Planning for retirement is essential, but life's unexpected circumstances may lead some individuals to consider early withdrawal from their 401(k) accounts. While tapping into retirement savings before reaching retirement age is generally discouraged due to potential tax penalties and long-term financial implications, there are certain situations where it might be necessary. Understanding the rules and options for early withdrawal from a 401(k) can help individuals make informed decisions about their financial future. There are various scenarios and strategies for early 401(k) withdrawals, and potential risks and benefits associated with accessing retirement funds ahead of schedule. Your first step should be to get in touch with your 401(k) plan administrator. They can provide you with information specific to your plan, including the process for early withdrawal and any potential penalties. Once you've reached out to your plan administrator, you need to verify if you are eligible for an early withdrawal. Factors that can affect your eligibility include your age, the reason for the withdrawal, and the terms of your specific 401(k) plan. Withdrawing from your 401(k) early could have significant tax implications. You must understand these before making a withdrawal. The money you withdraw will be considered income for tax purposes, and you could face additional penalties if you do not meet the eligibility criteria for an exception. After considering the criteria and potential consequences, weigh the pros and cons. Understand the immediate relief you may gain from the funds versus the long-term impact on your retirement savings and potential penalties and taxes. Financial Hardship: Financial hardship is one of the main reasons people consider early withdrawal. This can include situations such as sudden job loss, medical emergencies, or significant unforeseen expenses. Disability or Illness: If you become seriously ill or disabled and can no longer work, you might need to tap into your 401(k) early to cover your living expenses. First-Time Home Purchase: Some plans allow for an early withdrawal penalty-free for a first-time home purchase. However, the withdrawal is still subject to income taxes. Higher Education Expenses: You might also consider withdrawing from your 401(k) early to cover higher education expenses for you or your dependents. Rule 72(t), dictated by the Internal Revenue Service (IRS), permits you to make early withdrawals from your 401(k) without penalty, provided they're part of a series of substantially equal payments spread over your life expectancy. This strategy requires careful planning to ensure the payments are properly calculated and distributed. The Rule of 55 provides another exception to the early withdrawal penalty. If you resign from your job during or after the year you reach age 55 or 50, some public safety workers, you're permitted to make withdrawals from your 401(k) free from the usual 10% penalty. Disability is another circumstance that may necessitate early withdrawal from your 401(k). In the event you become permanently and completely disabled, you're eligible to access your funds without the imposition of the 10% early withdrawal penalty. In the instance of inheriting a 401(k), you are allowed to make withdrawals without being subject to the standard early withdrawal penalty. However, it's important to note that these withdrawals remain subject to regular income tax. Overview of Tax Penalties: Typically, when you withdraw from your 401(k) early, you are subject to a 10% early withdrawal penalty in addition to regular income taxes. How to Calculate Potential Tax Penalties: To calculate potential tax penalties, add your withdrawal amount to your taxable income for the year, apply your marginal tax rate, and add 10% for the early withdrawal penalty. Tips to Minimize Tax Penalties: To minimize tax penalties, consider whether you qualify for any of the penalty exceptions, look at other sources of income or loans first, or consider if a 401(k) loan might be a better option for you. A potential alternative to making an early withdrawal could be taking a loan from your 401(k), if your plan permits it. This alternative can be financially advantageous as the interest you pay is effectively paid back to your own account, thus retaining some value within your retirement fund. Rolling over your 401(k) into an Individual Retirement Account (IRA) might be a viable strategy. This option often offers more flexibility in withdrawal scenarios and could provide tax efficiencies that your current 401(k) plan does not. Before resorting to early withdrawal, you should thoroughly explore other financial aid and loan opportunities. These might include personal loans, home equity loans, or student financial aid, which may present fewer long-term disadvantages. After an early withdrawal, it's crucial to strategize about rebuilding your retirement savings. Options include increasing future 401(k) contributions, using catch-up contributions if you're over 50, and considering additional vehicles like an IRA or taxable investment account. The process of recovery should also involve setting clear financial goals and planning to achieve them. Budgeting, reducing unnecessary expenses, and potentially seeking financial advice could play significant roles in this process. The experience of an early withdrawal could be a valuable lesson for future financial planning. Consider establishing an emergency fund to avoid similar situations, be cautious about future withdrawals, and consider seeking financial advice to help you navigate future financial challenges. While early withdrawal from a 401(k) can provide immediate financial relief, it's crucial to consider the long-term implications. Not only could the funds withdrawn be subject to regular income taxes, but you may also face a 10% early withdrawal penalty unless you qualify for exceptions such as the IRS Rule 72(t) or Rule 55. Alternatives like borrowing from your 401(k) or an IRA rollover should be explored before deciding on early withdrawal. If you've already withdrawn funds, strategies to rebuild your retirement savings are essential. Increasing future contributions, setting clear financial goals, and learning from past decisions are key components of recovery. In all financial matters, especially those involving retirement savings, it's advised to seek professional financial advice to ensure you are making the most informed decisions.Early Withdrawal From 401(k) Overview

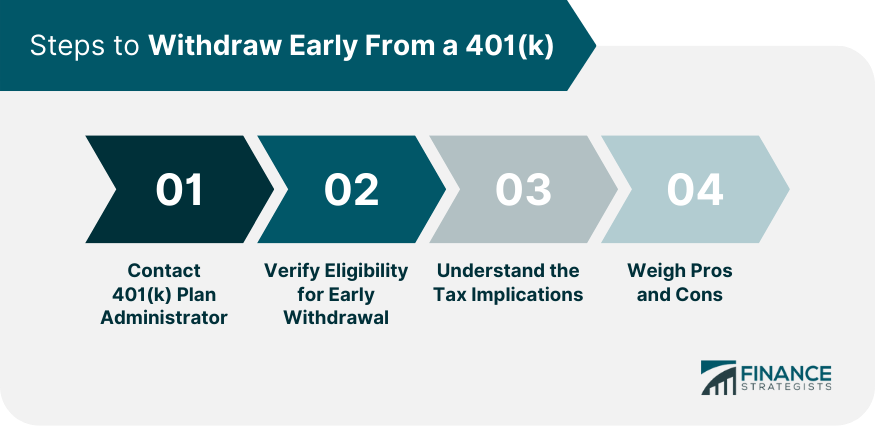

Steps to Withdraw Early From 401(k)

Contact 401(k) Plan Administrator

Verify Eligibility for Early Withdrawal

Understand the Tax Implications

Weigh Pros and Cons

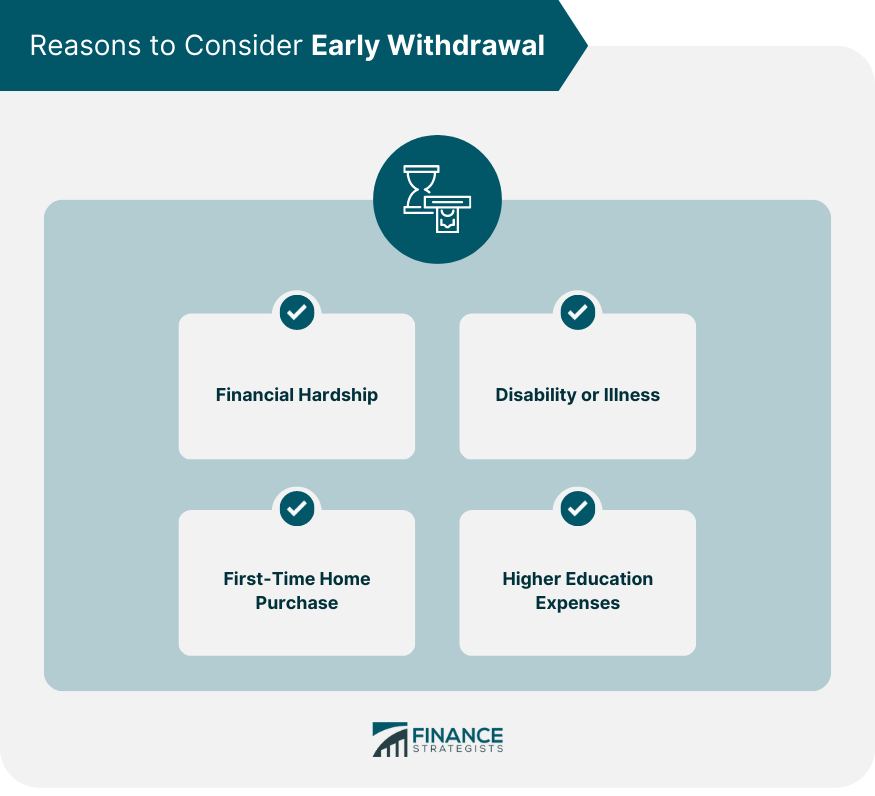

Reasons to Consider Early 401(k) Withdrawal

However, it's important to note that other financing options could be less detrimental to your long-term financial stability.

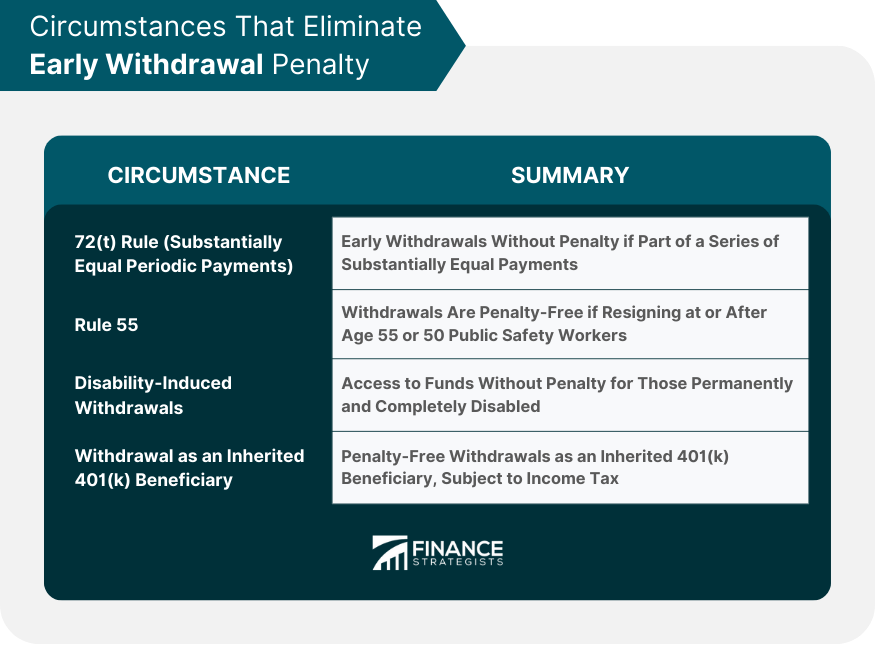

Circumstances That Eliminate Early 401(k) Withdrawal Penalty

72(t) Rule (Substantially Equal Periodic Payments)

Implement the Rule 55

Disability-Induced Withdrawals

Withdrawal as an Inherited 401(k) Beneficiary

Tax Implications of Early 401(k) Withdrawal

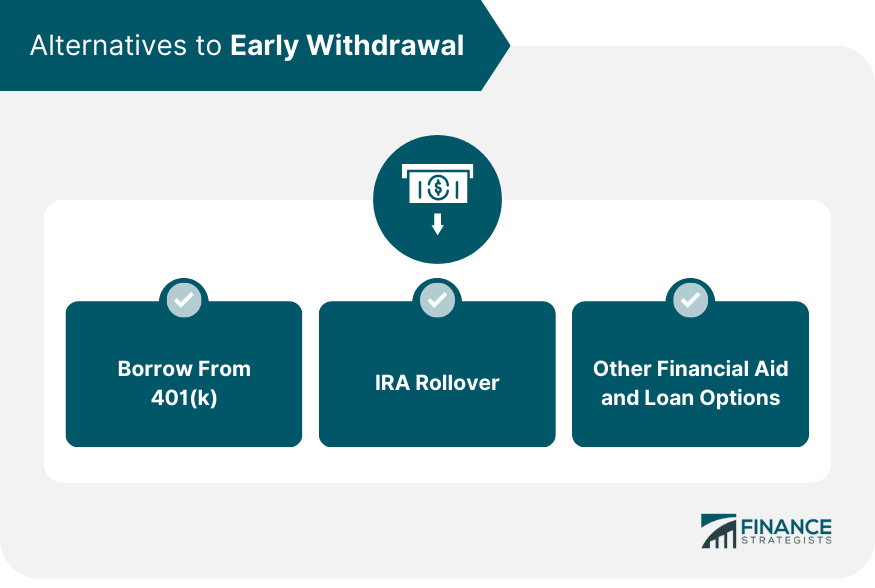

Alternatives to Early 401(k) Withdrawal

Borrow From 401(k)

IRA Rollover

Other Financial Aid and Loan Options

Recovery Strategies After Early 401(k) Withdrawal

Rebuild Retirement Savings

Set Clear Financial Goals

Learn From Past Financial Decisions

Conclusion

How to Withdraw Early From Your 401(k) FAQs

An early withdrawal from a 401(k) refers to taking out funds from your 401(k) retirement plan before reaching the age of 59 ½. This is generally discouraged due to the significant tax penalties and long-term effects on your retirement savings.

Yes, there are several exceptions to the 10% penalty for early 401(k) withdrawals, including the IRS Rule 72(t), which allows for a series of substantially equal periodic payments, the Rule of 55 for those leaving their job at 55 or older, permanent disability, and being a beneficiary on an inherited 401(k).

Yes, some 401(k) plans allow for loans, which could be a better financial decision than an early withdrawal. In this scenario, you pay the interest back to your own account. However, there are risks, including the full balance becoming due if you lose your job.

To calculate potential tax penalties, you would add the amount you plan to withdraw to your taxable income for the year. Then, you would apply your marginal tax rate to this total and add a 10% penalty for the early withdrawal.

Strategies to recover from an early 401(k) withdrawal include increasing your future 401(k) contributions, utilizing catch-up contributions if you're over age 50, contributing to an IRA, or using a taxable investment account. Establishing financial goals and creating a plan to reach them is also essential in the recovery process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.