The rule of 55 is a tax strategy that enables you to start withdrawing money from your retirement savings account without incurring the 10% tax penalty after attaining age 55. The funds withdrawn can be used for any purpose and are not limited to retirement-related expenses. This means you can use these distributions to fund your early retirement lifestyle. The rule of 55 specifically applies to 401(k) and 403(b) retirement plans. They are both tax-advantaged, employer-sponsored retirement plans, which means you can have one or the other as part of your benefits package at most full-time jobs. A 403(b) and 401(k) differ primarily in the sort of employer who offers them. Private, for-profit businesses provide 401(k) programs. On the other hand, tax-exempt organizations and nonprofits provide 403(b) plans. The rule of 55 does not apply to individual retirement accounts (IRAs). Originally, 401(k) and 403(b) imposed penalties on early distributions. If you take a payout from your 401(k) or 403(b) while you are under 59 1/2, you will be subject to a 10% early withdrawal penalty. However, a 20% income tax withholding rate would still apply to any distribution. After filing your yearly tax return, you will receive a refund if it turns out that 20% is more than you owe based on your total taxable income. The IRS regulation rule of 55 allows employees who are 55 or older to pull out funds from their 403(b) or 401(k) plan without penalty if two conditions are met. For instance, if an employee decides to quit his job shortly after his 55th birthday, he can withdraw funds from his 401(k) or 403(b) without incurring the 10% early withdrawal sanction. You cannot receive Social Security payments if you retire early. As a result, taking early withdrawals from retirement savings to meet your needs makes sense. Using the rule of 55 tax strategy will help you save on penalties that would have been incurred if you withdrew the money before 59 1/2. Below are the steps you can take to use the rule of 55 to help fund your early retirement. Verify with the retirement plan provider if the company policy allows the rule of 55. Upon confirmation, employees should leave their job the year they turn 55 or later, so they can take advantage of this regulation. Withdrawals can only be taken from the current 401(k) or 403(b) account and not from a previous employer’s plan. When planning to retire early, employees should transfer their retirement money from previous employment and other retirement accounts into their present 401(k) or 403(b). Employees are not required to retire earlier than usual if they withdraw at age 55. Suppose they decide to return to part-time or even full-time employment. In that case, they can still withdraw from their 401(k) without incurring a penalty, considering that they come from the same account. The rule of 55 is an excellent strategy for those who wish to retire early. It allows for access to retirement funds without incurring a 10% penalty. You can lower or eliminate the required minimum distributions (RMDs) you would be obligated to take at age 72. However, consider the potential tax repercussions before making decisions of this nature. This rule can also be helpful for individuals who lost their jobs and need to use the money to pay for their daily expenses. There are various scenarios when it would make sense, but consider that pulling out money from retirement accounts decreases its potential benefit for compounding returns. The following are some alternatives to the rule of 55 withdrawals: The SEPP plan lets an employee withdraw a fixed sum from his retirement account every year without being subject to the 10% early withdrawal penalty. The payments are based on the employee's life expectancy and can be taken for up to five years. A 401(k) loan can help avoid the 10% withdrawal penalty. It is possible to borrow up to $50,000 or 50% of the account's value, whichever is less. The interest paid on these loans is deposited back into the 401(k) account. The IRS also waives the 10% penalty in cases of severe financial need. The hardship must be due to the employee's immediate and heavy financial need. These may include, among others, medical expenses, the cost of purchasing a primary residence, and educational fees. The IRS offers exceptions to the 10% tax on early distributions. The most common exemption is applied for death or those with a total and permanent disability. In some cases, qualified higher education expenses are exempt from the early distribution tax and payments for health insurance premiums during unemployment. 401(k) includes automatic enrollment, corrective distributions, and payments made according to a Qualified Domestic Relations Order (QDRO). For 403(b), in-plan Roth rollovers or eligible distributions paid to another retirement plan or IRA within 60 days are also exempted. The rule of 55 is an IRS regulation that permits workers aged 55 or older to withdraw funds from their 401(k) and 403(b) retirement plans without incurring the 10% withdrawal penalty. Withdrawals are made in the year of the employee's 55th birthday and after leaving their employer. Workers can only withdraw from their current employer's plan. The rule of 55 is an excellent strategy for those who wish to retire early but pulling out money decreases the potential benefit for compounding returns. It is important to consult with a retirement professional before using the rule to determine the possible consequences of such actions.What Is the Rule of 55?

How the Rule of 55 Works

How to Fund an Early Retirement Using the Rule of 55

Leave Your Job the Year You Turn 55 or Later

Withdraw Funds Only From Your Current 401(k) or 403(b) Account

Retire Early or Change Jobs

When to Use the Rule of 55

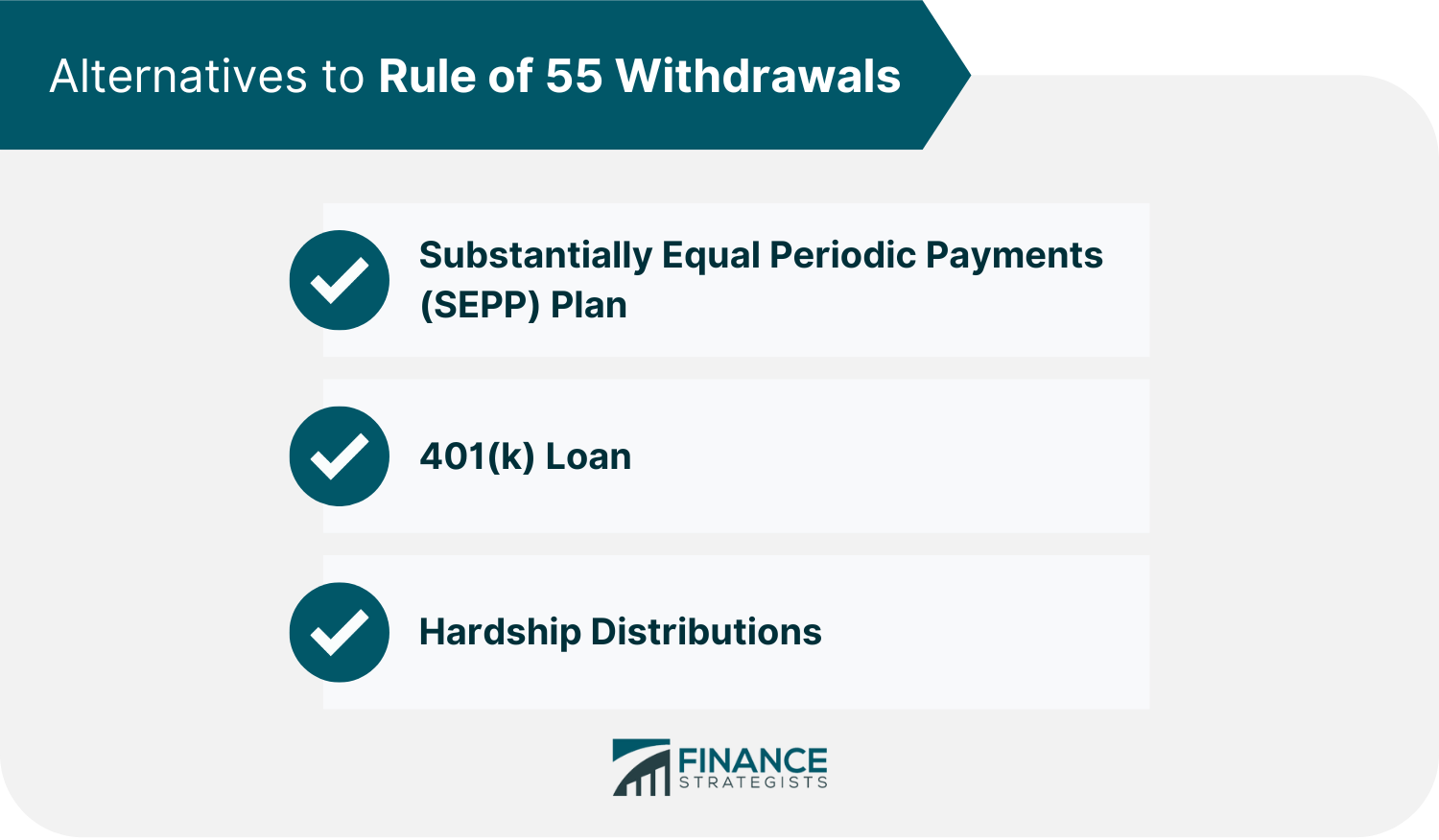

Alternatives to Rule of 55 Withdrawals

Substantially Equal Periodic Payments (SEPP) Plan

401(k) Loan

Hardship Distributions

Other Exceptions to the 10% Tax on Early Withdrawals

The Bottom Line

Rule of 55 FAQs

The rule of 55 is a special provision that allows employees who leave their job at age 55 or older to access their 401(k) and 403(b) account without incurring the 10% early withdrawal penalty.

No. The rule of 55 only waives the 10% early withdrawal penalty. Taxes will still be due on the distributions. Regardless of the rule of 55, employees are still responsible for the income tax. With a standard 401(k), they must pay taxes on any amount they withdraw.

You are not compelled to retire earlier than usual if you take early withdrawals at age 55. If you decide to return to part-time or even full-time employment, you can continue to withdraw from your 401(k) without incurring a penalty.

To qualify for the rule of 55, you must leave your job on or after the date you turn 55. If you retire before turning 55, you will not be eligible for the rule of 55 and will be subject to the 10% early withdrawal penalty if you take money from 401(k) or 403(b) accounts.

You can use the rule of 55 after you turn 55. Circumstantial events that may lead you to use this rule include leaving your job, retiring, or getting laid off.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.