Fannie Mae HomeStyle Loan is a unique mortgage product that merges the purchase of a home and its renovation into one integrated financing package. This innovative approach is especially valuable for buyers eyeing properties with great potential but in need of repairs or updates. Instead of grappling with multiple loans or deferred renovation dreams, borrowers can capitalize on this offering to buy and customize their space simultaneously. The loan covers a diverse range of property types, from primary residences to investment properties. Whether you're hoping to breathe new life into an older home or aiming to increase the value of an investment property, the Fannie Mae HomeStyle Loan offers a streamlined solution for both financing and renovation aspirations. HomeStyle is a distinctive offering in the sea of mortgage types. It's essentially a conventional loan but comes with a twist: the combination of purchase and renovation financing. At its core, the Fannie Mae HomeStyle loan is a conventional mortgage. This means it isn't backed by the federal government, unlike FHA or VA loans. Because it’s conventional, it might have slightly stricter credit requirements but offers more flexibility in other areas. The loan's primary purpose is dual-faceted. It not only helps borrowers purchase a home but also provides funds for renovations. This is especially useful when buying older homes that might need significant upgrades or repairs. Fannie Mae HomeStyle loans are flexible when it comes to the property type. Whether it's primary residences, second homes, or even investment properties, this loan has got you covered. This broad application makes it a preferred choice for many aspiring homeowners and investors. From structural overhauls to minor cosmetic changes, the HomeStyle loan is accommodating. This feature allows homeowners to truly customize their spaces, turning any property into their dream home. Of course, there are certain requirements borrowers must meet to be eligible for this unique loan offering. Standard financial criteria apply here: a good credit score, acceptable debt-to-income ratios, and a history of responsible borrowing. Specific requirements may vary, but a strong financial profile is a must. Not all properties qualify. While the program is flexible, certain homes or property types might be excluded based on location, condition, or other factors. The renovations must fall within the loan’s guidelines. While the HomeStyle loan is flexible, there are limits to the types of projects that can be financed. The journey from application to final inspection involves several crucial steps. Like any mortgage, it starts with pre-approval, giving you an idea of how much you can borrow. Then, it’s onto the full application, detailing the purchase and planned renovations. You can't pick just anyone. Contractors must be vetted and approved, ensuring quality work that aligns with the proposed plans. After submitting all necessary documents, underwriting will assess your financial stability and the viability of the project. An appraisal will determine the potential post-renovation value of the home. Funds aren’t handed over all at once. They're released in draws, corresponding to the completed phases of the renovation. Each draw is often preceded by an inspection, ensuring work is on track. Forget the hassle of separate loans for purchasing and renovating. With the Fannie Mae HomeStyle loan, both processes are combined, leading to a more streamlined and efficient application process. By financing renovations, homeowners can significantly increase the value of their homes, leading to a rise in home equity. This is a boon for those looking at real estate as an investment. Despite its added benefits, the HomeStyle loan doesn't skimp on competitive interest rates, often making it a more affordable option than taking out second mortgages or HELOCs. Being a conventional loan, the HomeStyle might have tighter credit score demands compared to government-backed options. The process involves multiple inspections which can be time-consuming and, occasionally, intrusive. The appraisal and inspection fees, coupled with potentially higher interest rates, can make this loan pricier in certain scenarios. While both loans cater to renovations, they have distinct differences. FHA 203(k) loans are backed by the federal government and might have more lenient credit requirements, but they come with their own set of constraints regarding renovations and property types. Traditional mortgages simply finance a home purchase. HomeStyle loans, on the other hand, integrate renovation financing. This means while traditional mortgages might have simpler requirements, they don't offer the combined benefit of purchase and renovation. Every loan comes with its costs, and understanding them is vital. Loan origination fees are charges for processing the loan application and can vary based on the lender. Given the nature of the loan, these fees might be higher due to the multiple inspections and the specialized post-renovation appraisal. Navigating the HomeStyle loan process is easier with some strategies in hand. An experienced lender familiar with the HomeStyle program can guide you smoothly through the application and approval phases. Clarity is key. Detailed plans ensure quicker approvals and fewer hiccups during the renovation process. From financial documents to renovation timelines, staying organized ensures you're always one step ahead, making the journey smoother. Fannie Mae HomeStyle Loan offers a transformative approach to home financing by seamlessly blending the purchase and renovation processes. This integrated package is invaluable for individuals aiming to revitalize properties requiring touch-ups or significant repairs. Its broad applicability spans from primary homes to investment properties, ensuring varied real estate aspirations are met. While the loan is celebrated for its streamlined application and potential equity growth, prospective borrowers should be vigilant about its stricter credit prerequisites and the associated costs. Making informed comparisons, such as between the HomeStyle and FHA 203(k) loans, can help in choosing the most suitable financing avenue. Ultimately, the HomeStyle Loan presents an efficient pathway to homeownership and customization, provided one navigates its intricacies with care and expertise.Fannie Mae Homestyle Loan Overview

Features of Fannie Mae HomeStyle Loan

Mortgage Type

Purpose

Property Types Allowed

Flexibility in Improvements

Eligibility Criteria for Fannie Mae HomeStyle Loan

Borrower Eligibility

Property Eligibility

Project Eligibility

How the Fannie Mae HomeStyle Loan Process Works

Pre-approval and Application

Selection and Validation of Contractors

Approval Process

Disbursement of Funds

Pros of Fannie Mae HomeStyle Loan

Streamlined Application Process

Potential for Increased Home Equity

Competitive Interest Rates

Cons of Fannie Mae HomeStyle Loan

Stricter Credit Requirements

Need for Thorough Inspections

Possible Higher Costs

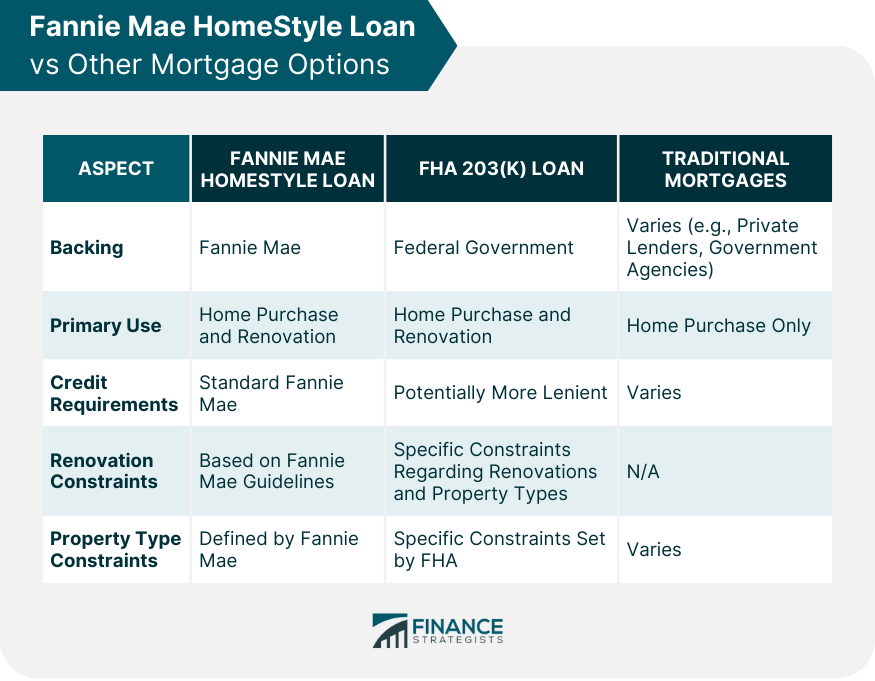

Comparing Fannie Mae HomeStyle Loan With Other Mortgage Options

HomeStyle vs FHA 203(k) Loans

HomeStyle vs Traditional Mortgages

Costs and Fees Associated With Fannie Mae HomeStyle Loan

Loan Origination Fees

Inspection and Appraisal Fees

Tips for a Successful Fannie Mae HomeStyle Loan Application

Working With an Experienced Lender

Preparing a Clear and Detailed Renovation Plan

Staying Organized

Conclusion

Fannie Mae Homestyle Loan FAQs

The Fannie Mae HomeStyle Loan is designed to help borrowers purchase a home and finance renovations simultaneously, making it easier to buy and customize older or damaged properties.

The Fannie Mae HomeStyle Loan covers a range of property types, including primary residences, second homes, and investment properties, offering flexibility for various real estate needs.

While both loans cater to renovation needs, the Fannie Mae HomeStyle Loan is a conventional mortgage not backed by the federal government, unlike the FHA 203(k) loan. The HomeStyle Loan may have stricter credit requirements but offers more flexibility in renovation types and property choices.

Yes, for projects financed by the Fannie Mae HomeStyle Loan, contractors must be vetted and approved to ensure quality and adherence to the proposed renovation plans.

Some potential drawbacks of the Fannie Mae HomeStyle Loan include stricter credit requirements compared to some government-backed loans, the need for multiple inspections, and possibly higher costs due to appraisal and inspection fees.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.