Fannie Mae HomeStyle Renovation Loan is designed for borrowers looking to purchase and renovate a home using a single loan. Key requirements include eligibility criteria for the property type, which spans single-family homes, multi-unit properties, condos, co-ops, and certain manufactured homes. The loan can finance both the acquisition and renovation of a primary residence, second home, or a refinancing venture. Borrowers must have a satisfactory credit score and adhere to set debt-to-income ratios. The renovation project itself should add value to the property, and a detailed written plan is essential. Contractors involved usually need to meet specific qualifications. Furthermore, the loan takes into account the post-renovation value of the property, influencing terms and amounts. Like all loans, understanding its intricacies ensures borrowers make informed financial decisions. The Fannie Mae HomeStyle Renovation Loan is tailored primarily for single-family homes. This means individual residential units designed to house one family. Whether it’s a new acquisition or an existing property, borrowers can apply for this loan type to finance their renovation projects. If you’re thinking of purchasing or renovating a duplex, triplex, or even a fourplex, you're in luck. The HomeStyle Renovation Loan extends to multi-unit properties, providing flexibility to investors and homeowners alike. Condominiums and co-operatives aren't left out. However, there might be additional guidelines and restrictions when renovating shared spaces or exteriors, so potential borrowers should clarify these details during the application process. While they're a more unconventional choice, manufactured homes are not excluded. There are specific restrictions in place for these properties, often involving stipulations around the home’s foundation and age. Ideal for homeowners looking to buy and renovate their main dwelling, this loan merges both purchase and renovation costs, offering streamlined financial management for borrowers. Not limited to primary residences, the HomeStyle Renovation Loan can also finance the purchase and makeover of a second home, providing more financial tools for those looking to invest or own vacation homes. If you already own a home and are looking to refinance while also funding a renovation, this loan type offers a dual-purpose solution. The loan's ability to combine both purchase and renovation costs under one umbrella offers unparalleled convenience to borrowers. In certain situations, and based on qualifications, borrowers can finance up to 97% of the property’s projected post-renovation value, making the loan exceptionally borrower-friendly. The HomeStyle Renovation Loan is lauded for its adaptability, covering a diverse range of renovation projects that many other loans might exclude. Given its dual nature, the loan process can be intricate, demanding more time and documentation from borrowers. The requirement for comprehensive planning and a plethora of documentation can be daunting for some borrowers. Renovations must align with the loan's disbursement stages, adding an extra layer of project management for the borrower. Funds from the HomeStyle Renovation Loan can be used for a plethora of renovation activities. From general remodeling to essential repairs, or even upgrades for energy efficiency, the possibilities are broad. While flexible, the loan does not cover every type of renovation. Projects that do not add value to the property, like luxury upgrades or extravagant landscaping, might not be covered. A thorough, written description of all planned work is mandatory. This aids lenders in understanding the scope of the project and ensures that the renovations align with loan guidelines. Depending on the property type and borrower's credit profile, down payment requirements can vary. Generally, there's a need for a certain percentage of the home’s purchase price or its appraised value. The LTV ratio is a crucial aspect of this loan. It determines how much of the property's value can be financed. The maximum LTV ratio often hinges on the nature of the property and the renovations being undertaken. One distinctive feature of this loan is the consideration of the post-renovation value. This prospective appraisal helps determine the future worth of the property after all renovations, which can influence the loan terms and amounts. Creditworthiness plays a pivotal role in loan approval. There's a baseline credit score that applicants must meet or surpass to qualify for the HomeStyle Renovation Loan. Lenders scrutinize an applicant's DTI ratio to assess their ability to manage monthly payments. It's a comparison of an individual's monthly debt obligations to their gross monthly income. Ensuring borrowers have a stable source of income is crucial. Applicants must provide relevant employment documentation and proof of consistent income to be considered for the loan. Not all contractors might be suitable for a HomeStyle Renovation project. Lenders often have a list of approved contractors that borrowers can choose from. Experience matters. Contractors should have a proven track record, supported by relevant credentials and references, to be considered for the renovation work. To ensure transparency and fairness, borrowers need to provide detailed bids and estimates from their chosen contractors. This ensures that the projected costs align with the loan amount and the renovation's scope. Before the loan is granted, an appraiser evaluates the property's current value and the projected value post-renovation. This duality ensures lenders have a clear financial picture before lending. Renovations can greatly influence a property’s worth. Thus, the nature, scope, and quality of proposed renovations weigh heavily during the appraisal process. Upon loan approval, an escrow account is usually set up to ensure funds are disbursed appropriately throughout the renovation. Rather than a lump sum, funds are often released in stages or "draws." These phased payments align with project milestones, ensuring work progresses as planned. Lenders will periodically inspect the renovation work. These checkpoints ensure the project adheres to the initial plan and that funds are used judiciously. Borrowers can opt for fixed or adjustable interest rates, each with its own set of pros and cons, which hinge on market conditions and the borrower’s financial situation. The HomeStyle Renovation Loan offers varied term lengths to cater to diverse financial needs, with the most common being 15 to 30 years. Market conditions can influence interest rates. Borrowers should stay abreast of these trends to get the best possible loan terms. Lenders charge origination fees to process the loan. Additionally, there might be other associated costs, all of which should be clarified upfront. Renovation projects might require additional inspections and title updates, both of which can incur added fees. In certain scenarios, especially if the loan carries more risk, lenders might adjust pricing. It's crucial for borrowers to understand all cost implications before committing. Fannie Mae HomeStyle Renovation Loan streamlines the purchase and revamp of properties under one financing umbrella. From single-family residences to condos and select manufactured homes, its flexibility caters to various property types. This loan is not just limited to new acquisitions; it accommodates refinancing endeavors too. Critical to securing this loan is a commendable credit profile and a balanced debt-to-income ratio. Any planned renovations should enhance the home's value, necessitating comprehensive project documentation. Moreover, it's imperative to engage qualified contractors. A distinguishing aspect is its consideration of the home's anticipated post-makeover worth, which dictates loan terms. Ultimately, a deep comprehension of this loan's facets is pivotal for astute financial planning.Fannie Mae HomeStyle Renovation Loan Requirements Overview

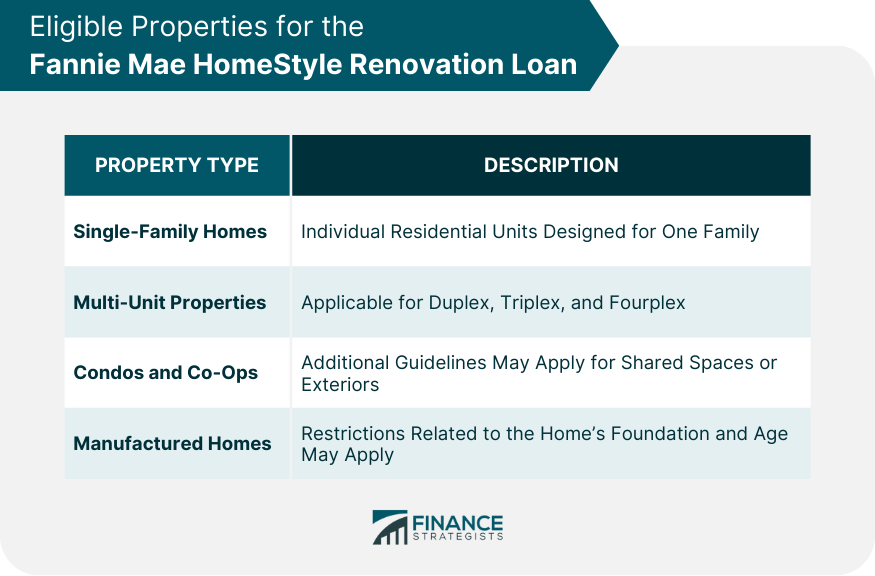

Eligible Properties for the Fannie Mae HomeStyle Renovation Loan

Single-Family Homes

Multi-Unit Properties

Condos and Co-Ops

Manufactured Homes

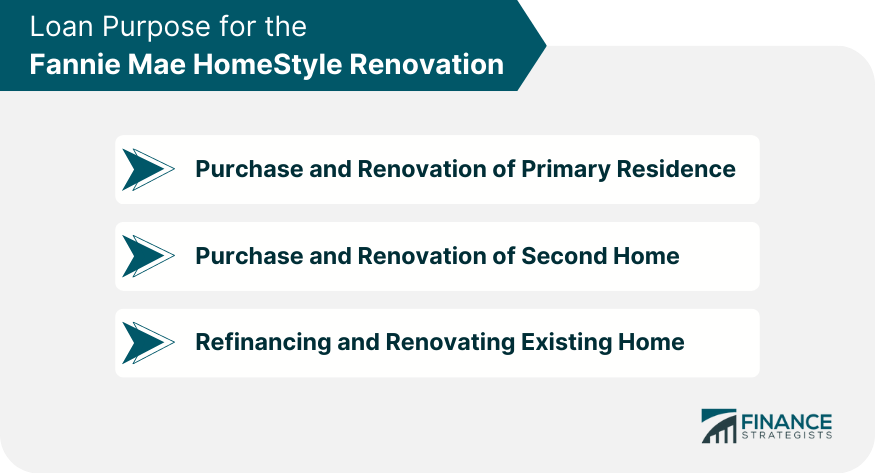

Loan Purpose for the Fannie Mae HomeStyle Renovation

Purchase and Renovation of a Primary Residence

Purchase and Renovation of a Second Home

Refinancing and Renovating an Existing Home

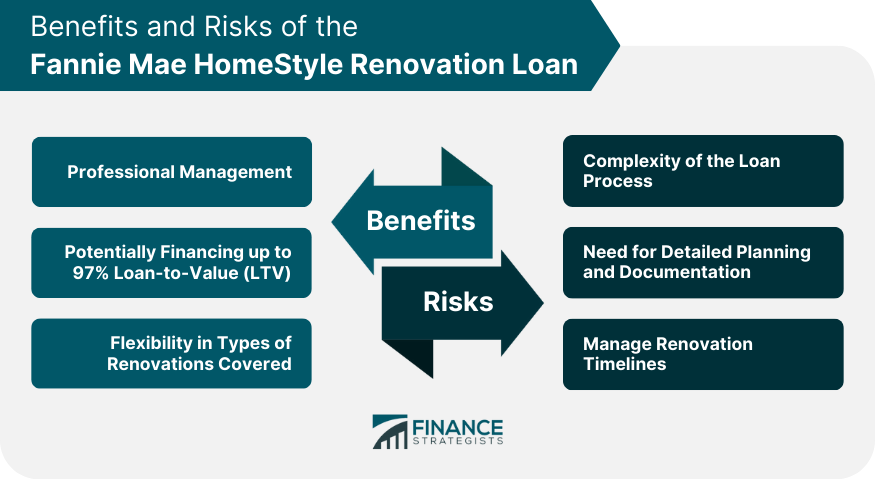

Benefits of the Fannie Mae HomeStyle Renovation Loan

Combining Purchase and Renovation Costs

Potentially Financing up to 97% LTV

Flexibility in Types of Renovations Covered

Risks and Challenges of the Fannie Mae HomeStyle Renovation Loan

Complexity of the Loan Process

Need for Detailed Planning and Documentation

Manage Renovation Timelines

Renovation Project Requirements

Down Payment and Loan-to-Value (LTV)

Minimum Down Payment Requirements

Maximum LTV Ratios

Consideration of Post-renovation Value

Borrower Qualifications

Credit Score Minimums

Debt-to-Income (DTI) Ratio Guidelines

Employment and Income Verification

Contractor Requirements

Use of Approved Contractors

Contractor Experience and Credentials

Requirement for Contractor Bids and Estimates

Appraisal Considerations

Determining the “As-Is” Value Versus the “After-Repair” Value

Importance of the Renovation in the Appraisal Process

Escrow and Draw Process

Setting up a Renovation Escrow Account

Disbursement of Funds in Phases

Inspection Checkpoints

Interest Rates and Loan Terms

Fees and Closing Costs

Conclusion

Fannie Mae HomeStyle Renovation Loan Requirements FAQs

The loan covers a wide range, including single-family homes, multi-unit properties, condos, co-ops, and certain manufactured homes.

Absolutely. This loan not only aids in purchasing and renovating homes but also allows borrowers to refinance and renovate an existing property concurrently.

Borrowers need a detailed written plan of the proposed work. This plan aids lenders in grasping the project's scope, ensuring it adheres to the loan's guidelines.

The loan incorporates an appraisal of the property’s anticipated value post-renovation, which subsequently can influence the loan terms and the amount provided.

Contractors should ideally have relevant experience and credentials. Moreover, lenders might have a list of approved contractors, ensuring quality and reliability for the renovation projects.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.