Bankruptcy law, a subset of insolvency law, is a legal status of a person or an entity that cannot repay the debts it owes to creditors. This status is often imposed by a court order initiated by the debtor. The primary purpose of bankruptcy law is to give a person who is burdened with debt a fresh start by wiping out his or her debts. Understanding bankruptcy law is vital for both creditors and debtors. For the debtor, knowledge of the law can provide a lifeline in desperate financial times, while for the creditor, it can aid in asset recovery and risk management. The concept of bankruptcy has been around for centuries and has evolved significantly over time. In ancient times, insolvency or inability to pay one's debt was considered a crime, and debtors were often subjected to harsh punishments. However, as society evolved, so did the perception of bankruptcy. During the Roman Empire, bankruptcy was still considered a crime, and debtors could be subjected to servitude. However, by the Middle Ages, societies began to view bankruptcy differently, recognizing that debtors, too, needed protection. This led to the introduction of laws that offered some relief for debtors. In the United States, the evolution of bankruptcy laws began in the 19th century. The Bankruptcy Act of 1898, often called the "Nelson Act," established uniform laws on the subject of bankruptcies throughout the United States, which served as the basis of modern bankruptcy law. Bankruptcy laws differ for individuals and corporations due to the nature of debts and operations. Individual bankruptcy, also known as personal bankruptcy, refers to the legal process that a person undergoes when he or she can't pay back their debts. Personal bankruptcy can provide a fresh start for the debtor, but it also impacts their credit history. On the other hand, corporate bankruptcy is a legal proceeding initiated by a business that cannot pay its debts. The aim is to give the company a chance to restructure its debts and, if possible, to continue operations. If restructuring is not possible, the business may be liquidated to pay off creditors. Chapter 7 bankruptcy, also known as "liquidation bankruptcy," is the most common form of bankruptcy in the United States. It is usually chosen by individuals who have little to no disposable income. In Chapter 7 bankruptcy, a debtor's non-exempt assets are sold by the trustee, and the proceeds are used to pay off creditors. It's important to note that not all assets are liquidated in this process. Certain properties, deemed as "exempt," are protected under bankruptcy law and cannot be sold off to pay creditors. To file for Chapter 7 bankruptcy, the debtor must qualify by passing the "means test." This test compares the debtor's monthly income to the median income in their state for a household of the same size. Once a debtor files for Chapter 7 bankruptcy, an "automatic stay" comes into effect, which stops most collection actions against the debtor. The court appoints a trustee, who takes control of the debtor's assets, selling non-exempt assets to pay back creditors. While Chapter 7 bankruptcy allows for the discharge of most debts, some types of debts, like student loans, child support, and tax debts, are not dischargeable. In most cases, the bankruptcy stays on the debtor's credit report for ten years, significantly impacting their credit score and ability to secure future credit. However, despite these implications, Chapter 7 bankruptcy can provide a clean financial slate for individuals buried under insurmountable debt, allowing them to start afresh. Chapter 11 bankruptcy is a form typically filed by corporations and partnerships. It can also be filed by individuals with substantial debts and assets. It allows entities to restructure their debts and obligations while remaining in operation. Chapter 11 is often referred to as a "reorganization" bankruptcy. The debtor, often a business entity, restructures its debts under a plan of reorganization to keep its business alive and pay creditors over time. There's no limit to the amount of debt a Chapter 11 debtor can have. Any business, whether it's a large corporation, a small business, or an individual who fits into the financial parameters, can file for Chapter 11. Filing for Chapter 11 triggers an automatic stay, stopping most collection attempts. The debtor then proposes a reorganization plan. This plan categorizes creditors according to the nature and security of their claims and how they'll be treated during bankruptcy. Creditors and the court must approve the plan, and if approved, the debtor continues to operate and function under supervision while implementing the plan. If the debtor can't propose a plan or if the proposed plan isn't accepted, the court can either convert the case to a Chapter 7 bankruptcy or dismiss it altogether. Chapter 13 bankruptcy is designed for individual debtors with regular income who would like to pay all or part of their debts in installments over a period of time. Chapter 13 bankruptcy, often termed "wage earner's bankruptcy," allows the debtor to keep their property and pay off their debts over time. The debtor must have a regular income and propose a plan to repay all or a portion of their debts over a three to five-year period. The debtor is eligible for Chapter 13 if their unsecured debts are less than a certain amount and their secured debts are also under a specified limit. These amounts are adjusted periodically to reflect changes in the consumer price index. The crux of Chapter 13 bankruptcy is the repayment plan. The debtor proposes a plan to repay creditors over the specified period. The plan must be approved by the court and overseen by a court-appointed trustee. At the end of the repayment period, the remaining debts are discharged, meaning the debtor is no longer legally required to pay them. However, some debts, like alimony, child support, certain taxes, and student loans, are not dischargeable. The first role of a bankruptcy lawyer is to assist the debtor in determining whether to file for bankruptcy and, if so, under which chapter. The lawyer will consider the client's financial situation, the nature of the debts, and the client's long-term financial goals. The bankruptcy lawyer guides the debtor through each step of the bankruptcy process, from preparing and filing the necessary paperwork to representing the debtor in court hearings. The lawyer ensures that the debtor understands their rights and obligations, the progress of the bankruptcy case, and the potential implications and outcomes. Bankruptcy can significantly impact an individual's or business's financial health. The immediate impact of bankruptcy is relief from debt pressure. The automatic stay stops most collection actions, and creditors can no longer contact the debtor. However, bankruptcy also has immediate negative impacts. It significantly lowers the debtor's credit score and stays on their credit report for seven to ten years. In the long term, bankruptcy can make it difficult to obtain credit, buy a home, or even get a job. It may also increase insurance premiums. However, these effects lessen over time, and there are steps a debtor can take to rebuild credit and financial health after bankruptcy. These include paying bills on time, creating a budget, and regularly reviewing credit reports. The road to recovery after bankruptcy involves a commitment to sound financial habits. Here are a few steps that can aid in this process: Budgeting: Create a realistic budget and stick to it. A budget can help you manage your income and expenses, preventing you from falling back into debt. Emergency Savings: Build an emergency fund to cover unexpected expenses. This fund acts as a safety net, reducing the likelihood of incurring debt due to unforeseen circumstances. Rebuild Credit: Obtain a secured credit card or a credit-builder loan to start rebuilding your credit. Always pay on time and keep the balance low. Monitor Credit Report: Regularly review your credit reports to ensure accuracy and track your progress. You can dispute any errors that you find. Financial planning post-bankruptcy is crucial. It involves setting financial goals, creating a plan to achieve them, and regularly reviewing and updating the plan. Financial planning can involve budgeting, investment planning, retirement planning, and estate planning. Working with a financial advisor can be helpful, especially when navigating the complexities of financial planning after bankruptcy. They can guide you in making sound financial decisions and assist in creating a plan tailored to your needs and goals. Bankruptcy law is a crucial component of insolvency law, offering a fresh financial start to those beleaguered by overwhelming debts. It is divided into different facets, including individual and corporate bankruptcy, each serving its unique purpose in managing financial crises. Grasping these legal intricacies is crucial for debtors seeking financial reprieve and creditors looking for asset recovery and risk management. Bankruptcy brings about significant repercussions on financial health, with immediate impacts on credit scores and long-term implications for credit access. Nevertheless, the journey post-bankruptcy is recoverable with the right steps like budgeting, saving, credit rebuilding, and vigilant credit report monitoring. Consulting a financial advisor or a bankruptcy lawyer can help you understand your options better, evaluate the impacts, and make informed decisions that align with your financial goals.What Is the Bankruptcy Law?

Historical Perspective of Bankruptcy Law

Understanding Different Types of Bankruptcy

Individual Bankruptcy

Corporate Bankruptcy

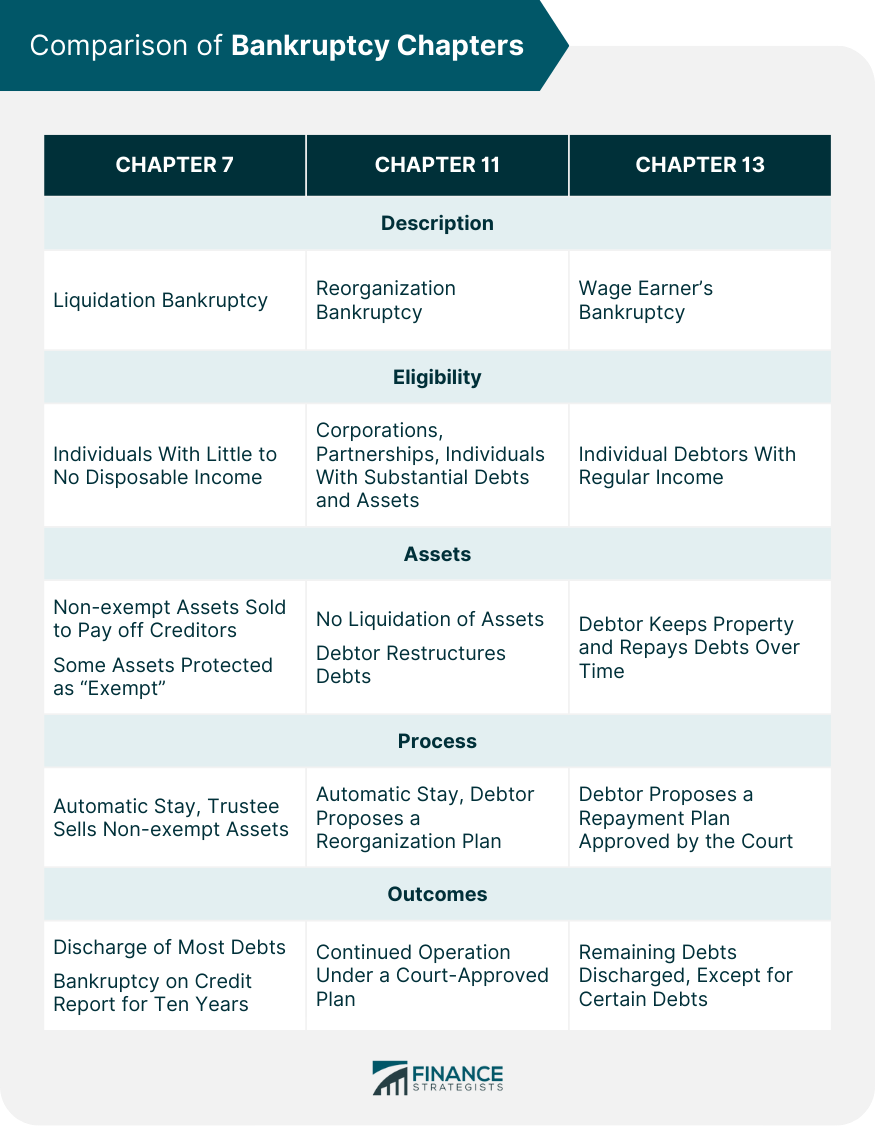

Bankruptcy Law: Chapter 7

Explanation and Eligibility

Process and Potential Outcomes

Bankruptcy Law: Chapter 11

Explanation and Eligibility

Process and Restructuring Plans

Bankruptcy Law: Chapter 13

Explanation and Eligibility

Repayment Plans and Discharge

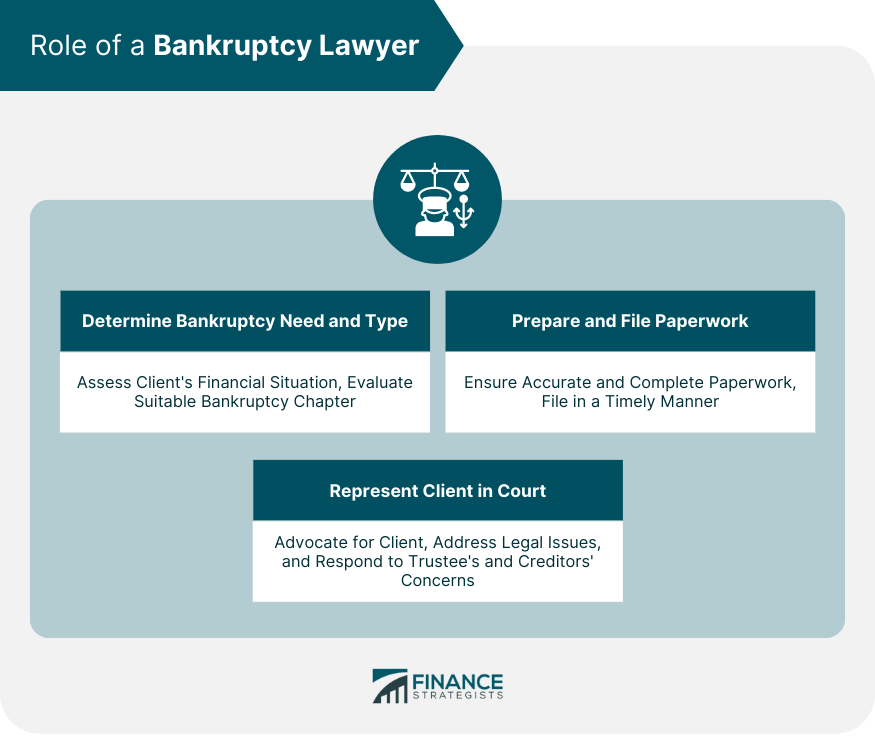

Role of a Bankruptcy Lawyer

Assist in Filing for Bankruptcy

Guidance Throughout the Process

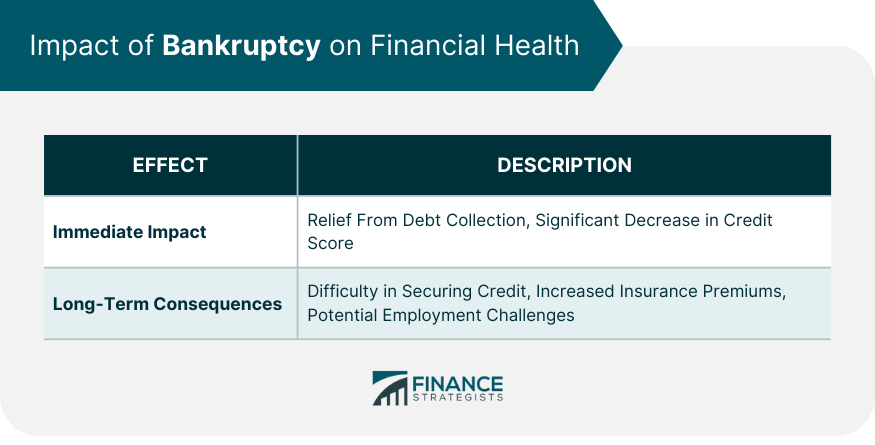

Impact of Bankruptcy on Financial Health

Immediate Effects

Long-Term Consequences

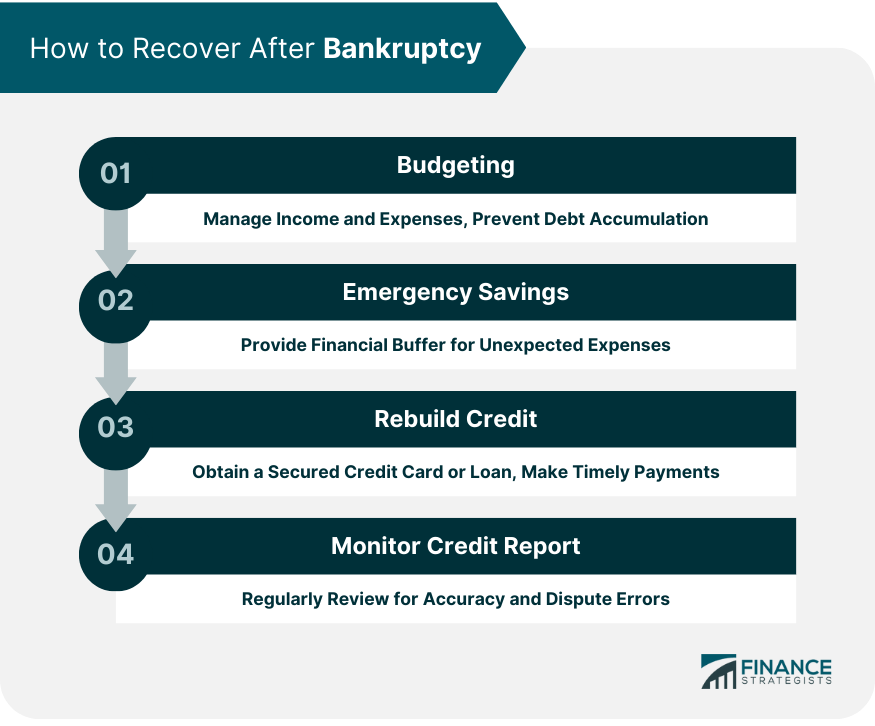

How to Recover After Bankruptcy

Importance of Financial Planning

Final Thoughts

Bankruptcy Law FAQs

Bankruptcy law provides a legal process for individuals or businesses that cannot repay their debts to creditors. It aims to offer debt relief and a fresh financial start.

The main types of bankruptcy include Chapter 7, focusing on the liquidation of assets; Chapter 11, offering businesses a chance to reorganize debts; and Chapter 13, allowing individuals to create a repayment plan.

A bankruptcy lawyer guides clients through the bankruptcy process, from determining whether to file and under which chapter to preparing the necessary paperwork and representing the client in court.

Bankruptcy significantly affects a debtor's credit score, making it challenging to secure credit, purchase a home, or even find employment. However, these effects lessen over time with sound financial habits.

Post-bankruptcy financial planning is crucial to rebuilding financial health. It involves setting financial goals, creating a budget, rebuilding credit, and regularly monitoring credit reports.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.