Tax credits are a type of financial incentive offered by the government to reduce an individual's or a company's tax liability. They directly reduce the amount of tax owed, dollar-for-dollar, as opposed to tax deductions, which lower the amount of taxable income. Tax credits play a significant role in promoting specific behaviors or supporting specific groups, such as low-income families, students, or businesses investing in research and development. They help reduce the tax burden on taxpayers, which can increase disposable income, stimulate economic growth, and promote social welfare. Non-refundable tax credits are tax credits that can only reduce a taxpayer's liability to zero. If the credit amount exceeds the tax owed, the excess will not be refunded to the taxpayer. These credits help lower the tax burden, but if a taxpayer has little to no tax liability, they may not benefit fully from non-refundable tax credits. Refundable tax credits, on the other hand, allow taxpayers to receive a refund if the credit amount exceeds their tax liability. This means that even if a taxpayer owes no tax, they can still receive the excess credit as a refund, providing additional financial support to individuals and families who may need it most. Hybrid tax credits combine elements of both refundable and non-refundable tax credits. A portion of the credit may be refundable, while the remainder is non-refundable. This structure provides a balance between offering financial support to taxpayers and limiting the potential cost to the government. Eligibility criteria for tax credits vary depending on the specific credit in question. Some credits may be available only to individuals or families with children, while others may target specific industries or activities, such as research and development. Taxpayers must meet the specific requirements for each credit to qualify. Many tax credits have income requirements, which may include income limits or phase-out ranges. These provisions are designed to ensure that the benefits of the tax credits are targeted at the intended recipients, such as low- and moderate-income individuals and families. Taxpayers are often required to provide documentation to support their eligibility for tax credits. This may include proof of income, expenses related to the credit, or other necessary documentation as specified by the tax credit's rules and regulations. The Earned Income Tax Credit (EITC) is a refundable tax credit designed to help low- to moderate-income working individuals and families. The credit amount varies based on the taxpayer's income, filing status, and number of qualifying children. The Child Tax Credit (CTC) is a partially refundable tax credit that provides financial assistance to families with qualifying children. The credit amount depends on the taxpayer's income and the number of eligible children. The American Opportunity Tax Credit (AOTC) is a partially refundable tax credit that helps eligible students and their families offset the cost of higher education. It applies to the first four years of post-secondary education and is based on the amount of qualified education expenses, such as tuition and fees. The Lifetime Learning Credit (LLC) is a non-refundable tax credit that helps taxpayers offset the cost of higher education for themselves, their spouses, or their dependents. The credit is available for any level of post-secondary education and has no limit on the number of years it can be claimed. The Retirement Savings Contributions Credit (Saver's Credit) is a non-refundable tax credit that encourages low- to moderate-income taxpayers to save for retirement by contributing to eligible retirement plans. The credit is based on a percentage of the taxpayer's eligible contributions and is subject to income limitations. Some tax credits have phase-out limits, which reduce or eliminate the credit's benefit for taxpayers with higher incomes. As a taxpayer's income increases within the specified phase-out range, the credit amount gradually decreases, ensuring that the benefits of the credit are targeted at those who need it most. Income limits are another common restriction for tax credits, setting a maximum income level beyond which a taxpayer is no longer eligible for the credit. These limits help to direct the benefits of the tax credit to the intended recipients, often low- and moderate-income taxpayers. The timing of claims can also impact a taxpayer's eligibility for certain tax credits. Some credits are available only for a specific period or have deadlines for claiming the credit. It's essential for taxpayers to be aware of these timeframes to maximize their benefits. Additional restrictions may apply to specific tax credits, such as limitations on the types of expenses that qualify or caps on the maximum credit amount. Taxpayers should carefully review the rules and regulations of each credit to ensure they are eligible and aware of any limitations. To claim tax credits, taxpayers must complete the appropriate forms and provide any required documentation to support their eligibility. The forms and documentation needed will vary depending on the specific tax credit being claimed. Taxpayers should consult the IRS website or a tax services professional for guidance on the necessary forms and supporting documents. Refundable tax credits are claimed on the taxpayer's income tax return, and any excess credit over the taxpayer's tax liability will be refunded. The refundable portion of the credit is typically calculated on a separate form or schedule, which must be attached to the tax return. Non-refundable tax credits are also claimed on the taxpayer's income tax return. However, unlike refundable tax credits, non-refundable credits can only reduce the taxpayer's tax liability to zero. If the credit amount exceeds the tax owed, the excess will not be refunded to the taxpayer. Tax credits serve as valuable financial incentives provided by the government to reduce tax liability for individuals and businesses. They play a crucial role in promoting specific behaviors and supporting targeted groups, such as low-income families, students, and businesses investing in research and development. Tax credits directly reduce the amount of tax owed, offering a dollar-for-dollar reduction rather than merely lowering taxable income like tax deductions. Understanding the different types of tax credits, including non-refundable, refundable, and hybrid credits, is essential for maximizing their benefits. However, tax credits also come with limitations and restrictions, such as phase-out limits, income requirements, timing considerations, and other specific restrictions that taxpayers must be aware of. To claim tax credits, individuals must complete the appropriate forms and provide the necessary documentation, with refundable credits potentially resulting in a refund while non-refundable credits only reduce tax liability to zero. By navigating these intricacies, taxpayers can effectively leverage tax credits to minimize their tax burden and potentially receive additional financial support.Definition of Tax Credits

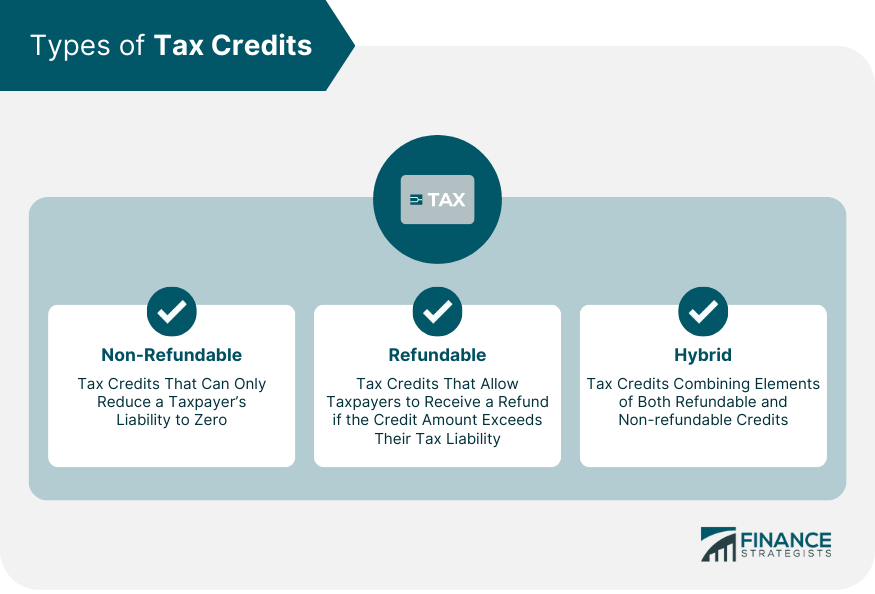

Types of Tax Credits

Non-Refundable Tax Credits

Refundable Tax Credits

Hybrid Tax Credits

Qualifying for Tax Credits

Eligibility Criteria

Income Requirements

Documentation Required

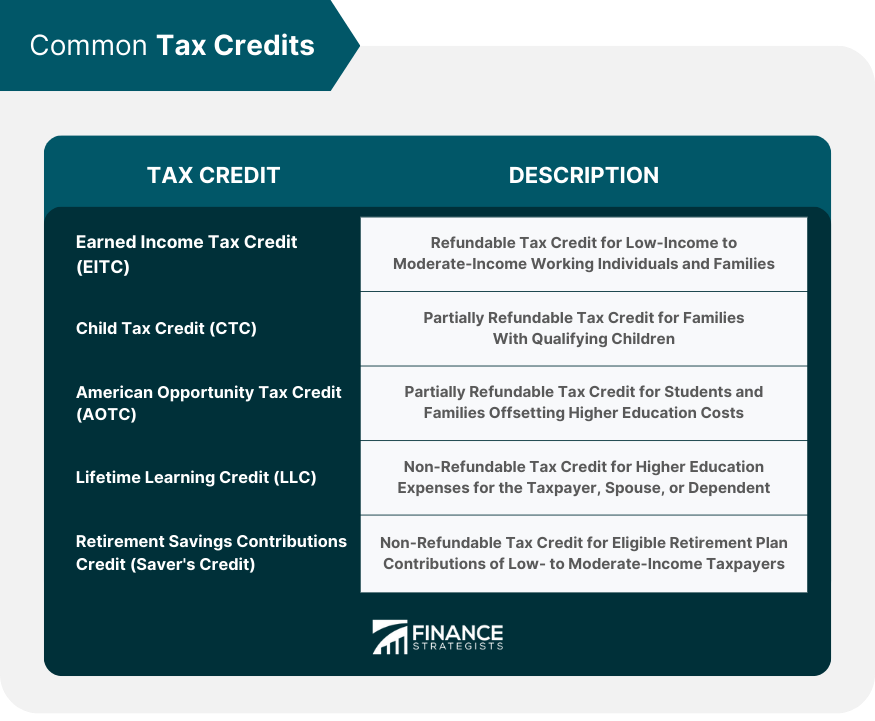

Common Tax Credits

Earned Income Tax Credit

Child Tax Credit

American Opportunity Tax Credit

Lifetime Learning Credit

Retirement Savings Contributions Credit

Limitations and Restrictions of Tax Credits

Phase-Out Limits

Income Limits

Timing of Claims

Other Restrictions

How to Claim Tax Credits

Forms and Documentation Required

Claiming Refundable Tax Credits

Claiming Non-Refundable Tax Credits

Conclusion

Tax Credits FAQs

Tax credits are reductions in tax liability offered by the government to incentivize certain behaviors or circumstances, such as buying an electric car.

Eligibility for tax credits depends on the type of credit, but typically it is based on factors such as income, family size, and expenses.

Refundable tax credits can reduce tax liability below zero, resulting in a refund. Non-refundable tax credits cannot result in a refund and only reduce tax liability.

Tax credits are typically claimed when filing your annual tax return. Forms and documentation must be submitted to prove eligibility for the credit.

Yes, there are often income limits, phase-out limits, and other restrictions on tax credits. The timing of claims may also be limited.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.