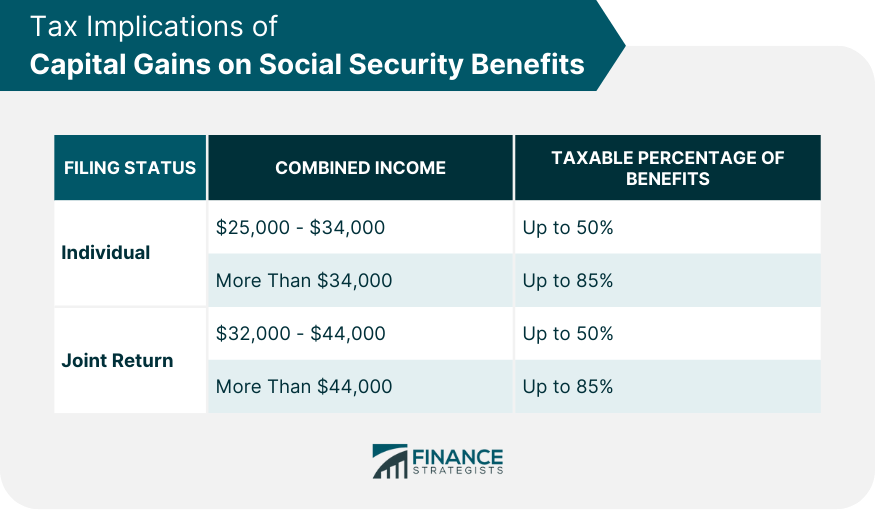

Capital gains refer to the profit made from the sale of an investment or property. They can be classified into two categories: short-term (held for one year or less) and long-term (held for more than one year). Social Security, on the other hand, is a U.S. federal program providing retirement, disability, and survivor benefits to eligible individuals. The benefits are funded by payroll taxes collected from current workers and their employers. It's important to note that while capital gains can increase one's adjusted gross income (AGI), they are not subject to Social Security taxes. However, a higher AGI from capital gains can potentially lead to a higher portion of Social Security benefits being taxable. Thus, it's essential to understand the interplay between capital gains and Social Security when planning for retirement or managing investments. Capital gains refer to the profit you make when you sell an asset, such as stocks, real estate, or other investments, for more than you paid for it. This gain, be it from a strategic investment or favorable market conditions, reflects the growth of your investment. Capital gains, however, come with tax implications that can significantly impact your overall financial portfolio. The nature of capital gains is determined by how long you've held onto the asset. Short-Term Capital Gains: Profits from assets held for a year or less. They are usually taxed at your ordinary income tax rate. Such gains can be a result of strategic short-term investments or capitalizing on market fluctuations. Long-Term Capital Gains: Profits from assets held for more than a year. They typically enjoy a lower tax rate, making them favorable for investors. Long-term investments often show commitment to a financial plan and patience in an asset's value to appreciate. The taxation rate for capital gains varies depending on several factors, primarily your income level and the duration you've held the asset. The tax system is designed to encourage long-term investments. As such, long-term capital gains can be taxed anywhere from 0% to 20%, while short-term gains are taxed at your ordinary income rate. Properly navigating these tax rates can make a substantial difference in the returns on your investments. The relationship between capital gains and social security is intricate, but crucial for retirees and those approaching retirement to understand. These connections can significantly influence your post-retirement financial health, affecting the amount of disposable income you have in your golden years. Capital gains can influence the amount of your Social Security benefits that are subject to taxation. For instance, if your combined income — which includes your adjusted gross income, non-taxable interest, and half of your Social Security benefits — exceeds a certain threshold, up to 85% of your benefits may be taxable. The inclusion of capital gains in your income can easily push you over these thresholds, leading to a higher tax on your Social Security benefits. This underlines the importance of thoughtful investment and disinvestment decisions, especially as you approach retirement. It's essential to recognize that not all Social Security benefits are taxable. For those filing as individuals: If your combined income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. This bracket is a sensitive range where slight changes in income can have amplified tax implications. If it's more than $34,000, up to 85% of your benefits may be taxable. For those who've built substantial assets and investment portfolios, understanding these numbers is pivotal. For couples filing jointly, the thresholds are between $32,000 and $44,000 for up to 50% taxation and more than $44,000 for up to 85% taxation. Navigating these thresholds as a couple requires joint financial planning and synchronized decision-making. Imagine a retiree, John, who gets $20,000 annually from Social Security. He also has $15,000 in other income and decides to sell an investment, realizing a capital gain of $10,000. This sale pushes his combined income to $35,000, making up to 85% of his Social Security benefits taxable, compared to 50% if he hadn't sold the asset. John's situation is not unique. Many retirees find themselves in similar scenarios, unaware of the ripple effect of their investment decisions. Delaying the sale of an asset can move the capital gains to a year where it might not push you into a higher taxation bracket for Social Security. If you're close to a threshold, consider if it's feasible to delay the sale. Planning sales around predictable income changes, such as a decrease in earned income during retirement, can also be advantageous. Assets in accounts like IRAs or 401(k)s grow tax-deferred. When you do decide to withdraw, it's considered regular income rather than capital gains. This can be a strategy to spread out income over several years, thus not pushing your Social Security benefits into a higher taxable bracket. By utilizing these accounts, you align your financial actions with long-term financial security. This involves selling investments that have lost value. The resulting capital losses can offset capital gains, potentially reducing the taxable amount. It's a proactive approach to managing your portfolio, ensuring that even downturns in some investments can have a silver lining for your broader financial picture. Donating appreciated assets, such as stocks, directly to charity can offer a double benefit: you avoid capital gains taxes and receive a charitable deduction. Beyond the financial benefits, this approach also allows you to make a positive impact on causes and organizations you care about. Social Security is a lifeline for many retirees. The benefits you receive are based on your 35 highest-earning years of work. However, the way these benefits are taxed can be influenced by other income, including capital gains. It's a system designed to ensure financial security in retirement, but its interaction with other income sources underscores the need for holistic financial planning. Social Security benefits are generally calculated based on the "average indexed monthly earnings." This calculation considers up to 35 years of an individual's adjusted earnings. This calculation ensures that your benefits reflect your contribution to the system throughout your working years. As mentioned, anywhere from 0% to 85% of your Social Security benefits can be taxable, based on your combined income and filing status. While it might seem daunting to understand the intricacies of this taxation, awareness can help you make informed decisions about other income sources. It's essential to strike a balance. While capital gains can provide a lucrative boost to your income, be mindful of how they can affect your Social Security benefits. By spreading out gains or strategically choosing when to Timing is crucial when it comes to claiming Social Security. Delaying the age at which you start collecting benefits can result in a significantly larger monthly payout. While the earliest you can start is age 62, waiting until your full retirement age (between 65 and 67, depending on when you were born) ensures you get 100% of your monthly benefit. Even more, for every year you delay past your full retirement age until age 70, your benefit increases. This growth can serve as a buffer against potential tax hits from capital gains in the future. Apart from retirement accounts, consider other tax-efficient investment options like Roth IRAs, which allow qualified withdrawals to be tax-free. This means that when you do decide to draw from these accounts, it won't count towards the income determining the taxation of your Social Security benefits. Roth conversions, where you convert traditional IRA money to a Roth IRA, can also be a strategic move, especially in years where you anticipate lower income. It's not just about which assets you own, but also where you place them. For instance, investments that generate regular taxable income, like bonds, might be better suited in tax-deferred accounts, while stocks, which have the potential for long-term capital gains, could be placed in taxable accounts. This strategy can ensure you have a mix of both regular and capital gain income, which you can strategically manage based on your Social Security income thresholds. If you're drawing from multiple income sources during retirement, adjust your withdrawal strategies annually. For instance, in a year where you realize more capital gains than anticipated, you might want to minimize withdrawals from retirement accounts. Conversely, in a year with minimal capital gains, it might be advantageous to draw more from retirement accounts and let your other investments grow. While understanding the basics is essential, the intricate dance between capital gains and Social Security can benefit from expert advice. Financial advisors or tax professionals can offer tailored strategies that factor in your unique financial situation, helping you maximize benefits while minimizing tax obligations. The intricate relationship between capital gains and Social Security taxation underscores the necessity for meticulous financial planning, especially for retirees or those nearing retirement. While capital gains can be a significant source of income, especially when assets appreciate, they can inadvertently affect the taxable amount of Social Security benefits. Distinct thresholds dictate the percentage of Social Security benefits that become taxable, and capital gains can easily tip a retiree's combined income over these thresholds. Strategic maneuvers, such as timing asset sales, using tax-advantaged retirement accounts, capital loss harvesting, and charitable giving, can help mitigate adverse tax implications. Moreover, understanding the Social Security system and seeking expert advice can ensure individuals reap the maximum benefits of their investments while ensuring their Social Security remains as tax-efficient as possible. If you're keen on maximizing your financial potential while minimizing tax liabilities, consider seeking expert tax planning services today.Overview of Capital Gains and Social Security

Understanding Capital Gains

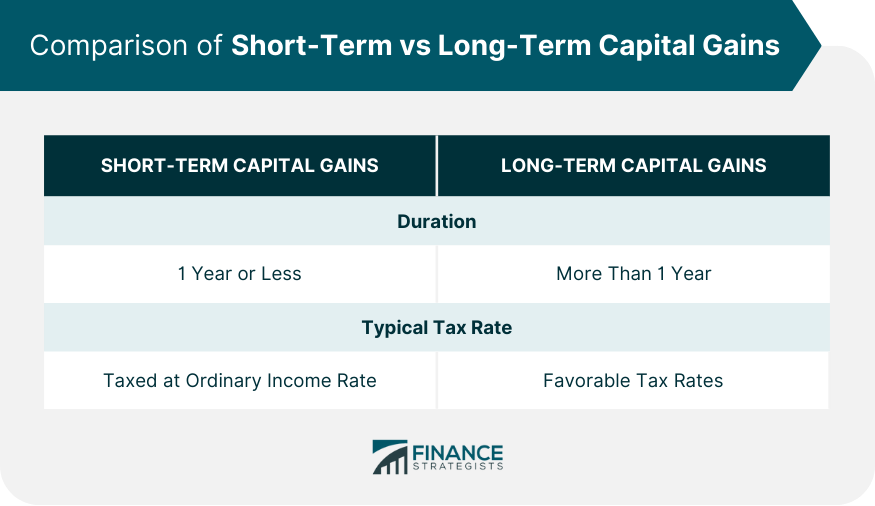

Types of Capital Gains: Short-Term vs Long-Term

How Capital Gains Are Taxed

Interplay of Capital Gains and Social Security Benefits

Direct Impact of Capital Gains on Social Security Benefits

Tax Implications of Capital Gains on Social Security Benefits

Examples Illustrating the Impact of Capital Gains on Social Security

Strategies to Minimize the Impact of Capital Gains on Social Security

Timing of Selling Assets

Using Tax-Advantaged Retirement Accounts

Capital Loss Harvesting

Utilizing Charitable Giving Strategies

Understanding Social Security

How Social Security Benefits Are Calculated

How Social Security Benefits Are Taxed

Strategic Planning for Capital Gains and Social Security

Balance Capital Gains and Social Security Income

Maximize Social Security Benefits

Use Tax-Efficient Investment Vehicles

Apply Asset Location Strategy

Adjust Withdrawal Strategies

Seek Professional Guidance

Bottom Line

Impact of Capital Gains and Social Security FAQs

Capital gains can influence the taxable amount of your Social Security benefits, with up to 85% potentially being taxable based on combined income.

Short-term capital gains arise from assets held for a year or less and are taxed at your ordinary income rate. Long-term gains come from assets held longer and usually have favorable tax rates.

Not necessarily. Depending on combined income, including capital gains, anywhere from 0% to 85% of your Social Security benefits can be taxable.

Strategies include timing of selling assets, using tax-advantaged retirement accounts, capital loss harvesting, and charitable giving.

While one can start at age 62, waiting until the full retirement age (between 65 and 67) ensures 100% benefits. Delaying even further up to age 70 can increase benefits by about 8% annually.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.