The 529 plans are state-sponsored, tax-advantaged savings plans for future education costs, comprising prepaid tuition and education savings plans. Prepaid tuition plans let you buy future tuition credits at current rates, while education savings plans are investment accounts with tax-free growth for educational expenses. These plans offer tax-free growth and withdrawals for qualified expenses, with many states providing additional tax benefits. Individual Retirement Accounts (IRAs), essential for retirement planning, offer tax advantages for long-term savings. Traditional IRAs provide tax-deferred growth and possible tax-deductible contributions, taxed upon retirement withdrawal. Roth IRAs allow tax-free growth and withdrawals with after-tax contributions. The choice between these depends on individual tax rates, retirement age, and income needs, governed by specific IRS rules. The 529 plans are ideal for funding education with flexible beneficiary changes and high contribution limits, while IRAs, crucial for retirement savings, offer different tax benefits based on the account type, aiding in financial security planning. Yes, you can roll over unused funds from a 529 plan into a Roth IRA. This provision was enacted as part of the SECURE 2.0 Act, which was signed into law in December 2022. The rollover is limited to a lifetime maximum of $35,000 for each 529 account beneficiary. To be eligible for the rollover, the 529 account must have been open for at least 15 years, and the funds must have been in the account for at least five years. For 2026, the rollover amount cannot exceed the annual Roth IRA contribution limit, which is $7,500 for individuals under age 50 and $8,100 for individuals age 50 and older. The rollover must be made directly from the 529 plan to the Roth IRA. The beneficiary of the 529 plan must also be the owner of the Roth IRA. The rollover is tax-free and penalty-free. Here are some of the benefits of rolling over unused 529 funds into a Roth IRA: Tax-Free Growth and Withdrawals: Your Roth IRA will grow tax-free, and you will be able to withdraw your contributions and earnings tax-free in retirement. More Flexibility: You can use your Roth IRA for a wider range of expenses than you can use your 529 plan. For example, you can use your Roth IRA to purchase a first home or pay for medical expenses. No Age Restrictions: You can withdraw money from your Roth IRA at any age without penalty. The 529 plans generally do not have annual contribution limits but do have lifetime contribution limits that vary by state, often reaching several hundred thousand dollars. This allows for significant flexibility in how much can be saved over time. In contrast, IRAs have annual contribution limits set by the IRS, which are typically much lower. For instance, as of 2026, the limit is $7,500 per year or $8,100 for those aged 50 and older. Understanding these limits is vital for effective financial planning. While 529 plans allow for large, lump-sum contributions, making them ideal for grandparents or relatives who wish to contribute to a child's education, IRAs require a more consistent, annual contribution approach, making them suitable for gradual retirement savings. The tax treatment of 529 plans and IRAs is a key difference between the two. Contributions to 529 plans are not federally tax-deductible, though many states offer tax deductions or credits. The primary tax benefit of a 529 plan lies in the tax-free growth and tax-free withdrawals for qualified education expenses. In contrast, IRAs offer different tax benefits based on the type of account. Traditional IRAs may provide immediate tax benefits in the form of tax-deductible contributions, while Roth IRAs offer tax-free withdrawals in retirement. This difference in tax treatment means that individuals must consider their current and future tax situations when choosing between these accounts. For instance, a Roth IRA might be more beneficial for someone who expects to be in a higher tax bracket in retirement, while a 529 plan is ideal for those prioritizing education savings with tax-free growth. The 529 plans are specifically designed for education-related expenses, including tuition, fees, room and board, books, and supplies at eligible institutions. This includes both post-secondary education and, up to a certain amount, K-12 tuition. The focus on education makes these plans highly suitable for families looking to save for a child’s educational future. IRAs, being retirement savings vehicles, do not typically include education expenses as qualified distributions, except under certain circumstances like the first-time home purchase or specific education expenses. Early withdrawals from IRAs for non-qualified expenses can result in penalties and taxes, emphasizing the need to use these accounts primarily for retirement purposes. Withdrawal rules for 529 plans are relatively straightforward: withdrawals are tax-free as long as they are used for qualified education expenses. Non-qualified withdrawals, however, are subject to income tax and a 10% penalty on the earnings. In contrast, IRAs have different rules based on the type of account. Traditional IRAs impose taxes and penalties on early withdrawals before age 59 ½, while Roth IRAs allow contributions to be withdrawn tax- and penalty-free, but earnings are subject to taxes and penalties if withdrawn early. Understanding these withdrawal rules is critical, especially when considering the timing and purpose of withdrawals. For 529 plans, aligning withdrawals with educational expenses is key, while for IRAs, planning for retirement age and the tax implications of withdrawals is essential. One viable alternative to a direct rollover is changing the beneficiary of the 529 plan. This option is particularly useful if the original beneficiary does not need all the funds for their education. The plan allows for the beneficiary to be changed to another family member, including siblings, cousins, or even the account holder themselves, without incurring any tax penalty as long as the new beneficiary uses the funds for qualified educational expenses. This flexibility makes 529 plans uniquely adaptable to changing family circumstances or educational needs. It allows families to continue to benefit from the plan’s tax advantages and ensures that the funds are used for their intended educational purpose, even if the original beneficiary's situation changes. Withdrawing funds from a 529 plan for non-qualified expenses is another option, albeit with tax implications. While such withdrawals are subject to income tax and a 10% penalty on the earnings portion, they provide a way to access funds if the beneficiary does not need them for education. This can be a practical choice in situations where the funds are needed for other important family expenses or financial needs. However, this approach should be used cautiously due to the tax and penalty implications. It is often recommended to explore all other options and use this as a last resort, ensuring that the decision aligns with the overall financial plan and long-term goals of the family. For unused 529 plan funds, considering other investment options is a prudent strategy. Transferring these funds to a taxable investment account is one possibility. This approach allows for continued investment growth, although without the tax-free benefit for educational expenses. Such accounts offer greater flexibility in terms of investment choices and the use of the funds, making them suitable for long-term financial goals beyond education. Another option is to simply hold the funds in the 529 plan for future educational needs, such as graduate studies or the education of a future family member. This approach maintains the tax advantages and can be part of a longer-term educational savings strategy. The key is to align the decision with the overall financial objectives, considering factors like investment horizon, risk tolerance, and potential future educational needs within the family. When balancing a 529 plan and an IRA, it's crucial to assess your financial goals with a focus on the long-term perspective. For families with young children, prioritizing education savings might be more pressing, while for those nearing retirement, maximizing IRA contributions could be paramount. This assessment should take into account the time horizon for each goal, the projected costs of education, and the estimated needs for retirement. It's also essential to consider the flexibility of each account type. While 529 plans are specifically for education expenses, IRAs offer broader options for retirement savings. Understanding these nuances can help in making informed decisions that align with both immediate and future financial needs. Diversifying contributions between a 529 plan and an IRA can be an effective strategy for addressing both education and retirement goals. This approach allows you to take advantage of the distinct tax benefits of each account type while working towards multiple financial objectives. It's important to regularly review and adjust these contributions based on changes in income, family circumstances, and financial goals. Another strategy is to take a phased approach, prioritizing one type of account during certain life stages and then shifting focus as circumstances change. For example, you might focus on 529 contributions when children are young and shift to higher IRA contributions as they grow older and closer to college age. Timing contributions and withdrawals from both 529 plans and IRAs is essential for tax efficiency. For 529 plans, consider state tax benefits and the timing of educational expenses to maximize tax advantages. For IRAs, factor in tax deductions, tax brackets, and potential tax implications of retirement withdrawals. Timing contributions to align with high-income years can maximize tax benefits for Traditional IRAs while contributing to a Roth IRA in lower-income years can optimize tax-free growth. Additionally, consider the impact of required minimum distributions (RMDs) from Traditional IRAs and the tax-free nature of Roth IRA withdrawals in retirement planning. Balancing contributions between Traditional and Roth IRAs can provide tax diversification and flexibility in managing taxable income in retirement. Long-term tax planning is essential when considering any rollover decisions between a 529 plan and an IRA. While direct rollovers are not permitted, the decision to reallocate funds from one type of account to another should be made with an understanding of future tax implications. This includes considering the tax treatment of withdrawals and the impact on overall tax liability. For instance, if funds are withdrawn from a 529 plan for non-qualified expenses and then contributed to an IRA, the tax implications of this action must be carefully evaluated. It's important to consult with a tax advisor to understand the nuances of such decisions and how they align with your overall tax strategy. Any decision involving the movement of funds from a 529 plan could potentially impact your retirement savings goals. It's essential to consider how reallocating these funds may affect your ability to meet your retirement objectives. If funds initially earmarked for education are redirected, it may necessitate adjustments to retirement savings strategies or contribution levels. In this context, it's important to consider the long-term growth potential of both types of accounts and how they contribute to overall financial security. Balancing the immediate need for education funding with the long-term goal of retirement savings is a key aspect of comprehensive financial planning. Financial planning must be adaptable to unexpected changes in circumstances. This includes being prepared for changes in educational needs, retirement goals, or overall financial situations. When dealing with 529 plans and IRAs, having a flexible strategy that can accommodate such changes is crucial. For example, if a child decides not to pursue higher education, understanding the options for the 529 plan funds becomes important. Similarly, changes in retirement plans or financial needs might necessitate a reassessment of IRA contributions and investment strategies. Planning for these eventualities and understanding the options available can help ensure that financial goals remain achievable even as circumstances evolve. Navigating 529 plans and Individual Retirement Accounts (IRAs) is key to effective financial planning. The SECURE 2.0 Act allows for limited rollovers from 529 plans to Roth IRAs, providing tax-free growth and diversified expense options. It's crucial to understand their differences in contribution limits, tax treatments, and qualified expenses. The 529 plans are ideal for education savings with higher contribution limits, while IRAs offer retirement-focused tax benefits with annual contribution limits. Strategic planning should balance these accounts, focusing on long-term goals and tax-efficient timing of contributions and withdrawals. Alternatives like beneficiary changes in 529 plans or other investment routes accommodate evolving educational and financial needs. Careful consideration of long-term tax implications, retirement goals, and adaptability to changing circumstances is essential in maximizing these financial tools.Overview of 529 Plans and Individual Retirement Accounts (IRAs)

Can You Rollover a 529 Plan Into an IRA?

Understanding the Differences Between 529 Plans and IRAs

Contribution Limits

Tax Treatment and Benefits

Qualified Expenses

Withdrawal Rules

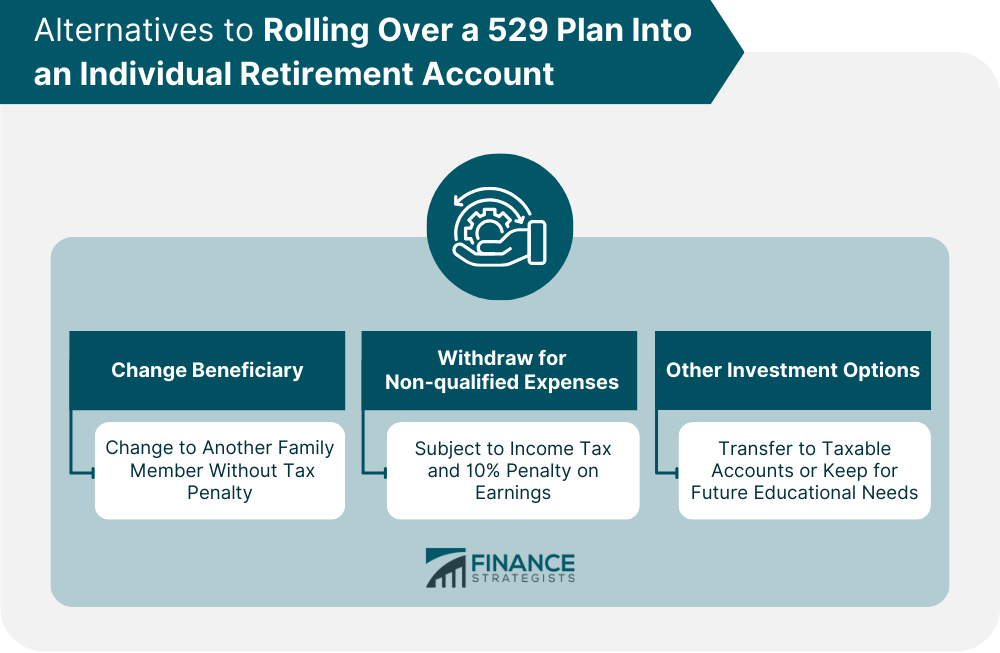

Alternatives to Rolling Over a 529 Plan Into an IRA

Change the Beneficiary of a 529 Plan

Withdraw Funds for Non-qualified Expenses

Other Investment Options for Unused 529 Funds

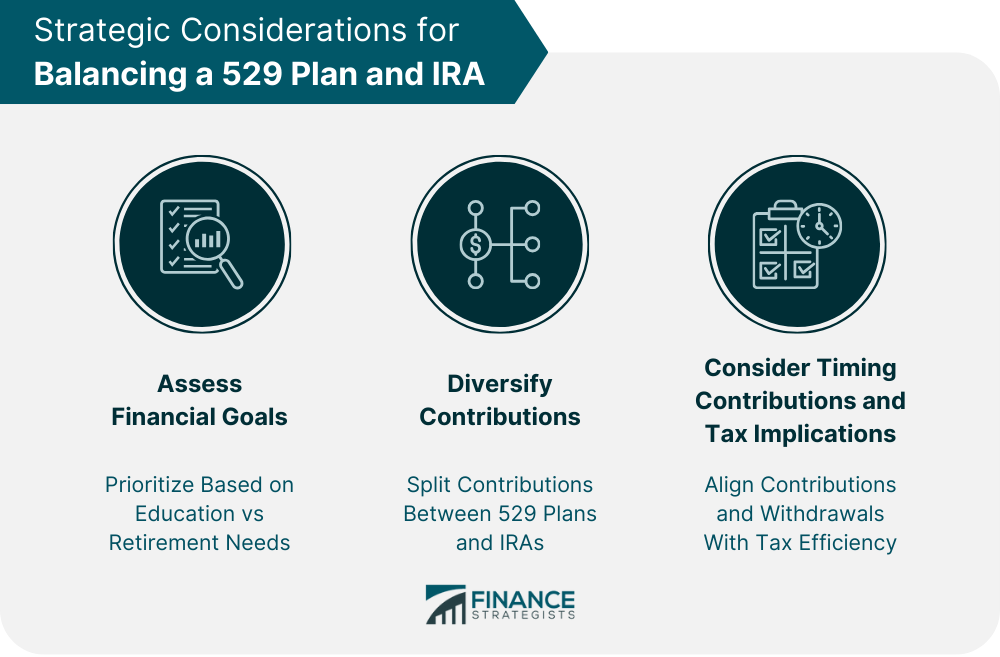

Strategic Considerations for Balancing a 529 Plan and IRA

Assess Financial Goals

Diversify Contributions

Consider Timing Contributions and Tax Implications

Long-Term Implications of Rollover Decisions

Future Tax Considerations

Impact on Retirement Savings Goals

Planning for Unexpected Changes in Circumstances

Final Thoughts

Rollover 529 to IRA FAQs

Yes, you can rollover unused funds from a 529 plan to a Roth IRA under the SECURE 2.0 Act, with a lifetime limit of $35,000 per beneficiary and certain conditions like a 15-year account opening requirement.

For a rollover from 529 to IRA, the 529 account must be at least 15 years old, the funds should have been in the account for a minimum of 5 years, and the rollover amount cannot exceed the annual Roth IRA contribution limits.

The rollover from 529 to IRA is tax-free and penalty-free, provided it meets the requirements of the SECURE 2.0 Act, such as the 529 plan being 15 years old and adhering to the Roth IRA contribution limits.

You can rollover up to a lifetime maximum of $35,000 per 529 account beneficiary to an IRA, but the annual contribution must not exceed the Roth IRA limits (In 2026, it is $7,500 for individuals under 50 and $8,100 for those 50 and older).

Beneficiaries of a 529 plan who no longer need the funds for educational purposes can benefit from a rollover to an IRA, allowing them to repurpose these funds for retirement savings while enjoying tax-free growth.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.