A 401k is a retirement savings plan sponsored by an employer. It allows workers to save and invest a portion of their paycheck before taxes are taken out. The main appeal of 401k is its tax advantages - taxes aren’t paid on the money until it is withdrawn from the account. On the other hand, bonds are fixed-income instruments that represent a loan made by an investor to a borrower, usually corporate or governmental. When you purchase a bond, you're effectively lending money to the issuer in exchange for periodic interest payments and the return of the bond's face value when it matures. Bonds play an integral part in any well-diversified investment portfolio. They're often seen as safer than stocks because if you hold them until maturity, you will get all your initial investment back in addition to the interest earned. However, like any financial decision, moving a 401k entirely into bonds should not be taken lightly. Generally, the younger you are, the more risk you can afford to take. This is because you have more time to recover from any potential losses. Conversely, as you get closer to retirement, preserving capital becomes a priority. Bonds, with their lower risk profile and consistent return, can be attractive in this situation. Some people can stomach major market swings, while others lose sleep over minor fluctuations. It's essential to honestly assess your risk tolerance and ensure it aligns with your financial goals. If you are risk-averse or looking for stable income in retirement, bonds could be a suitable choice. The broader economic situation and interest rates can greatly impact the decision to move a 401k into bonds. When interest rates are high, newly issued bonds will have higher yields, making them more attractive. However, in a low-interest-rate environment, bonds may not provide the desired returns. Anytime you take money out of a traditional 401k before age 59 1/2, the withdrawal is subject to both ordinary income taxes and a 10% early withdrawal penalty. It's crucial to consult with a tax professional to understand all potential tax implications fully. Usually, bonds have lower returns than stocks. In an environment with high inflation, the returns from bonds may not keep up with inflation, reducing purchasing power over time. Bonds, especially government and high-grade corporate bonds, are often less volatile than stocks. Therefore, an investment in bonds could provide a smoother and more predictable path to your financial goals, particularly if you're nearing retirement and have a lower risk tolerance. When you buy a bond, the issuer agrees to pay you a specified rate of interest over a set period, and then, when the bond matures, return the principal to you. This feature can make bonds attractive to retirees looking for a predictable income stream to fund their post-working life. Bonds, especially those with high credit ratings, offer a degree of predictability and reliability that can be appealing. If a bond issuer doesn't default, you know exactly how much you'll receive and when you'll get it. This predictability can help with financial planning and provide a level of comfort not always available with other investments. While bonds are generally less risky than stocks, they also usually offer lower returns. Over the long term, this could result in a smaller nest egg at retirement. If you are many years away from retirement, it may be worthwhile to endure the additional volatility that comes with stocks in exchange for potentially higher returns. Unlike stocks, bonds do not offer the potential for capital appreciation. The best-case scenario for a bondholder is that the issuer makes all scheduled interest payments and repays the principal in full at maturity. This characteristic may make it harder to achieve your financial goals, particularly if you have a long investment horizon. There is always the risk that the bond issuer could default, leaving bondholders without their expected interest payments or even their original investment. Additionally, bonds are sensitive to interest rates. When interest rates rise, the price of existing bonds falls. This could lead to losses if you need to sell a bond before it matures. An alternative to moving an entire 401k to bonds is to adopt a balanced portfolio approach. This allows for potential growth from stocks, while bonds can provide income and reduce portfolio volatility. The right combination depends on your individual risk tolerance, financial goals, and investment horizon. Target-date funds are a type of mutual fund that automatically adjusts the asset mix over time based on a selected retirement date. Early on, they're heavily weighted towards riskier investments like stocks, but as the target date approaches, the fund automatically shifts towards safer assets like bonds. This can be a good alternative if you're looking for a hands-off approach to retirement investing. It involves investing in different types of bonds with varying maturities, yields, and credit qualities. By doing this, you can potentially maximize returns, minimize risk, and ensure a steady cash flow. A bond ladder is a strategy where you invest in several bonds with different maturity dates. As each bond matures, you reinvest the principal into a new bond. This can be an effective way to manage interest rate risk, as you'll be regularly investing in new bonds that should reflect current market interest rates. Given the complexity and potential implications of moving a 401k to bonds, it's advisable to seek advice from a financial professional. They can provide personalized advice based on your individual circumstances and help you understand the potential risks and rewards. This includes thinking about how long you expect to live, the lifestyle you want to have in retirement, and potential healthcare costs. You should also consider other sources of retirement income, like Social Security or pensions. The investment decisions you make today can have a significant impact on your lifestyle in retirement. It's essential to consider how different scenarios could affect your ability to afford the things you want to do in retirement, like travel, hobbies, or helping family members financially. The decision to move a 401k entirely into bonds should be carefully considered, taking into account several key considerations, like age, retirement timeline, risk tolerance, financial goals, the current economic climate, interest rates, tax implications, and inflation rates. While bonds offer advantages such as lower volatility, steady income generation, predictability, and reliability, there are potential drawbacks to consider, including lower potential returns, limited growth potential, and the risk of bond defaults and interest rate fluctuations. For those seeking a balanced approach, maintaining a mix of stocks and bonds or considering target-date funds can provide the potential for growth while reducing volatility. Diversifying within bond investments and utilizing a laddering strategy can also be effective in managing risk and optimizing returns. Long-term financial planning strategies and considering the impact on retirement lifestyle are essential aspects to contemplate when making investment decisions. It is crucial to consult a financial advisor or other finance professionals to understand the individual implications and make informed decisions based on personal circumstances. 401k and Bonds: Overview

Understanding 401k

Bonds and Their Role in Investment

Key Factors and Considerations in Moving 401k to Bonds

Age and Retirement Timeline

Risk Tolerance and Financial Goals

Current Economic Climate and Interest Rates

Tax Implications and Potential Penalties

Current and Projected Inflation Rates

Potential Benefits of Moving 401k to Bonds

Lower Volatility and Risk Management

Steady Income Generation

Predictability and Reliability

Potential Drawbacks of Moving 401k to Bonds

Lower Potential Returns Compared to Stocks

Lack of Growth Potential

Risks Associated With Bonds

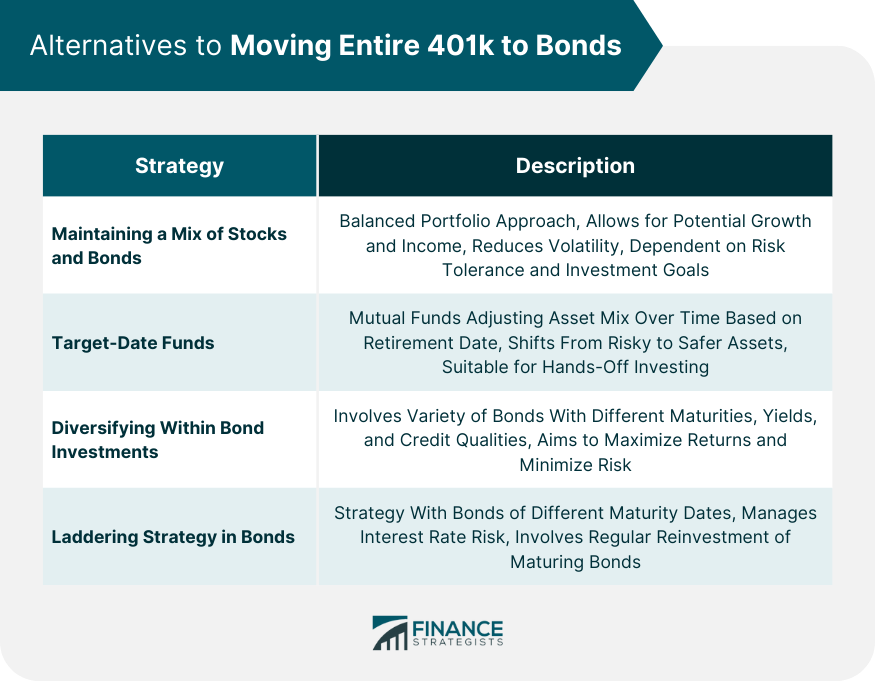

Alternatives to Moving Entire 401k to Bonds

Maintaining a Mix of Stocks and Bonds

Target-Date Funds

Diversifying Within Bond Investments

Laddering Strategy in Bonds

Additional Tips in Deciding to Move 401k to Bonds

Seek Professional Financial Advice

Use Long-Term Financial Planning Strategies

Gauge Potential Impact on Retirement Lifestyle

The Bottom Line

Should I Move 401k to Bonds? FAQs

Moving your 401k to bonds can offer benefits such as lower volatility and risk management, steady income generation, and predictability. Bonds, especially government and high-grade corporate bonds, are often less volatile than stocks, providing a smoother path to your financial goals, particularly if you have a lower risk tolerance or are nearing retirement.

One potential drawback is the lower potential returns compared to stocks. While bonds are generally less risky, they typically offer lower returns, which could result in a smaller retirement nest egg over the long term. Additionally, bonds lack the growth potential of stocks and are subject to the risk of default by the bond issuer.

Yes, there are alternatives to consider. One option is to maintain a balanced portfolio that includes a mix of stocks and bonds, allowing for potential growth from stocks while bonds provide income and reduce portfolio volatility. Another alternative is investing in target-date funds, which automatically adjust the asset mix based on your selected retirement date.

Besides the potential benefits and drawbacks of moving your 401k to bonds, it is important to consider factors such as your long-term financial planning strategies, including expected lifespan, desired retirement lifestyle, and potential healthcare costs. It is also crucial to evaluate the impact on your retirement lifestyle and whether it aligns with your goals and financial needs. Seeking advice from a financial professional can help you assess all these factors and make an informed decision.

To minimize risk, you can adopt diversification strategies within bond investments. This involves investing in different types of bonds with varying maturities, yields, and credit qualities. By diversifying, you can potentially maximize returns, minimize risk, and ensure a steady cash flow. Another strategy is to utilize a bond laddering approach, where you invest in bonds with different maturity dates, spreading out the risk and managing interest rate fluctuations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.