The Fannie Mae condo guidelines serve as a blueprint for condominium associations, buyers, and lenders, establishing specific criteria that must be met for a condominium to qualify for financing backed by Fannie Mae. These guidelines consider factors such as owner occupancy ratios, delinquency rates on condo fees, insurance coverage, and budgetary practices. For new or newly converted condos, the developer's plans, selling practices, and project feasibility are closely scrutinized. The guidelines also outline a streamlined Limited Review Process for certain transactions. Non-compliance with these guidelines can restrict access to financing, impacting both condo associations and prospective buyers. Thus, understanding and adhering to the Fannie Mae condo guidelines is crucial for the financial viability and marketability of condo projects. For new or newly converted condo projects, Fannie Mae's guidelines are rather strict, reflecting the higher level of risk often associated with new developments. The guidelines require a more comprehensive review, including a close examination of the developer's plans, selling practices, and project feasibility. Important parameters such as pre-sale requirements, owner occupancy ratios, and association budgetary practices come under careful scrutiny. In contrast to new developments, established condo projects face slightly more relaxed guidelines. The review process for established projects involves checking compliance with financial requirements, occupancy ratios, insurance coverage, and legal stipulations. However, established condo projects with a high percentage of non-owner-occupied units or those with a significant number of units in delinquency might face challenges in meeting the guidelines. One of the key eligibility requirements according to Fannie Mae condo guidelines is the owner-occupancy ratio. The association must ensure that a certain percentage of the total units are owner-occupied. This percentage aims to maintain a healthy balance between owner-occupied and non-owner-occupied units, promoting a stable living environment and reducing the risk of mortgage default. Another crucial eligibility requirement is the delinquency rate. Condo associations must demonstrate that no more than a specific percentage of condo units are 60 days or more past due on their association dues. High delinquency rates could indicate financial instability and, thus, make lenders wary of extending mortgage financing for units in the project. Fannie Mae condo guidelines stipulate that condo associations must have adequate insurance coverage, including general liability, fidelity, and hazard insurance. Furthermore, in regions prone to specific natural disasters, additional policies, such as flood or earthquake insurance, may be required. The guidelines also require condo associations to have a budget that adequately caters to operating expenses, maintains appropriate reserve funds, and accounts for bad debts. The budget must include allocations for various expenses like management fees, utility expenses, and funds for routine maintenance and repair. The limited review process is a streamlined version of the condo project evaluation, applicable for certain transactions. Eligibility criteria for a limited review include lower loan-to-value ratios, indicating substantial borrower investment, and primary residence or second home transactions. It's important to note that not all condominium projects will qualify for a limited review. In the limited review process, fewer items are scrutinized compared to the full review process. For instance, the evaluation of the association's budget, insurance coverage, and litigation may not be as exhaustive. This process can expedite the loan approval process and make it easier for eligible borrowers to secure mortgage financing. However, it's crucial to remember that a limited review still necessitates compliance with fundamental eligibility criteria. The full review process is the standard procedure for assessing a condo project's eligibility. This process is required when a project does not meet the criteria for a limited review or when the transaction involves a higher loan-to-value ratio, investment property, or two- to four-unit projects. The full review process is more comprehensive, scrutinizing all elements of the condo project. It reviews factors such as the project's legal documents, financial stability, owner occupancy ratios, insurance coverage, and more. While the full review process can be more time-consuming, it provides a thorough assessment of the condo project's sustainability and risk factors. Fannie Mae provides a specific review service called the Project Eligibility Review Service (PERS). This is a discretionary review process that condo projects can opt for, particularly when they do not meet all standard eligibility requirements. PERS approval can provide an advantage in the competitive housing market by offering an additional level of assurance to lenders and prospective buyers. The special approval designation process includes a thorough review of the project, similar to the full review process. However, it also considers compensating factors that might offset specific project deficiencies. The process is detailed and requires the submission of a complete project package for Fannie Mae's review. Condo projects that successfully receive this special approval designation demonstrate a level of stability and viability, making them attractive to potential buyers and lenders. Non-compliance with Fannie Mae condo guidelines can have significant consequences for condo buyers. A condo project that doesn't meet Fannie Mae's guidelines might struggle to attract buyers, as it could be challenging for potential buyers to secure financing. This situation could restrict the marketability of units within the project and potentially impact unit prices. For condo associations, non-compliance can lead to difficulties in attracting new buyers or retaining existing owners. A lack of Fannie Mae compliance might also result in lower property values, financial instability, and a deteriorating reputation. This could lead to a cycle of non-occupancy, delinquency, and financial hardship. For buyers, due diligence is crucial. Working with a knowledgeable real estate agent and getting a preapproval letter can help navigate the complex landscape of Fannie Mae guidelines. Buyers should also consider engaging legal counsel to review condo documents, including association bylaws and financial statements, to ensure compliance with Fannie Mae guidelines. Condo associations can overcome challenges by ensuring they meet the required owner-occupancy ratios, maintaining a healthy financial standing, and keeping delinquencies to a minimum. Regular reviews and updates of the association's policies and legal documents can also help maintain compliance with Fannie Mae condo guidelines. Additionally, employing professional property management services can be beneficial in navigating the complexities of Fannie Mae's compliance. Fannie Mae condo guidelines play a crucial role in maintaining the financial stability and marketability of condo projects. These guidelines define clear criteria for new and established projects alike, including owner occupancy ratios, delinquency rates, insurance requirements, and budgetary practices. The Limited Review Process serves as a streamlined method for certain transactions, while the Full Review Process provides a comprehensive assessment. Special designations like PERS can offer additional assurance for lenders and buyers. Non-compliance with these guidelines can significantly impact both condo associations and buyers, influencing marketability, property values, and financial stability. Therefore, a thorough understanding of these guidelines and adherence to them is paramount for the sustained success of condo projects.Fannie Mae Condo Guidelines Overview

Fannie Mae's Condo Project Review Requirements

New and Newly Converted Condo Projects

Established Condo Projects

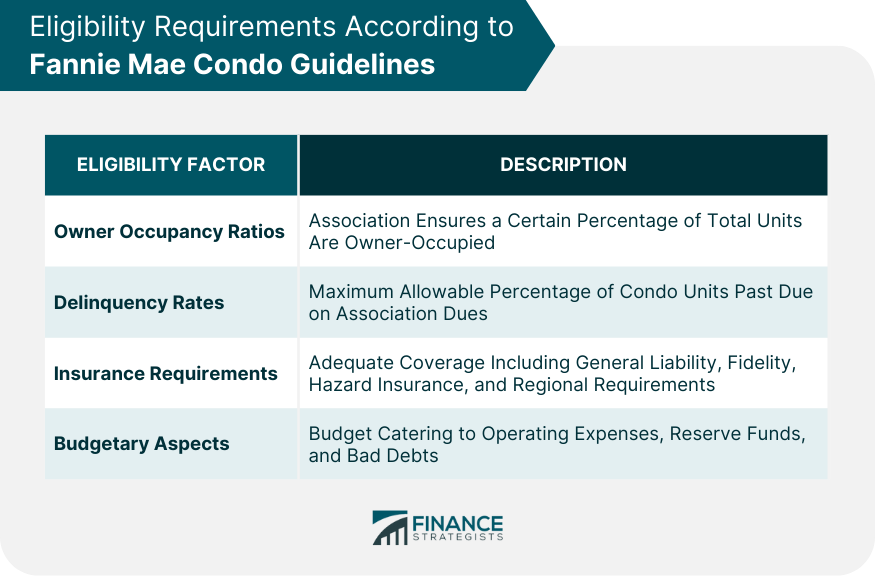

Eligibility Requirements According to Fannie Mae Condo Guidelines

Owner Occupancy Ratios

Delinquency Rates

Insurance Requirements

Budgetary Aspects

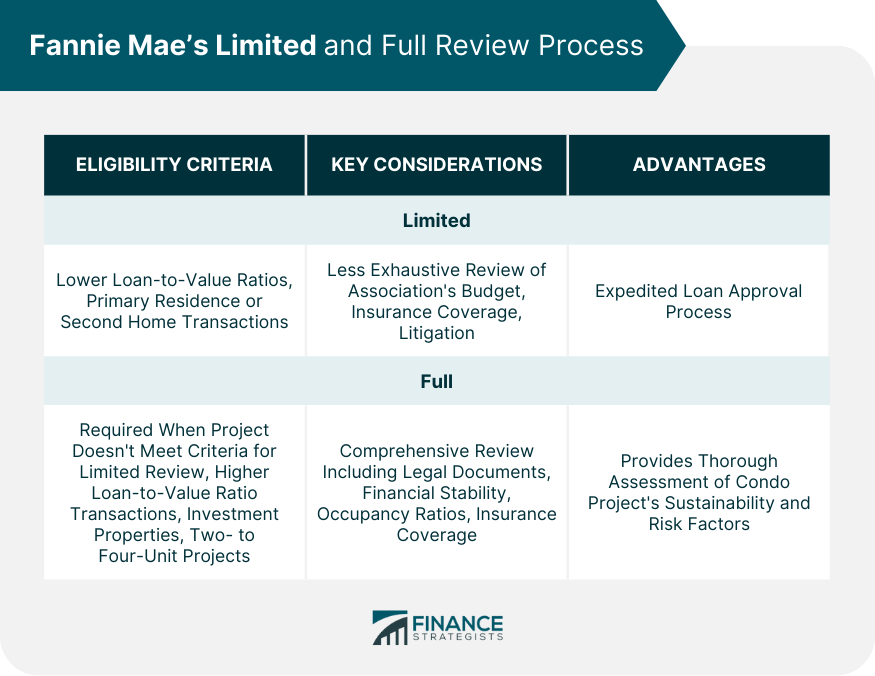

Fannie Mae’s Limited Review Process

Eligibility Criteria for Limited Review

Limited Review Process and Its Advantages

Fannie Mae's Full Review Process

Eligibility Criteria for Full Review

Full Review Process and Its Considerations

Special Approval Designations by Fannie Mae

Project Eligibility Review Service (PERS)

Fannie Mae's Special Approval Designation Process

Consequences of Non-compliance With Fannie Mae Condo Guidelines

Potential Impacts on Condo Buyers

Potential Impacts on Condo Associations

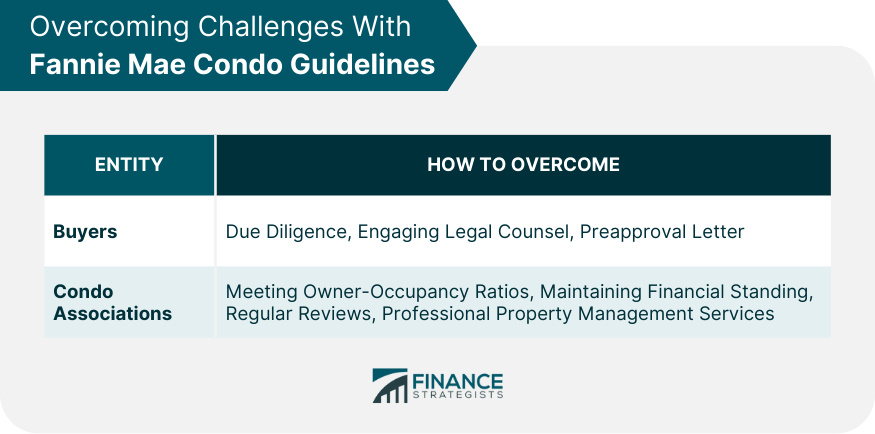

Overcoming Challenges With Fannie Mae Condo Guidelines

Strategies for Buyers

Strategies for Condo Associations

Conclusion

Fannie Mae Condo Guidelines FAQs

The Fannie Mae condo guidelines take into account a range of factors, including owner occupancy ratios, delinquency rates, insurance requirements, and budgetary practices. Each of these factors plays a significant role in the financial stability and overall viability of the condo project.

The Fannie Mae condo guidelines significantly impact condo buyers as they establish the eligibility criteria for financing. A condo project not meeting these guidelines can make it difficult for potential buyers to secure mortgage financing, thereby affecting the unit's marketability and pricing.

Under the Fannie Mae condo guidelines, new or newly converted condo projects undergo a more comprehensive review process that scrutinizes the developer's plans, selling practices, and project feasibility. Established condo projects, on the other hand, are reviewed based on factors like compliance with financial requirements, occupancy ratios, insurance coverage, and legal stipulations.

The Limited Review Process in the Fannie Mae condo guidelines provides a streamlined evaluation for certain transactions, speeding up the loan approval process. However, it's important to note that not all condominium projects will qualify for this type of review, and they must still meet certain fundamental eligibility criteria.

Failure to comply with Fannie Mae's condo guidelines can lead to significant consequences for both condo buyers and condo associations. It could potentially limit the marketability of units, lower property values, and lead to financial instability, making it difficult to attract new buyers or retain existing owners.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.