Securities lending is an arrangement where the owner of a security allows another party to borrow it temporarily. In return, the lender receives compensation. This compensation may come from a lending fee, income from investing cash collateral, or a share of the revenue generated through a lending program. The borrower gives collateral to help protect the lender. Collateral may be cash, government securities, letters of credit, or other approved assets, depending on the arrangement. The loan is usually not meant to be permanent. The borrower returns the securities later, and the lender returns the collateral. This is why securities lending is different from selling an investment. The lender is not trying to exit the position. The lender still has economic exposure to the security, even though the security has been temporarily transferred. Selling an investment means giving up ownership in exchange for cash or other consideration. Once you sell a stock, you no longer participate in its gains or losses unless you buy it back. Securities lending is different. The lender temporarily lends the security but generally continues to have economic exposure to the investment. If the stock price rises or falls during the loan period, that movement still matters to the lender’s portfolio. The borrower must return the security or an equivalent security under the loan agreement. The lender also typically receives substitute payments for dividends or interest that occur while the security is on loan, though these payments may have different tax treatment than regular dividends. So, securities lending is not a sale in the usual investment sense. It is more like renting out an asset while expecting to get it back. Securities lending exists because certain market participants need access to securities they do not currently own. Short sellers may need to borrow shares before selling them short. Broker-dealers may need securities to settle trades. Hedge funds and trading firms may need borrowed securities for hedging, arbitrage, or market-making strategies. On the other side, long-term investors may hold large portfolios of securities they do not plan to sell immediately. Securities lending allows them to potentially earn extra income on those holdings. That creates a market. Borrowers get temporary access to securities. Lenders get potential compensation. The broader market may benefit from improved liquidity, price discovery, and settlement efficiency. But this does not mean securities lending is risk-free. It is a financial transaction with counterparties, collateral, contracts, and operational complexity. The process begins with a securities owner. This may be a mutual fund, ETF, pension fund, insurance company, endowment, hedge fund, bank, or individual investor. The owner has securities in a portfolio and agrees to lend some of them under specific terms. In an institutional setting, securities lending may be managed by a custodian bank or lending agent. In a retail setting, the brokerage firm may operate a fully paid securities lending program. The lender does not usually lend securities randomly. The decision depends on demand, expected compensation, risk controls, collateral standards, and program rules. Hard-to-borrow securities may command higher lending fees because demand is greater and supply is limited. The borrower generally must provide collateral to protect the lender. Collateral is important because the borrower has received a valuable security and must return it later. If the borrower fails to return the security, the lender can use the collateral to help replace the position. Collateral may be cash or non-cash assets. For example, a borrower may provide cash, government securities, or other approved instruments. The SEC has noted that when a securities loan is terminated, the fund returns the collateral to the borrower and the borrower returns the borrowed securities to the fund. Collateral is often marked to market, meaning its value is monitored and adjusted as market prices change. If the value of the borrowed security increases, the borrower may need to provide more collateral. This process helps reduce, but not eliminate, counterparty risk. The borrower pays for the right to borrow the security. The fee depends on supply and demand. Easy-to-borrow securities may have low lending fees. Hard-to-borrow securities may have much higher fees. For example, a widely held large-cap stock may be cheap to borrow because many institutions own it and are willing to lend. A heavily shorted small-cap stock may be expensive to borrow because many traders want to short it and fewer shares are available. In some lending arrangements, the lender earns a direct loan fee. In others, especially when cash collateral is involved, the lender may earn income from reinvesting that cash collateral. The SEC notes that a fund’s income from securities lending may come from borrower fees and/or reinvestment of cash collateral. That income may be shared among the lender, lending agent, brokerage firm, or fund shareholders, depending on the program. Securities lending is temporary. At the end of the loan, the borrower returns the securities to the lender. The lender then returns the collateral to the borrower. Some securities loans are open-ended, meaning they can be terminated by either party under the agreement. Others may have specific terms. If the lender wants to sell the securities, vote on an important corporate matter, or end the loan for risk management reasons, the lender may recall the securities. The mechanics can be smooth in normal markets. But during market stress, operational failures, borrower default, or collateral problems can create risk. That is why securities lending depends heavily on controls, collateral management, and counterparty oversight. These may include mutual funds, ETFs, pension funds, insurance companies, endowments, foundations, and sovereign wealth funds. They often hold large portfolios of stocks and bonds for long-term investment purposes. Since they may not plan to sell certain holdings soon, they can lend them out to generate additional income. For a fund, securities lending income may help offset expenses or modestly improve returns. However, funds must also manage the risks that come with lending. This includes borrower default risk, collateral risk, liquidity risk, operational risk, and conflicts related to voting rights. Broker-dealers often help facilitate securities lending. They may borrow securities from customers, institutions, or other market participants and lend them to hedge funds, short sellers, or other borrowers. They may also use borrowed securities to support settlement or trading activities. Broker-dealers may play multiple roles in the lending chain. They can act as intermediaries, borrowers, lenders, custodians, or program administrators, depending on the situation. Because broker-dealers may interact directly with retail investors through fully paid securities lending programs, disclosure and customer protection rules are especially important. FINRA Rule 4330 addresses the permissible use of customers’ securities and requires member firms to determine the appropriateness of borrowing fully paid or excess margin securities from customers. A short seller borrows shares, sells them in the market, and hopes to buy them back later at a lower price. To do this, the short seller needs access to borrowed shares. Hedge funds may also borrow securities for hedging, arbitrage, market-neutral strategies, or other trading approaches. Borrowing costs matter to these strategies. If the lending fee is high, the short seller must overcome that cost to make a profit. If the borrowed security becomes difficult to locate or the loan is recalled, the borrower may need to cover the position or find another source of shares. Retail investors may participate through fully paid securities lending programs offered by brokerage firms. In these programs, investors allow their broker to lend out fully paid securities from their account. In exchange, the investor may receive a share of the lending income. This can sound attractive because it may generate passive income from securities the investor already owns. But there are trade-offs. The investor may temporarily lose voting rights on loaned shares. Payments received in place of dividends may be treated differently for tax purposes. There may be counterparty and program risks. Investor protections can also vary depending on the structure. FINRA has brought enforcement actions related to fully paid securities lending programs, including sanctions against firms for supervisory and advertising violations. That does not mean all programs are bad. It does mean investors should read the disclosures carefully before enrolling. The most direct reason to lend securities is income. The lender may receive a lending fee or a share of the revenue from the loan. This income can be higher for securities that are in strong demand. For example, a stock with heavy short interest may command a higher lending fee than a widely available blue-chip stock. This income is not guaranteed. It can vary based on market demand, the type of security, the borrower’s needs, and program terms. Still, for large portfolios, even small incremental income can add up. Mutual funds and ETFs may use securities lending to modestly improve fund returns or offset operating expenses. If a fund lends securities and earns revenue, some of that income may benefit fund shareholders. However, fund shareholders should understand how the lending income is split among the fund, adviser, lending agent, or other service providers. The impact may be small in many cases, but over time, it can contribute to performance. The key question is whether the incremental return is worth the added risk. Long-term investors may hold securities for years. Securities lending allows those holdings to produce additional revenue without requiring the investor to sell them. For example, an index fund may hold thousands of securities simply because they are part of the index. Some of those securities may be in demand by borrowers. By lending them, the fund may generate income while maintaining broad market exposure. That is the appeal. The lender maintains the investment strategy while seeking to earn additional returns from securities that would otherwise sit in the portfolio. Short selling is one of the main reasons borrowers take out securities loans. A short seller believes a security’s price may fall. To act on that view, the short seller borrows the security, sells it, and later tries to buy it back at a lower price. If the price falls, the short seller may profit after costs. If the price rises, the short seller may lose money. Borrowed shares are central to this process. Without borrowing, the short seller generally cannot deliver the shares sold into the market. Settlement is the process of completing a securities transaction. If a firm needs to deliver securities but does not have them available at the required time, borrowing may help avoid a failed settlement. This function supports market efficiency. It helps transactions complete properly and reduces friction in the trading system. A hedge fund may borrow a security to offset risk in another position. A trading firm may borrow securities as part of a relative value trade. An arbitrage strategy may involve buying one security and shorting a related one to profit from pricing differences. These strategies can be complex. But the basic idea is the same: the borrower needs temporary access to securities to execute a trading or risk management strategy. Lenders may earn fees from securities they already own. For long-term investors, funds, and institutions, this can create an additional return source without changing the core investment strategy. For retail investors, brokerage stock lending programs may offer a way to earn income from fully paid shares. However, the income may be modest, inconsistent, and dependent on demand. Investors should understand how much of the lending revenue they actually receive and how much the brokerage or lending agent keeps. Securities lending can support market liquidity by making securities available to traders and market makers. When securities can be borrowed more easily, trading can function more smoothly. Borrowing may help with settlement, hedging, and short selling. Liquidity matters because it can make markets more efficient. It may help buyers and sellers transact more easily and may support price discovery. For mutual funds and ETFs, securities lending revenue may help offset fund expenses. This can potentially benefit shareholders if lending income is passed back to the fund. Some index funds use securities lending as one way to reduce the net cost of ownership for investors. The impact depends on the fund, the securities lent, the demand for those securities, the revenue split, and the risks taken. Investors should not assume that all securities lending revenue automatically benefits them equally. The fund’s disclosures matter. Borrowers benefit because securities lending provides access to securities needed for certain strategies. Short selling, hedging, market making, and arbitrage often require borrowed securities. This access can make markets more complete. It allows investors to express negative views, hedge exposures, and pursue relative value opportunities. For the broader market, that can contribute to price discovery. For lenders, it creates a source of demand that may generate lending income. This is the risk that the borrower does not return the securities as required. Collateral is designed to reduce this risk. If the borrower defaults, the lender may use the collateral to replace the securities. But collateral does not eliminate risk. If the collateral value falls, if the securities rise sharply, or if the collateral cannot be liquidated quickly, the lender may suffer a loss. This is why borrowers are screened, collateral is monitored, and loans are marked to market. When the collateral is cash, the lender or lending agent may reinvest it. This can create additional income. It can also create risk. If cash collateral is invested in instruments that lose value or become illiquid, the lender may not have enough cash to return to the borrower when the loan ends. Collateral reinvestment risk became especially important during periods of financial stress, when some supposedly conservative investments proved less liquid or safe than expected. The income from reinvestment can be appealing, but it should not be treated as risk-free. Market risk remains even when securities are lent. The lender usually continues to have economic exposure to the lent security. If the security’s value falls, the lender still experiences that decline. Liquidity risk can also arise if a lender needs securities returned quickly, but the borrower cannot return them immediately, or the market is stressed. In normal conditions, securities lending is often routine. In stressed conditions, recalls, collateral adjustments, and replacement trades can become more difficult. When securities are lent, voting rights generally transfer to the borrower during the loan period. That means the lender may not be able to vote those shares unless the securities are recalled before the record date. This can matter during important corporate events, such as mergers, proxy fights, shareholder proposals, or governance disputes. The SEC has stated that if fund management knows of a material vote related to loaned securities, fund directors should recall the loan in time to vote the proxies. For many investors, voting may not seem important. But for funds, institutions, and governance-focused investors, it can be a major consideration. Tax treatment can change when securities are lent. If a stock pays a dividend while it is on loan, the lender may receive a substitute payment instead of a qualified dividend. That substitute payment may be taxed differently than the original dividend. This matters most in taxable accounts. For retail investors, the tax impact can reduce the value of lending income. A lending program that looks profitable before taxes may be less attractive after taxes. Investors should review the tax implications and consider consulting a tax professional before enrolling in a lending program. Disclosure is important because securities lending has risks that may not be obvious to investors. Retail brokerage programs should explain how the program works, how investors are paid, what rights they give up, what risks exist, and how securities are protected. FINRA’s enforcement actions in this area show that regulators pay attention to how firms supervise and advertise fully paid securities lending programs. For funds, investors should review prospectuses, statements of additional information, annual reports, and other disclosures to understand lending activity and revenue sharing. The borrower must provide collateral to protect the lender if the securities are not returned. The collateral is often marked to market and may require adjustments as values change. High-quality collateral and conservative collateral management can reduce risk. Poor collateral practices can increase risk. Investors should understand not only whether collateral is required, but what kind of collateral is used, how it is valued, where it is held, and what happens if the borrower defaults. Effective securities lending depends on risk management. This includes borrower approval, collateral standards, daily valuation, limits on loan exposure, liquidity controls, legal agreements, indemnification arrangements, and oversight by fund boards or brokerage supervisors. For institutions, securities lending programs are typically governed by formal policies. For retail investors, much of the risk management is handled by the broker. That makes it even more important to understand the brokerage’s role, obligations, and disclosures. Investors should not assume that “fully paid” means “risk-free.” It does not. Securities lending may make sense when the investor understands the program, the compensation is meaningful, the collateral protections are strong, and the risks are acceptable. It may be more attractive for investors holding securities with high borrowing demand. It may also make sense inside certain funds if lending income helps offset expenses and the fund has strong controls. For a long-term investor, lending may seem appealing because it can generate income from securities they planned to hold anyway. But that does not mean every investor should participate. Securities lending may not be worth it when the income is small, the risks are unclear, or the investor values voting rights, dividend treatment, or simplicity more than extra income. It may also be less attractive in taxable accounts if substitute payments create worse tax treatment than regular dividends. Some investors simply do not want the added complexity. That is reasonable. An investment strategy does not need every possible income source to be successful. Look at the revenue split. Review collateral protections. Understand whether voting rights are transferred. Consider tax treatment. Ask whether you can sell securities you have loaned out. Review what happens during borrower default. For funds, review how lending revenue is shared and how risks are managed. For brokerage programs, read the fully paid lending agreement carefully. The central question is simple: Is the extra income worth the added complexity and risk? Securities lending is the temporary transfer of securities from a lender to a borrower in exchange for compensation. It can help lenders earn extra income, support market liquidity, and make short selling, settlement, hedging, and arbitrage possible. It is common among institutions and increasingly available to retail investors through brokerage stock lending programs. But it is not free money. Securities lending comes with borrower default risk, collateral reinvestment risk, liquidity risk, voting rights risk, and potential tax complications. The income may be worthwhile in some cases, but investors should understand the trade-offs before participating. For funds and institutions, securities lending can be a useful portfolio management tool when properly controlled. For individual investors, it should be evaluated carefully. The best approach is to ask what you are earning, what you are giving up, and what could go wrong. If the answer is clear and the compensation is worth the risk, securities lending may have a place. If not, simplicity may be the better choice.Securities Lending: Overview

What Is Securities Lending?

How Securities Lending Differs From Selling an Investment

Why Securities Lending Exists

How Securities Lending Works

The Securities Owner Lends Shares or Bonds

The Borrower Provides Collateral

The Borrower Pays a Lending Fee

The Securities Are Returned Later

Who Participates in Securities Lending?

Institutional Investors

Broker-Dealers

Hedge Funds and Short Sellers

Retail Investors Through Brokerage Programs

Why Do Investors Lend Securities?

Additional Portfolio Income

Improved Fund Returns

Efficient Use of Long-Term Holdings

Why Do Borrowers Borrow Securities?

Short Selling

Settlement Needs

Hedging and Arbitrage Strategies

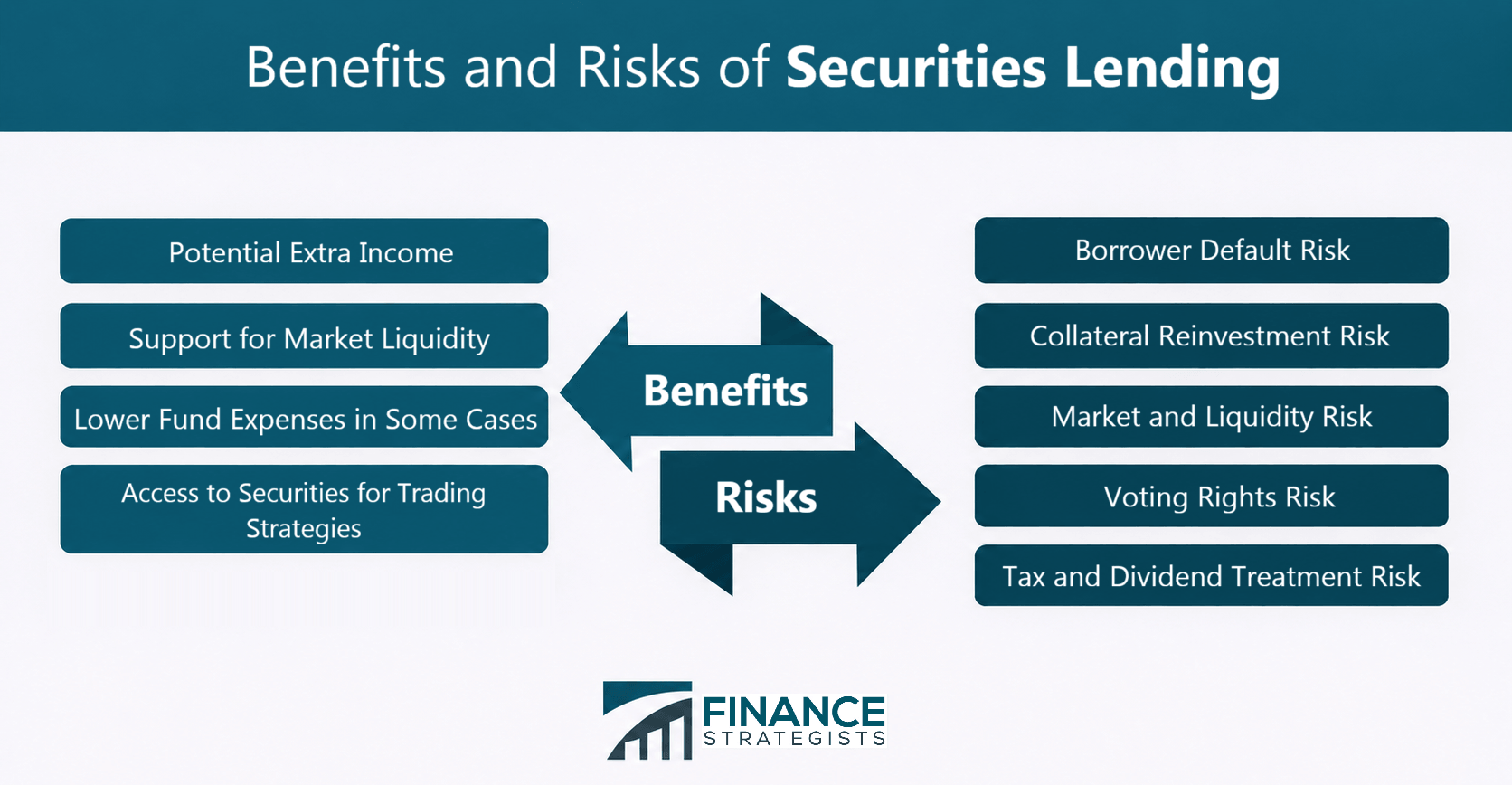

Benefits of Securities Lending

Potential Extra Income

Support for Market Liquidity

Lower Fund Expenses in Some Cases

Access to Securities for Trading Strategies

Risks of Securities Lending

Borrower Default Risk

Collateral Reinvestment Risk

Market and Liquidity Risk

Voting Rights Risk

Tax and Dividend Treatment Risk

Regulation and Oversight of Securities Lending

Disclosure Requirements

Collateral Requirements

Risk Management Practices

Is Securities Lending Worth It?

When Securities Lending May Make Sense

When Securities Lending May Not Be Worth It

How to Evaluate the Trade-Offs

Bottom Line

Securities Lending FAQs

Securities lending is the act of loaning out securities in exchange for collateral. The practice enables investors to generate income from idle securities, while also providing borrowers with the ability to use securities without having to purchase them outright.

There are a number of risks associated with securities lending, including the risk of market value changes, the risk of counterparty default, and the risk of collateral value changes.

Securities lending fees refer to the compensation that lenders receive for loaning out their securities. Securities lending fees are typically calculated by taking the difference between the return rate of the loaned security and an agreed-upon interest rate.

For domestic loans, 102 percent margins must be maintained on the collateral (2% above current market value to cover the potential decrease in the market value of underlying collateral). For loans outside of your home country, you must have collateral worth 105% more than the loan in order to cover any potential losses from market value changes.

Revenue sharing for securities loans is calculated utilizing both total profits and expenses. Customers may be asked to pay a flat percentage of net income or, in some cases, give their whole earnings. The borrower's specific rebate is calculated by each of the securities loans related to them.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.