When contemplating filing for bankruptcy, a key hurdle that many individuals face is the seeming paradox of needing money to declare that you have none. However, it is possible to navigate these waters, and understanding the implications of this move is a crucial first step. Bankruptcy is a legal process where a person who cannot pay their creditors can seek relief from some or all of their debts. However, the process of declaring bankruptcy is not free. There are court costs, credit counseling fees, and attorney's fees. Additionally, individuals considering bankruptcy should be aware that the type of bankruptcy they file for will determine the extent of their debt relief and the impact on their assets. Bankruptcy costs can include the filing fee, which for Chapter 7 bankruptcy is around $335, and for Chapter 13 is approximately $310. Credit counseling and debtor education courses are also required and can cost between $20 and $100 each, though fee waivers may be available. Lastly, attorney fees can vary greatly, often ranging from $1,000 to $3,700, depending on the complexity of the case and your location. These costs, while intimidating, should not deter those in desperate need of financial relief. Understanding the types of bankruptcy you can file for and their processes can help determine the best route to take when you have no money. There are options available even when funds are scarce, and making an informed choice can ease the process. Chapter 7 bankruptcy is often referred to as "liquidation bankruptcy." It allows you to erase most if not all, of your debt by liquidating your non-exempt assets. However, it is essential to meet certain criteria to be eligible for this form of bankruptcy. To qualify for Chapter 7, your disposable income must be low enough to pass the "means test." If your income is below the median for your state, you automatically pass. If it's above, other factors come into play, like your expenses and specific types of debt. Understanding your financial position in detail can make this process smoother. If you pass the means test, you can file for Chapter 7. You'll need to complete the required credit counseling and then file a petition with the bankruptcy court. If you cannot afford the filing fee, you can apply to have it waived or paid in installments. Even with limited resources, options exist to ensure you can access this legal recourse. In contrast to Chapter 7, Chapter 13 involves a repayment plan that lets you repay some or all your debt over three to five years. It's a different approach to handling bankruptcy and one that suits some people better, depending on their circumstances. Chapter 13 requires that you have a regular income and have debt within certain limits. As of 2023, your secured debts and unsecured debts cannot exceed $2,750,000 as of the date of the bankruptcy filing. Knowing these limits can help you decide whether this path is feasible. If you qualify, you'll propose a repayment plan based on your income, living expenses, and debt. If approved by the court, you'll make regular payments to a bankruptcy trustee who then distributes the funds to your creditors. You may be able to include the costs of bankruptcy in your repayment plan. It's an option that provides an organized approach to tackling your debts. Before diving into bankruptcy, consider these alternatives, which could provide a path to financial stability without the stigma and long-term impact of bankruptcy. It's often better to explore all possible avenues before committing to such a significant decision. Under a debt management plan, you'll work with a credit counselor to create a repayment plan with your creditors. You'll make regular payments to the counseling agency, which in turn pays your creditors. It's a structured approach that can make a substantial difference if you're overwhelmed by multiple debts. Some creditors may be willing to negotiate reduced payments, lower interest rates, or even a reduction in the total amount you owe. This approach requires communication and negotiation skills, but it can pay off significantly by reducing your financial burden. Debt settlement is a more drastic form of negotiation, where you or a company working on your behalf negotiate with your creditors to let you pay a "settlement" to resolve your debt — typically less than you owe. While this can substantially reduce your debt, it's essential to consider the potential impact on your credit score. The process of declaring bankruptcy can be complex and tricky to navigate, but there are resources available to help you. Even with a limited budget, there are avenues to seek professional advice. Several organizations provide free or low-cost legal services to those in need. Look into options like Legal Aid, pro bono services from bankruptcy attorneys, and law school clinics. Just because you're facing financial difficulties does not mean you need to face the legal process alone. Numerous non-profit organizations provide free credit counseling services and can help you understand your options. Government programs are also available to provide assistance. Leveraging these resources can lighten your burden and provide much-needed guidance. A bankruptcy attorney can guide you through the process, helping ensure paperwork is completed accurately, representing you in court, and negotiating with creditors. Despite the associated costs, an attorney's expertise can be invaluable, saving you time and potentially more money in the long run. Even with little to no money, there are steps you can take to prepare for the bankruptcy process. Preparation can significantly reduce stress and ensure that you navigate the process as smoothly as possible. You'll need to gather financial documents, such as pay stubs, bank statements, tax returns, and information about your debts. You'll use this information to complete the bankruptcy forms. Even when facing bankruptcy, organization can simplify the process and save you from future headaches. You must complete credit counseling from a government-approved organization within six months before you file for bankruptcy. It's an opportunity to evaluate your personal financial situation and explore realistic budgeting and other alternatives to bankruptcy. This step is not just a requirement but can also be a valuable educational tool. After you file your paperwork, a court-appointed bankruptcy trustee will schedule a meeting of creditors. It's usually a short and straightforward process, but you will be put under oath, and the trustee and creditors may ask you questions about your financial status and property. It's a pivotal part of the bankruptcy process and one that demands honesty and transparency. The road to financial recovery post-bankruptcy can be challenging, but by taking the right steps, you can reestablish your financial footing. Bankruptcy is not the end of your financial life but a chance for a fresh start. Post-bankruptcy, rebuilding your credit is crucial. It can be a slow process, but with patience and good financial habits, you can improve your credit score over time. Gradual improvement can open up opportunities for better financial options in the future. Creating and sticking to a budget is a key part of regaining financial stability after bankruptcy. This includes regular savings and living within your means. A sustainable budget is the cornerstone of a secure financial future. Learning from past mistakes and making strategic financial plans for the future can help avoid landing back in the same predicament. Effective planning can shield you from financial pitfalls and set you up for a stable financial future. Filing for bankruptcy without money may seem like a daunting task, but it is possible to navigate the process with the right knowledge and resources. Understanding the costs associated with bankruptcy, exploring alternative options, and seeking legal help are essential steps to consider. Additionally, exploring alternatives such as debt management plans, negotiating with creditors, or debt settlement can provide alternative paths to financial stability. It is crucial to be prepared by gathering necessary documents, completing credit counseling, and attending the meeting of creditors. Remember that bankruptcy is not the end but rather an opportunity for a fresh start. Rebuilding credit, establishing a sustainable budget, and engaging in future financial planning are key steps toward regaining financial stability. While facing these challenges, it is highly recommended to seek the guidance of a financial advisor who can provide personalized assistance throughout the bankruptcy process and beyond.Overview of Filing Bankruptcy

Costs Associated With Filing Bankruptcy

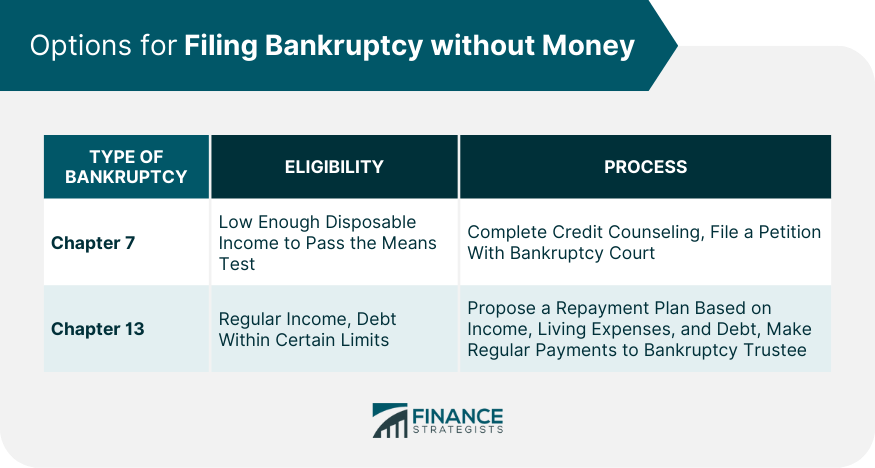

Options for Filing Bankruptcy Without Money

Chapter 7 Bankruptcy

Eligibility Criteria

Process of Filing Chapter 7 Without Money

Chapter 13 Bankruptcy

Eligibility Criteria

Process of Filing Chapter 13 Without Money

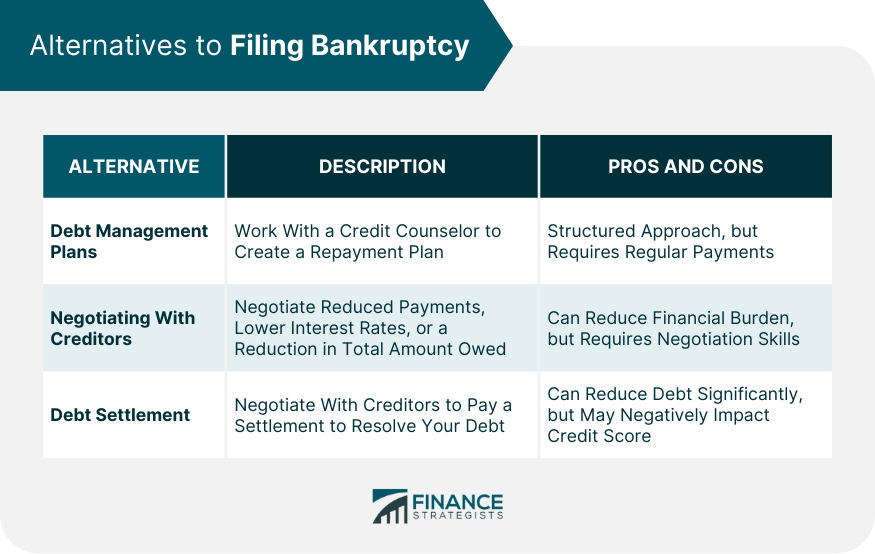

Alternatives to Filing Bankruptcy

Debt Management Plans

Negotiating With Creditors

Debt Settlement

Getting Legal Help When Filing for Bankruptcy

Finding Low-Cost or Free Legal Help

Non-profit Organizations and Government Programs

Role of a Bankruptcy Attorney

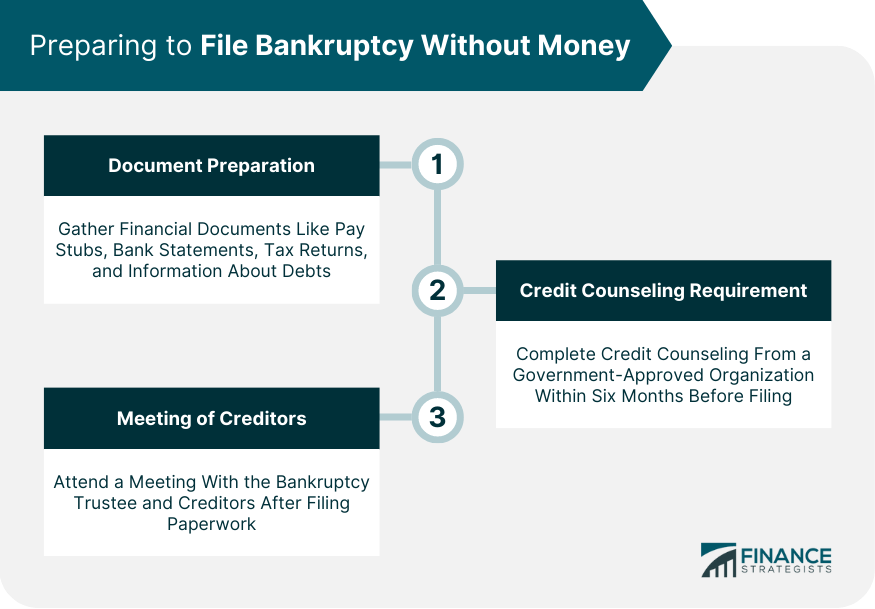

Preparing to File Bankruptcy Without Money

Document Preparation

Credit Counseling Requirement

Meeting of Creditors

Life After Bankruptcy

Rebuilding Your Credit

Establishing a Sustainable Budget

Future Financial Planning

The Bottom Line

Filing Bankruptcy Without Money FAQs

Costs include filing fees, credit counseling fees, and attorney's fees. You might apply for fee waivers or payment installments.

If you pass the means test, you can file for Chapter 7. You may apply to have the filing fee waived or paid in installments.

Alternatives include debt management plans, negotiating with creditors, or debt settlement.

You can seek free or low-cost legal help from organizations like Legal Aid, pro bono services from bankruptcy attorneys, and law school clinics.

Prepare your financial documents, complete the required credit counseling, and be ready for the meeting of creditors.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.