repay their debts. They must also attend a meeting of creditors, where they will be asked questions about their financial situation. Once the court approves the reorganization plan, the debtor will make regular payments to a trustee, who will then distribute the payments to the creditors. At the end of the process, most remaining debts will be discharged. One of the benefits of Chapter 11 bankruptcy is that it allows businesses to continue operating while they reorganize their debts. It also provides a way to repay debts over a longer period of time, which can make it more manageable for some debtors. However, it has several drawbacks as well. One of the biggest drawbacks is that it is a complex and expensive process that can take years to complete. When choosing a type of bankruptcy, there are several factors to consider, such as the amount and type of debt, the debtor's income and assets, and their long-term financial goals. Chapter 7 bankruptcy is an option to consider for individuals with limited income and few assets who are looking for a quick and efficient way to eliminate unsecured debts. However, it involves liquidating assets, which can be a significant loss for the debtor. Additionally, not all debts are dischargeable in Chapter 7 bankruptcy. Chapter 13 bankruptcy is an option for individuals with a regular income and significant debt who are looking for a way to reorganize their debts and repay them over a longer period of time. It allows the debtor to keep their assets, such as their home or car, as long as they can continue to make payments on them. However, the repayment plan can be complex and difficult to manage, and not all debts are dischargeable. Chapter 11 bankruptcy is a good option for businesses and individuals with significant debts who are looking for a way to reorganize their debts and continue operating. However, it is a complex and expensive process that can take years to complete. Additionally, the debtor must be able to demonstrate that they can reorganize their debts and continue operating. Bankruptcy is a legal process that provides relief to individuals or businesses struggling with debt. There are three main types of bankruptcies: Chapter 7, Chapter 13, and Chapter 11. Each type of bankruptcy has its own eligibility requirements, process, benefits, and drawbacks. It is crucial to seek the advice of a qualified bankruptcy attorney before filing for bankruptcy to ensure that you make the best decision for your financial future. If you are experiencing financial difficulties and considering bankruptcy, it is essential to educate yourself and consult with a financial advisor. Take the time to learn about the eligibility requirements, benefits, and drawbacks of each type of bankruptcy. This will help you decide which bankruptcy is best suited for your particular situation. Remember, bankruptcy is not a decision that should be taken lightly, and it has long-term consequences that can affect your credit score and financial standing for years to come.Overview of Bankruptcy

Types of Bankruptcy

Chapter 7 Bankruptcy

Chapter 13 Bankruptcy

Chapter 11 Bankruptcy

Comparing the Different Types of Bankruptcy

Final Thoughts

Different Types of Bankruptcies FAQs

Bankruptcy is a legal process that permits individuals or businesses to eliminate or reorganize their debts when they are no longer able to pay them. Someone might consider filing for bankruptcy if they face overwhelming debt and impending foreclosure or experiencing other financial challenges.

There are three main types of bankruptcies: Chapter 7, Chapter 13, and Chapter 11. Each type of bankruptcy has its own eligibility requirements, process, benefits, and drawbacks.

Chapter 7 is known as a "liquidation" bankruptcy because it involves liquidating assets to pay off debts. To be eligible, the debtor must pass the "means test," which compares their income to the median income in their state.

Chapter 13 bankruptcy is a bankruptcy that allows individuals to reorganize their debts and repay them over a period of three to five years. To be eligible, the debtor must have a regular income, and their debts must be within certain limits.

When choosing a type of bankruptcy, several factors should be considered, such as the amount and type of debt, the debtor's income and assets, and their long-term financial goals. It is crucial to seek the advice of a qualified bankruptcy attorney before filing for bankruptcy to ensure that you make the best decision for your financial future.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.