Yes, it is possible to include student loans in a bankruptcy, but it's a complex and challenging process. Unlike other forms of debt, student loans aren't automatically considered for discharge. The debtor must prove in court that repaying the loans would cause them "undue hardship," a stringent standard often defined as an inability to maintain a minimal standard of living if forced to repay the loans. This hardship must be likely to persist for a significant portion of the repayment period, and the debtor must have made good-faith efforts to repay the loans. It's recommended to consult with a financial advisor or a bankruptcy attorney to understand the implications and alternatives before deciding to include student loans in bankruptcy. There are two primary types of student loans - federal and private. Federal student loans are funded by the U.S. government, and their terms and conditions, which are set by law, include many benefits not typically available with private loans. Conversely, private loans are provided by private organizations like banks, credit unions, and sometimes the schools themselves. The terms and conditions of these loans are set by the lender. Repayment of student loans presents several challenges. Federal loans typically offer a six-month grace period after graduation before repayment must begin. Private loans vary widely, with some requiring payments while still in school. Borrowers often face a complex range of repayment options. For example, federal loans offer several repayment plans, such as standard, extended, graduated, and income-driven plans, each with its terms and repayment period. The financial impact of student loans is profound, often leaving borrowers with significant financial distress. Student loans can limit borrowers' ability to attain financial milestones like homeownership or retirement savings. Furthermore, excessive student loan debt may lead to mental health problems due to constant worry about repayment. Bankruptcy can discharge many types of debts, but student loans are typically an exception. The general rule is that student loans cannot be discharged in bankruptcy unless repaying the loan would cause an "undue hardship" on the debtor. The "undue hardship" standard is a test used by courts to decide whether to discharge student loans in a bankruptcy case. However, the Bankruptcy Code does not specifically define what constitutes "undue hardship," leaving it to courts to decide on a case-by-case basis. The Bankruptcy Code considers student loans as "non-dischargeable" debts, meaning they cannot be eliminated through bankruptcy. This law has been in place since 1978, with the rationale that government or non-profit-funded education loans should be repaid to support the continuing availability of such funding for future students. "Undue hardship" is not specifically defined in the Bankruptcy Code. However, many courts interpret it to mean that the borrower cannot maintain a minimal standard of living if forced to repay the student loans. Moreover, the hardship must be expected to continue for a significant portion of the loan repayment period. To assess whether a borrower meets the "undue hardship" standard, many courts use the Brunner test. This three-pronged test examines whether the debtor cannot maintain a minimal standard of living, whether additional circumstances exist indicating that this state of affairs is likely to persist, and whether the debtor has made good faith efforts to repay the loans. Chapter 7 bankruptcy, also known as "liquidation bankruptcy," allows a debtor to discharge most of their debts. However, under this chapter, student loans are typically non-dischargeable unless the debtor can demonstrate undue hardship. Chapter 13 bankruptcy, also known as "wage earner's bankruptcy," involves the reorganization of a debtor's financial obligations. Here, student loans are considered non-priority unsecured debts. Although the debtor still owes these loans after the bankruptcy proceedings, Chapter 13 may lower the monthly payment during the repayment period. While both Chapter 7 and Chapter 13 treat student loans as non-dischargeable, key differences exist. Chapter 7 aims to wipe out the debtor's general unsecured debts without a repayment plan, while Chapter 13 involves developing a three- to five-year repayment plan before any remaining debt can be discharged. To seek discharge of student loans through bankruptcy, the borrower must initiate a separate action known as an adversary proceeding. The debtor must file a complaint in bankruptcy court, arguing that repaying the student loans would cause undue hardship. The borrower, in this case, acts as the plaintiff, with the lenders as the defendants. The court's role is to evaluate the evidence presented by both parties and determine whether the borrower meets the undue hardship standard. Given the complexity of these cases, legal representation is often necessary. However, securing legal aid can be challenging due to costs. Additionally, proving "undue hardship" can be difficult and requires detailed documentation of the borrower's financial situation. For borrowers who do not meet the undue hardship standard, there are other debt relief options. These alternatives may include deferment, forbearance, loan consolidation, and refinancing, each of which may provide temporary or permanent relief. Income-Driven Repayment (IDR) plans are an alternative to federal student loans. These plans calculate payments based on income and family size, which can make monthly payments more manageable for those with lower incomes. Loan forgiveness programs provide another avenue for eligible borrowers to alleviate student loan debt. For instance, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on Direct Loans after the borrower has made 120 qualifying payments under a qualifying repayment plan while working full-time for a qualifying employer. While student loans represent a significant financial burden, discharging them through bankruptcy is a complex process, hinged on the stringent "undue hardship" standard. Federal and private loans offer varying terms, and the burden of repayment often creates a profound impact on borrowers' financial and mental well-being. While bankruptcy can relieve many debts, student loans are considered non-dischargeable, except in rare cases of demonstrated undue hardship. These exceptions are evaluated in separate adversary proceedings within the bankruptcy case. The different types of bankruptcy - Chapter 7 and Chapter 13 - treat student loans differently, but both still present significant hurdles for discharging student loan debt. For those who can't meet the undue hardship standard, alternatives such as deferment, forbearance, loan consolidation, refinancing, Income-Driven Repayment plans, and loan forgiveness programs can provide other pathways to debt relief.Can You Put Student Loans in a Bankruptcy?

Understanding Student Loans

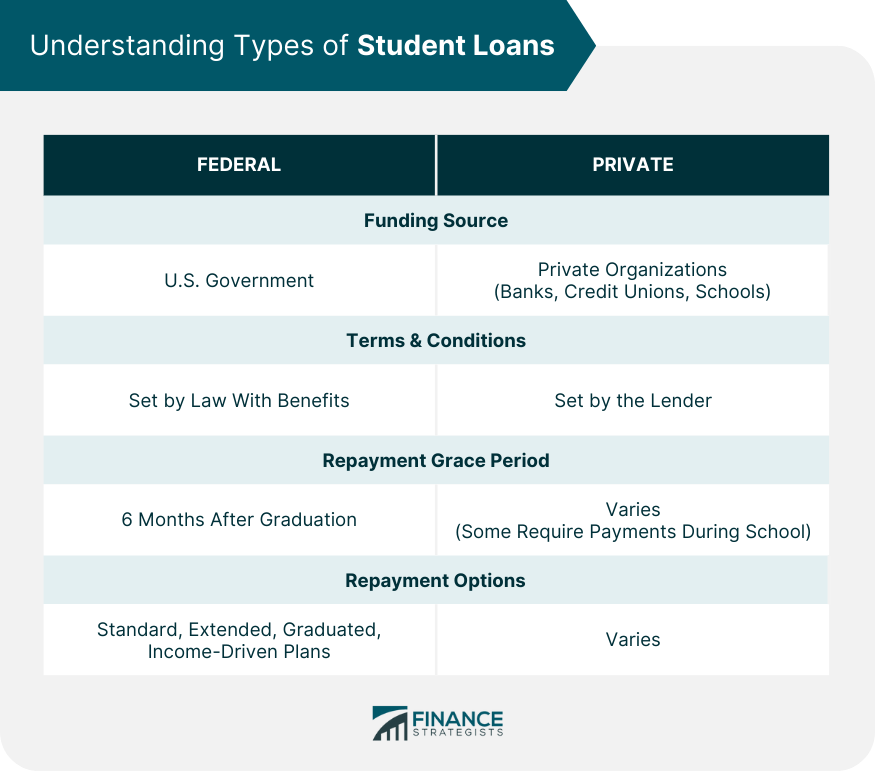

Different Types of Student Loans

Repayment Options and Challenges for Borrowers

Impact of Student Loan Debt on Borrowers' Financial Well-being

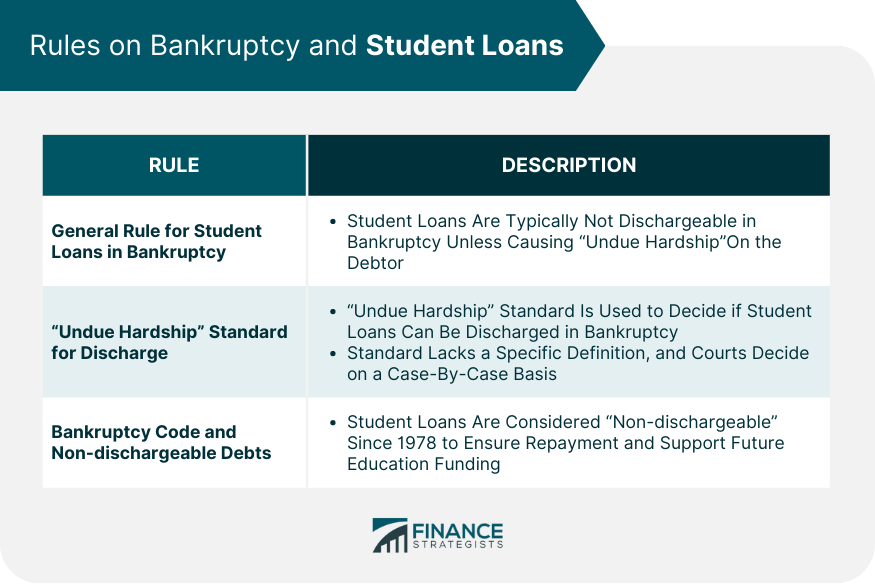

Rules on Bankruptcy and Student Loans

General Rule Regarding Student Loans in Bankruptcy

"Undue Hardship" Standard for Discharging Student Loans

Bankruptcy Code and Non-dischargeable Debts

Undue Hardship Exception

Definition and Application to Student Loans

Criteria Used by Courts

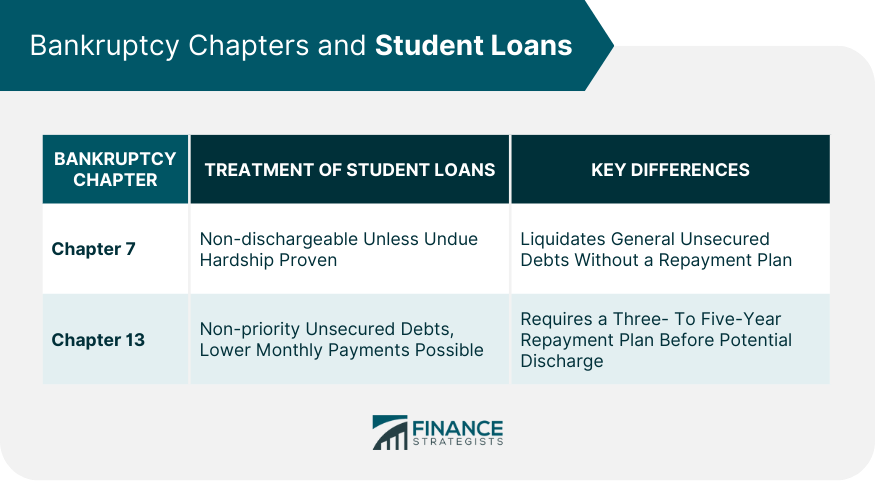

Bankruptcy Chapters and Student Loans

Treatment of Student Loans in Chapter 7 Bankruptcy

Treatment of Student Loans in Chapter 13 Bankruptcy

Differences Between the Chapters

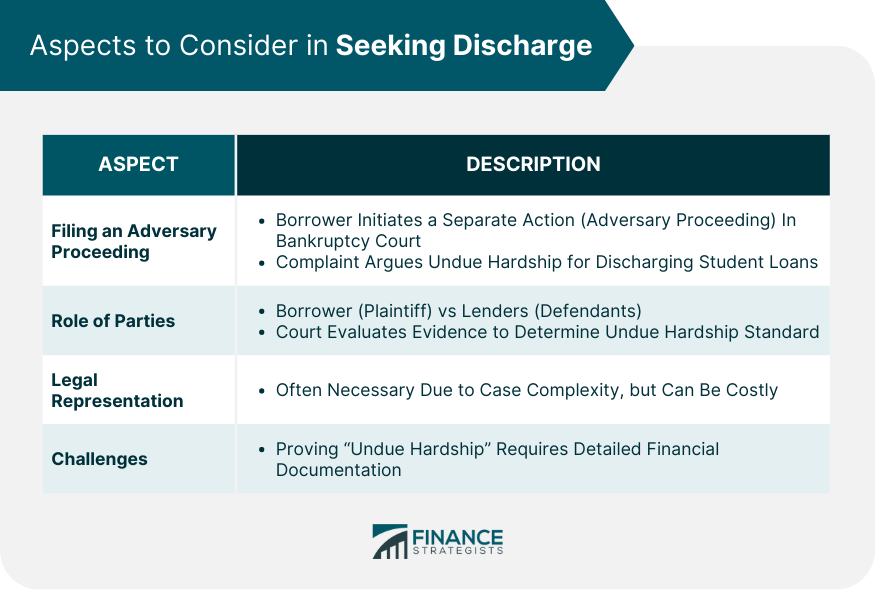

Seeking Discharge

Filing an Adversary Proceeding

Role of the Borrower, Lenders, and the Court

Legal Representation and Challenges

Alternatives to Discharge

Other Debt Relief Options

Income-Driven Repayment Plans

Loan Forgiveness Programs

Bottom Line

Can You Put Student Loans in a Bankruptcy? FAQs

Federal student loans are funded by the U.S. government, and their terms, conditions, and benefits are set by law. Private loans, on the other hand, are provided by private organizations such as banks and credit unions, and their terms and conditions are set by the lender.

"Undue hardship" is a legal standard used to determine whether a borrower can discharge student loans in bankruptcy. It generally means that the borrower cannot maintain a minimal standard of living if forced to repay the student loans, and the hardship is expected to persist for a significant portion of the loan repayment period.

Both types of bankruptcy generally consider student loans as non-dischargeable. Chapter 7, known as "liquidation bankruptcy," wipes out most debts without a repayment plan, but student loans can only be discharged if the borrower demonstrates undue hardship. Chapter 13, "wage earner's bankruptcy," involves a three- to five-year repayment plan for the debts, after which any remaining debt may be discharged.

An adversary proceeding is a separate legal action within the bankruptcy case initiated by the debtor to argue that repaying the student loans would cause undue hardship. The borrower (plaintiff) and lenders (defendants) present their evidence, and the court decides if the undue hardship standard is met.

Alternatives include deferment or forbearance (temporarily postponing or reducing your loan payments), loan consolidation (combining multiple loans into one for a single monthly payment), and refinancing (replacing your loan with a new one with different terms). Income-Driven Repayment plans and loan forgiveness programs are also available for federal student loans.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.