Permanent life insurance is a type of life insurance policy that provides coverage for the entire lifetime of the insured as long as the premiums are paid. Unlike term life insurance, which offers coverage for a specified term, permanent life insurance offers lifelong protection. It combines a death benefit with a cash value component, which grows over time. The cash value can be accessed by the policyholder through policy loans or withdrawals, providing a source of funds for various financial needs. Permanent life insurance offers stability, flexibility, and the potential for long-term growth, making it an important option for individuals seeking lifelong coverage and financial security. Whole life insurance is a type of permanent life insurance that guarantees lifelong coverage, provided premiums are paid. This policy features level premiums, meaning that the cost remains the same throughout the policy's duration. Additionally, whole-life policies accumulate cash value over time, which can be borrowed against or withdrawn under specific circumstances. Universal life insurance offers more flexibility than whole life insurance, as it allows policyholders to adjust their premiums and death benefits within certain limits. This type of permanent life insurance also includes an investment component, with a portion of the premiums allocated to a cash value account that grows at a minimum guaranteed interest rate. Indexed universal life insurance is a variation of universal life insurance that ties the policy's cash value growth to the performance of a stock market index, such as the S&P 500. This means that the policy's cash value can increase when the index performs well, providing potentially higher returns than traditional universal life insurance. However, indexed policies typically include a cap on returns and a floor to protect against negative market performance. Variable life insurance is another type of permanent life insurance that offers an investment component, allowing policyholders to invest the cash value in a variety of sub-accounts, such as stocks, bonds, and mutual funds. While this option provides the potential for higher returns, it also carries a greater level of risk due to market fluctuations. Selecting the appropriate permanent life insurance policy involves the following steps: Determine the desired coverage amount, taking into account factors such as income replacement, debt repayment, and future expenses (e.g., college tuition, retirement). Compare different types of permanent life insurance policies to determine which one best aligns with personal financial goals and risk tolerance. Obtain quotes from multiple insurance providers to compare costs and coverage options, ensuring the best value for the desired policy. Consult with an expert to help navigate the complexities of permanent life insurance and make an informed decision. Permanent life insurance policies offer several advantages, including: Lifetime Coverage: As long as premiums are paid, the policy remains in force, providing lifelong protection for the insured's beneficiaries. Cash Value Accumulation: A portion of the premiums paid is allocated to a cash value account, which grows tax-deferred over time and can be accessed for various purposes. Tax Advantages: Permanent life insurance policies offer tax-free death benefits, tax-deferred cash value growth, and potentially tax-free policy loans and withdrawals. Fixed Premiums (For Some Policies): Whole life insurance policies feature level premiums, ensuring that the cost remains the same throughout the policy's duration. Policy Loans and Withdrawals: Policyholders can borrow against the cash value or make withdrawals, providing financial flexibility during their lifetime. While both permanent and term life insurance provide financial protection, there are key differences between the two: Coverage Duration: Permanent life insurance provides lifetime coverage, whereas term life insurance offers coverage for a specific period (e.g., 10, 20, or 30 years). Cash Value: Permanent life insurance policies include a cash value component, while term life insurance policies do not. Premiums: Permanent life insurance policies typically have higher premiums due to the lifetime coverage and cash value features. When choosing between permanent and term life insurance, individuals should consider factors such as their financial goals, budget, and need for lifetime coverage. Permanent life insurance is a valuable financial tool that offers lifelong protection, investment opportunities, and tax advantages. By exploring the different types of policies available, such as whole life, universal life, indexed universal life, and variable life insurance, individuals can tailor their coverage to meet their unique needs and financial goals. Permanent life insurance policies provide numerous benefits, including lifetime coverage, cash value accumulation, and financial flexibility through policy loans and withdrawals. When selecting the right policy, it is crucial to assess one's financial goals and needs, compare quotes from different insurers, and consult with an expert to make an informed decision. Ultimately, permanent life insurance can provide peace of mind, financial security, and wealth building opportunities for both the policyholder and their beneficiaries.Definition of Permanent Life Insurance

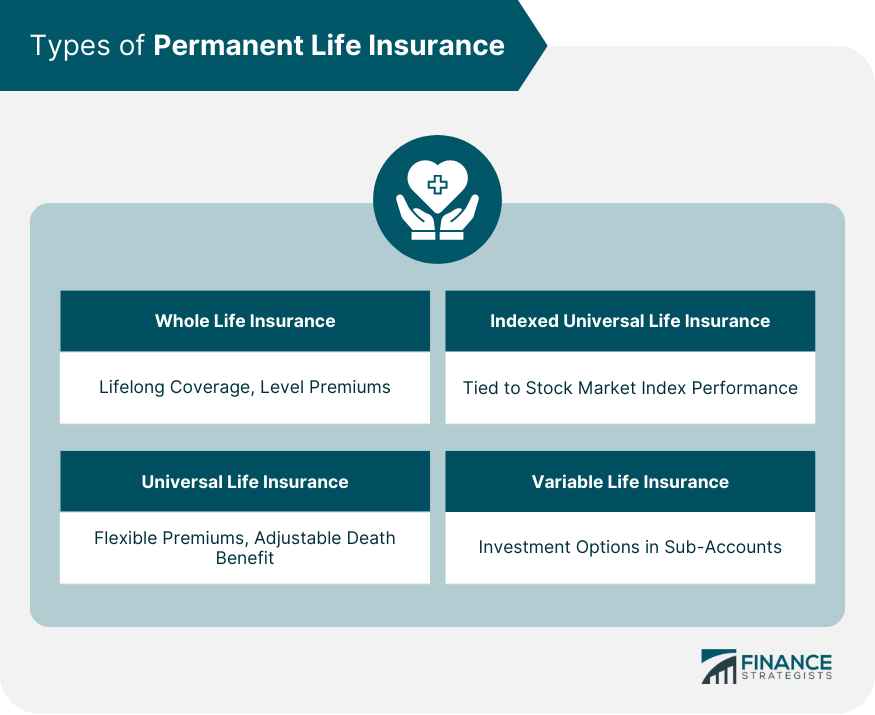

Types of Permanent Life Insurance

Whole Life Insurance

Universal Life Insurance

Indexed Universal Life Insurance

Variable Life Insurance

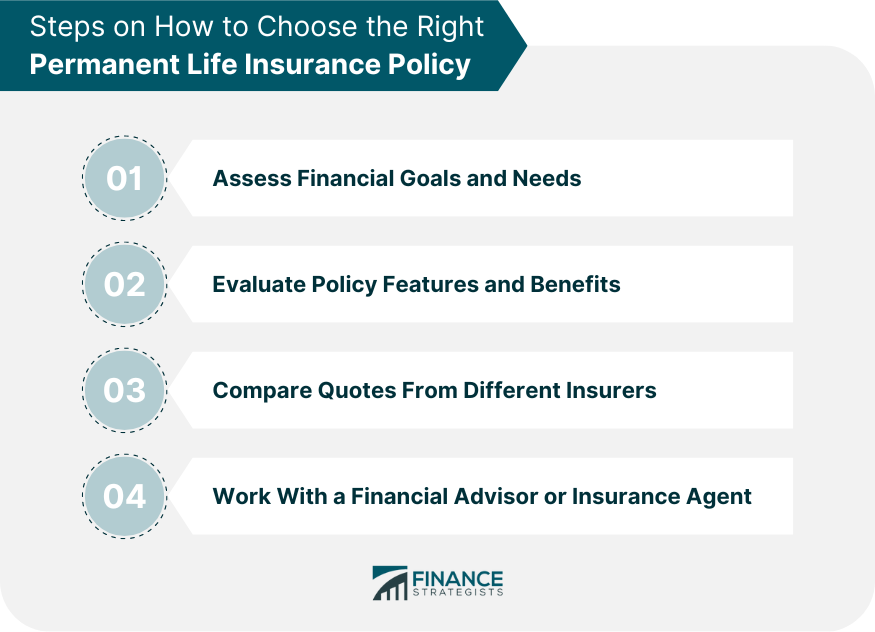

How to Choose the Right Permanent Life Insurance Policy

Assessing Financial Goals and Needs

Evaluating Policy Features and Benefits

Comparing Quotes From Different Insurers

Working With a Financial Advisor or Insurance Agent

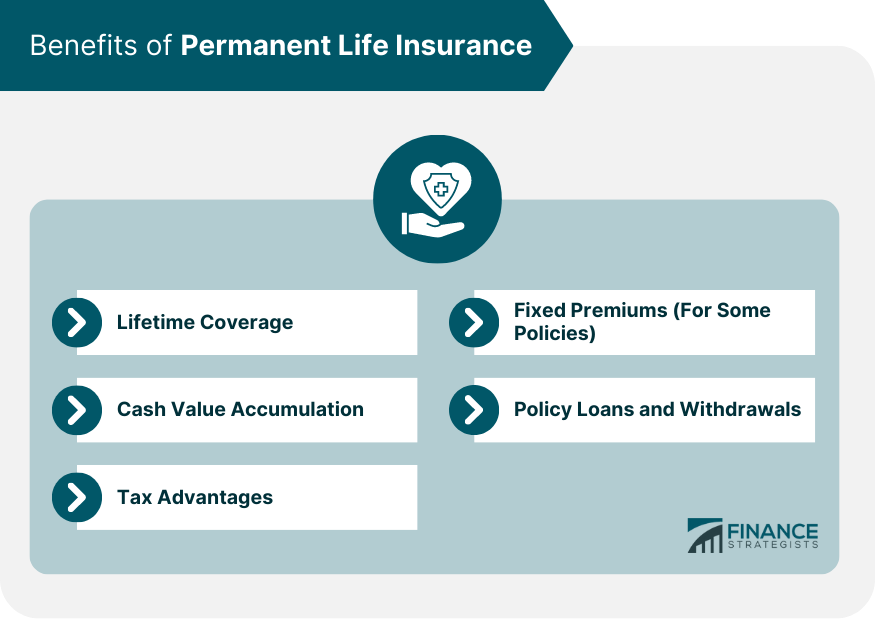

Benefits of Permanent Life Insurance

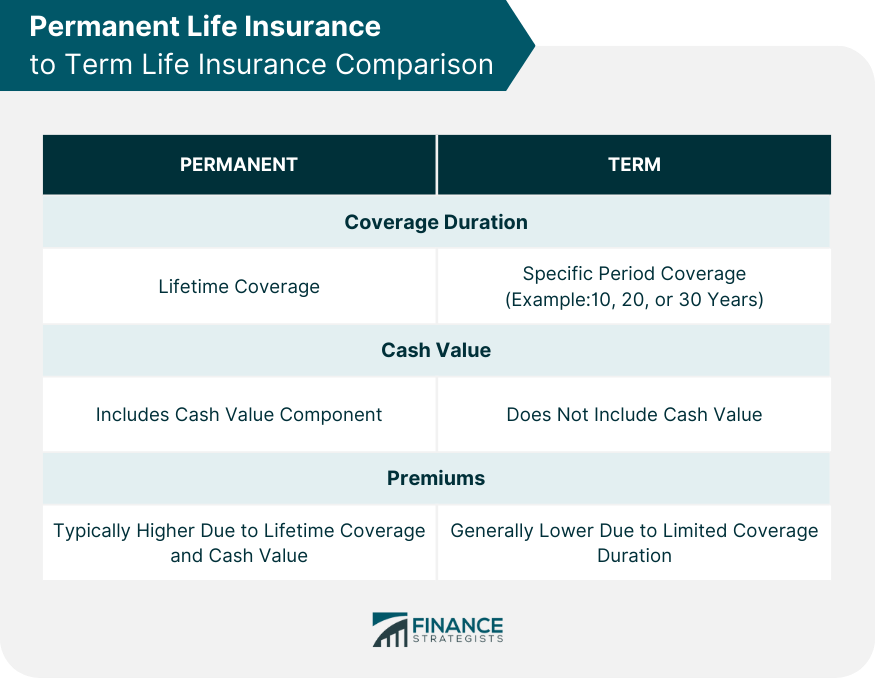

Comparing Permanent Life Insurance to Term Life Insurance

Bottom Line

Permanent Life Insurance FAQs

Permanent life insurance provides lifetime coverage and includes a cash value component, while term life insurance offers coverage for a specific term and does not have a cash value feature.

Yes, most permanent life insurance policies allow you to take out policy loans using the accumulated cash value as collateral, providing financial flexibility.

Consider your financial goals, risk tolerance, and budget when selecting a permanent life insurance policy. Compare policy features, benefits, and quotes from different insurers to make an informed decision.

Typically, yes. Permanent life insurance policies have higher premiums due to the lifetime coverage and cash value component, which are not present in term life insurance policies.

Cash value growth in permanent life insurance policies is tax-deferred. Taxes may be owed when accessing the cash value through withdrawals or loans, depending on the circumstances.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.