Fannie Mae, formally known as the Federal National Mortgage Association, was born out of the New Deal in 1938. Its purpose was to revive the housing market during the Great Depression by buying long-term mortgages from banks, thereby encouraging further lending. The goal was to make home ownership accessible to the middle-class. Fannie Mae became a private entity in 1968 but continues to aim at enhancing homeownership accessibility for low to moderate-income Americans under a congressional charter. In the mortgage industry, Fannie Mae is instrumental. It ensures lenders have adequate funds for home loans by buying mortgages, converting them into mortgage-backed securities, and selling these to investors. Fannie Mae's endorsement gives lenders the confidence to offer more home loans. Moreover, it sets guidelines for the mortgages it will acquire, including loan limits, down payment requirements, and eligible properties. These rules significantly influence the mortgage industry and home buyers' opportunities. Appraisals are vital in the mortgage lending process because they provide an objective estimate of a property's value. The appraisal helps ensure that the amount of money requested by a borrower is appropriate, given the property's condition and market value. It also protects Fannie Mae (and, by extension, taxpayers), from undue risk, ensuring the loan is adequately collateralized. Fannie Mae sets specific appraisal requirements to regulate the process, making sure it's accurate, reliable, and conducted by qualified professionals. Compliance with these guidelines is necessary for a mortgage to be eligible for purchase by Fannie Mae. Fannie Mae's appraisal guidelines cover multiple areas, including the qualifications of the appraiser, the contents of the appraisal report, and the minimum standards the property must meet. Furthermore, they outline the methods that appraisers should use to determine the property's market value. Moreover, there are specific requirements concerning the age of an appraisal, appraisal updates, and the forms used for documenting these processes. All of these collectively ensure the appraisal provides a thorough, accurate, and current assessment of the property's value. Fannie Mae's appraisal guidelines lay out the Minimum Property Standards (MPS) that properties must meet. These standards ensure that the homes financed by Fannie Mae mortgages are safe, sound, and structurally secure. The property should be free from hazards that could affect the occupants' health or safety or jeopardize the structure's soundness and security. MPS cover a wide range of factors, including utilities, structural condition, mechanical systems, and site hazards. The appraiser's job is to assess these factors and determine if the property meets Fannie Mae's standards. Fannie Mae requires appraisers to complete specific forms when conducting an appraisal. The Uniform Residential Appraisal Report (URAR), also known as Form 1004, is the most commonly used. This form asks the appraiser to describe the property's physical characteristics, assess its condition, and compare it with similar properties that have recently sold in the area. There are other forms for different types of properties and appraisal situations. For instance, there's a specific form for condominium units and another for multi-family homes. Selecting and correctly filling out the right form is a crucial part of the appraisal process. Market value, as defined by Fannie Mae, is the most probable price a property should bring in a competitive and open market. The appraiser's task is to estimate this value by examining the property's characteristics, recent comparable sales, and current market conditions. The appraiser is expected to use one or more of the standard appraisal methods: the sales comparison approach, the cost approach, and the income approach. The selected method or methods depend on the property type and the local market. The appraisal should include an analysis of the site on which the property is located. The appraiser must examine the size, shape, and topography of the site, as well as its utilities, street improvements, and compatibility with the neighborhood's character. In addition, the appraiser must assess any adverse site conditions or external factors that could impact the property's value. These might include issues like noise, odor, traffic, or other nuisances. A crucial part of the appraisal process involves analyzing the property's neighborhood. The appraiser must examine current market conditions, property values, sales activity, and any positive or negative factors influencing the neighborhood's desirability. The property itself is analyzed in detail. This analysis includes its current use, zoning, improvements, structural integrity, condition, and any needed repairs. The property's suitability for its intended use is also part of the evaluation. According to Fannie Mae's guidelines, a property needs to be evaluated within 12 months preceding the note and mortgage date when obtaining an appraisal. If the date of the original appraisal report is between four and 12 months from the note and mortgage date, an updated appraisal becomes necessary. The update includes a review of current market data and an outside inspection of the property to assess if its value has depreciated since the original appraisal. This mandate stands whether the property's initial appraisal was under proposed or existing construction. When conducting an appraisal update, the appraiser must complete the update within four months prior to the date of the note and mortgage. This is crucial in maintaining the accuracy of the appraisal in a fluid housing market where property values can fluctuate. The appraisal update involves an exterior inspection of the property and a review of the current market data. The appraiser's goal is to identify any significant changes in the property's condition or market value that have occurred since the original appraisal. Ideally, the original appraiser should complete the appraisal update. However, lenders may use substitute appraisers. Substitute appraisers must review the original appraisal report and express an opinion about whether the original appraiser's opinion of market value was reasonable on the date of the original appraisal report. If a substitute appraiser is used, the lender must note in the file why the original appraiser was not used. This protocol ensures consistency and validity in the update process and minimizes potential bias or errors. The inspection and results of the appraisal update must be reported on the Appraisal Update and/or Completion Report (Form 1004D). This form provides a structured way to document any changes in the property's condition or market value since the original appraisal. If the appraiser indicates on the Form 1004D that the property value has declined, then the lender must obtain a new appraisal for the property. Conversely, if the appraiser indicates that the property value has not declined, then the lender may proceed with the loan in process without requiring any additional fieldwork. The results of an appraisal update can directly influence the processing of a mortgage loan. If the update reveals a decrease in property value, the lender is required to order a new appraisal. This could potentially affect the amount of the loan or its approval. On the other hand, if the property value hasn't declined, the loan process continues without further appraisal-related tasks. This underlines the importance of the appraisal update in risk management for both the lender and Fannie Mae. When the effective date of the original appraisal report is more than 12 months from the date of the note and mortgage (with or without an appraisal update), a new appraisal report is required. This rule ensures that the collateral's value supporting the mortgage is current and accurate, minimizing risk for both the lender and Fannie Mae. However, there's an exception for single-close construction-to-permanent financing loans. For other types of loans, these policies apply even if they receive appraisal and value representation and warranty enforcement relief. Fannie Mae requires that all appraisals be completed by a state-licensed or -certified appraiser. These individuals must have the necessary knowledge and experience in valuing properties within the specific geographic location and the particular property type being appraised. Moreover, they must be familiar with Fannie Mae's guidelines and comply with the Uniform Standards of Professional Appraisal Practice (USPAP). The appraiser's qualifications, experience, and adherence to professional standards are vital to the reliability and validity of the appraisal. Lenders are responsible for selecting a qualified appraiser to complete the appraisal. The chosen appraiser should have the right credentials and sufficient experience in appraising similar properties in the same geographic area. Moreover, the appraiser must not be debarred or suspended by any federal or state agency. The selection process must also comply with the Appraiser Independence Requirements (AIR) established by Fannie Mae. These rules prohibit lenders from exerting undue influence over appraisers and protect the appraiser's independence, ensuring a fair and accurate appraisal. The appraisal process starts when a lender orders an appraisal for a property. The appraiser then sets up a time to inspect the property. The inspection involves a thorough walk-through of the property, where the appraiser notes the property's condition, features, and any factors that could affect its value. Photographs are taken, and measurements are made to confirm the property's size and layout. The appraiser also evaluates the quality of the construction, the condition of the roof, the functionality of the systems (like heating and cooling), and other attributes. After the inspection, the appraiser conducts an analysis. This includes researching comparable sales in the area, considering the property's location, and taking into account any other factors that could impact its value. The appraiser prepares a report detailing their findings, providing a justified and supported estimate of the property's market value. The report includes information about the property, an analysis of the local market, a description of the methods used to determine the value, and the appraiser's final value opinion. Once completed, the appraisal report is sent to the lender for review. The lender must ensure that the appraisal meets Fannie Mae's guidelines and that the estimated value is accurate and well-supported. If the appraisal is acceptable, the lender includes it in the loan file. The lender, or a subsequent reviewer, may also submit the report to Fannie Mae as part of a post-purchase review or a quality control process. The appraisal plays a critical role in the mortgage approval process and can impact the loan's final terms and conditions. The value determined by the appraisal directly influences the loan amount a lender is willing to offer. Lenders use the lower of the sales price or the appraised value to determine the loan-to-value ratio (LTV), a key factor in the loan approval process. For example, if a property is appraised lower than the sales price, the lender will use the appraised value to calculate the LTV. This may result in the borrower needing to make a larger down payment to meet the LTV requirements or renegotiating the purchase price with the seller. Meeting Fannie Mae's appraisal requirements can present some challenges. For instance, if a property does not meet the Minimum Property Standards, the lender must require the borrower to complete necessary repairs before closing the loan. Alternatively, the lender could establish an escrow holdback for the required repairs. Another potential challenge is when a property appraises for less than the sales price. In this case, the buyer and seller may need to renegotiate the purchase price, or the buyer may need to increase their down payment. To navigate these challenges, it's crucial for all parties involved - lenders, borrowers, real estate agents - to understand Fannie Mae's appraisal requirements. Engaging a qualified and experienced appraiser is also key to ensuring an accurate, fair, and compliant process. Fannie Mae's appraisal requirements play an indispensable role in securing mortgages, ensuring loans are appropriately collateralized, and limiting financial risk. The guidelines cover various areas, including the qualifications of the appraiser, appraisal report forms, minimum property standards, and more. They stipulate that properties must be evaluated within 12 months before the note and mortgage date and necessitate updates if the initial appraisal is between 4-12 months old. All appraisals must be completed by a state-licensed or certified professional, adhering to stringent criteria to maintain the reliability and validity of the appraisal. The appraisal directly impacts the loan amount a lender offers, establishing a crucial connection between the property's value and the loan-to-value ratio. Understanding these requirements is paramount for lenders, borrowers, and real estate agents, and it aids in navigating any potential challenges, like discrepancies between the sales price and appraisal value.What Is Fannie Mae?

Understanding Fannie Mae Appraisal Requirements

Purpose and Importance of Appraisal Requirements

Brief Summary of Fannie Mae Appraisal Guidelines

Detailed Explanation of Fannie Mae Appraisal Requirements

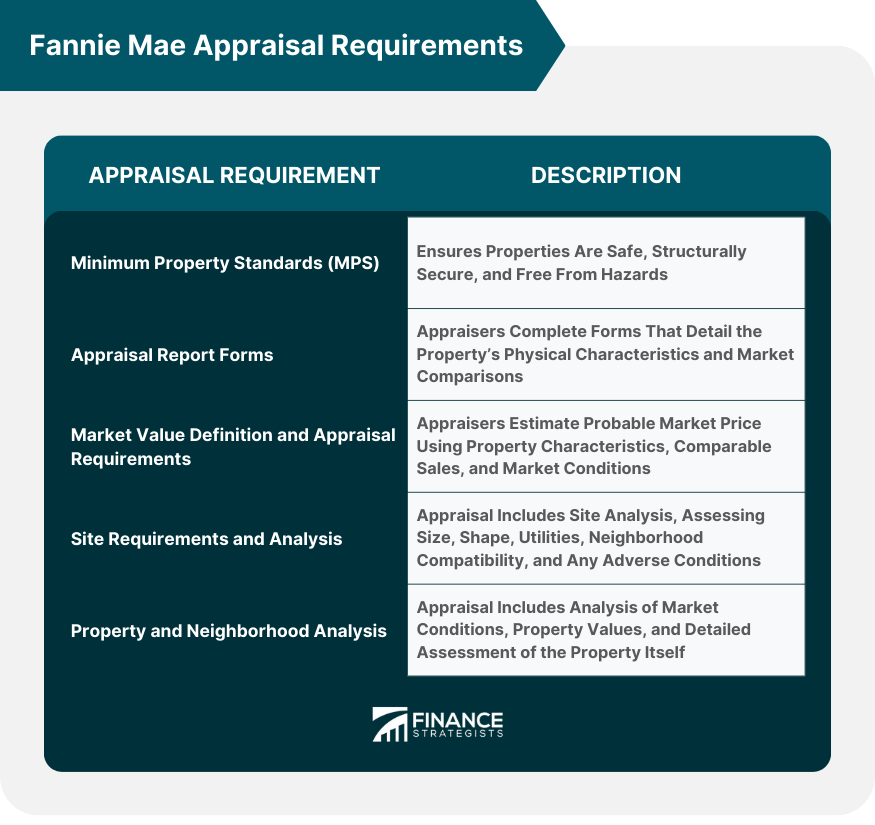

Minimum Property Standards (MPS)

Appraisal Report Forms

Market Value Definition and Appraisal Requirements

Site Requirements and Analysis

Property and Neighborhood Analysis

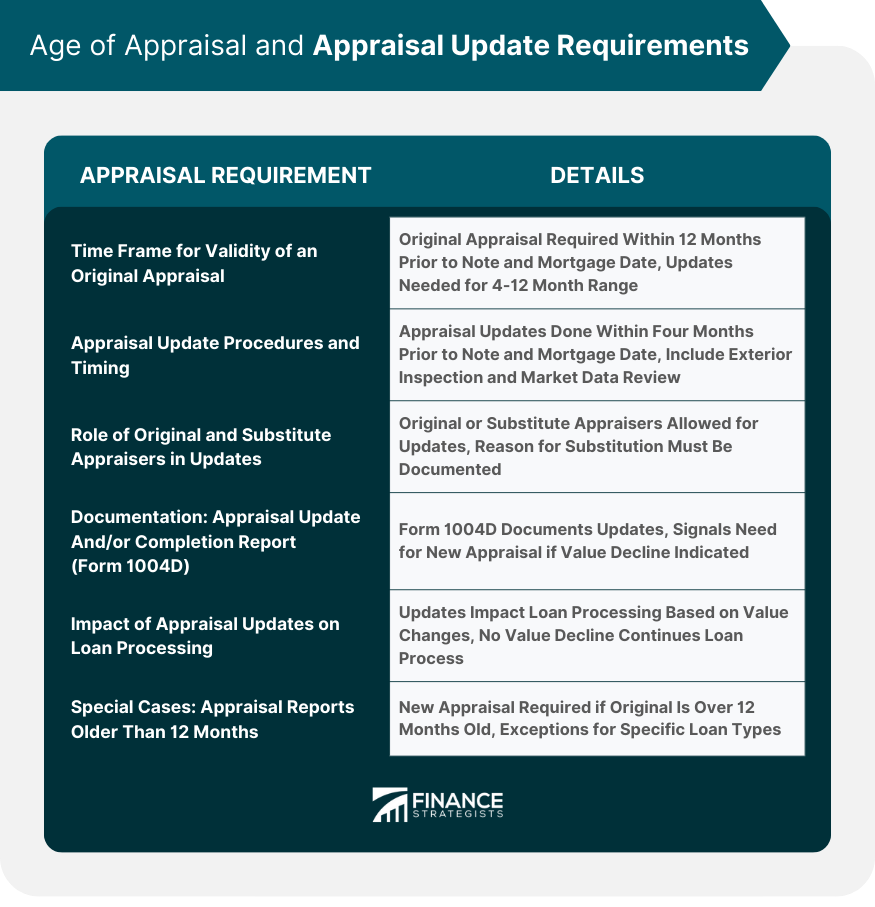

Age of Appraisal and Appraisal Update Requirements

Time Frame for Validity of an Original Appraisal

Appraisal Update Procedures and Timing

Role of Original and Substitute Appraisers in Updates

Documentation: Appraisal Update and/or Completion Report (Form 1004D)

Impact of Appraisal Updates on Loan Processing

Special Cases: Appraisal Reports Older Than 12 Months

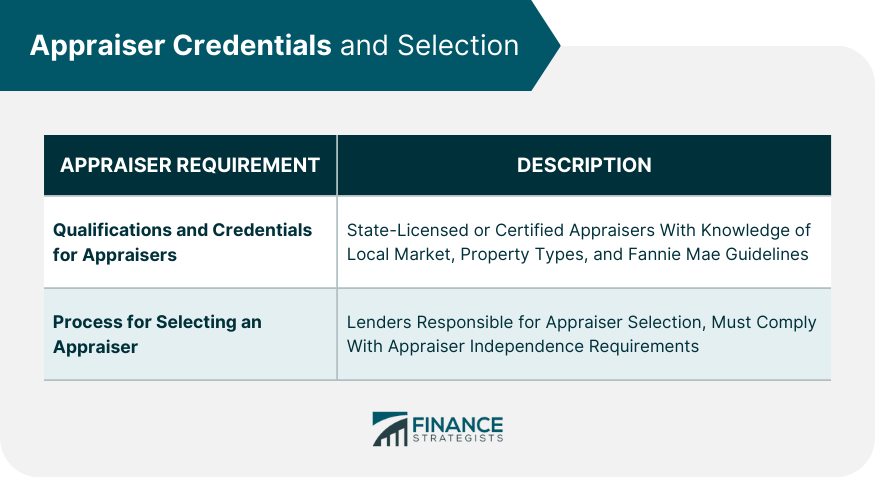

Appraiser Credentials and Selection

Qualifications and Credentials for Appraisers

Process for Selecting an Appraiser

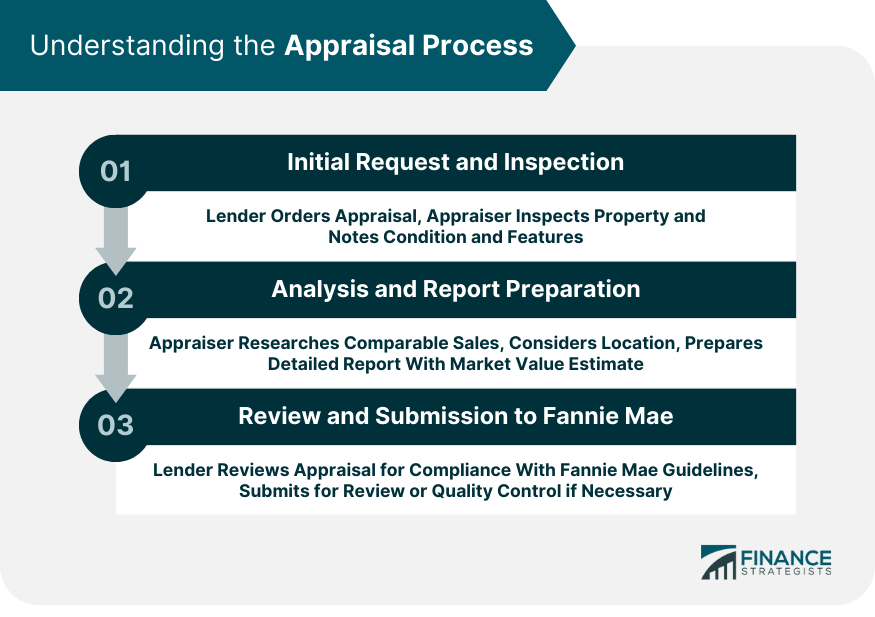

Understanding the Appraisal Process

Initial Request and Inspection

Analysis and Report Preparation

Review and Submission to Fannie Mae

Impact of Appraisal on Loan Approval

How Appraisal Value Influences Loan Amount

Potential Challenges and Solutions in Meeting Appraisal Requirements

Bottom Line

Fannie Mae Appraisal Requirements FAQs

Fannie Mae appraisal requirements stipulate guidelines for the appraisal process, including the qualifications of the appraiser, the contents of the appraisal report, the property's minimum standards, and the methods used to determine its market value.

Appraisals for Fannie Mae must be completed by state-licensed or -certified appraisers who are knowledgeable and experienced in valuing properties within a specific geographic location and type.

Fannie Mae's Minimum Property Standards ensure that the properties financed by Fannie Mae mortgages are safe, sound, and structurally secure, free from hazards that could affect the occupants' health, safety, or the structure's stability.

The appraisal value directly impacts the loan amount a lender offers. Lenders use the lower of the sales price or appraised value to calculate the loan-to-value ratio (LTV), a critical factor in the loan approval process.

If a property doesn't meet Fannie Mae's appraisal requirements, the lender may require necessary repairs before loan closing or establish an escrow holdback. If the appraisal value is less than the sales price, the buyer may need to increase their down payment or renegotiate the purchase price.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.