Capital gains tax on goodwill refers to the tax levied on the profit realized when a business is sold and part of the selling price is attributed to its goodwill. Goodwill, an intangible asset, represents the excess value of a business over its tangible assets and liabilities. When a business is sold, the selling price is allocated among its assets, including goodwill. The gain on goodwill, calculated as the selling price less its original cost, is subject to capital gains tax. This tax is typically at a long-term rate, as goodwill is considered a long-term asset. The exact tax implications can be complex and vary based on factors such as the seller's tax status and specific tax laws, making professional advice essential when dealing with capital gains tax on goodwill.

To apply capital gains tax, the selling price of the business must be allocated among all its assets, including goodwill. The portion assigned to goodwill is typically based on an appraisal or valuation that assesses the value of the business's intangible assets. The gain from the sale of goodwill is the difference between the selling price allocated to goodwill and the original cost of goodwill. In most cases, the original cost of goodwill for the seller is zero, as goodwill is self-created and does not have a purchase cost. Hence, the entire amount allocated to goodwill in the selling price could be considered a capital gain. The capital gains tax is applied based on the calculated gain and the current tax rates. If the business has held the goodwill for more than one year, it is generally considered a long-term capital gain and is subject to lower tax rates. However, if the goodwill is sold within a year of its creation, the gain may be classified as short-term and taxed at ordinary income tax rates. When a business is bought, the purchase price is allocated among its tangible and intangible assets, including goodwill. Goodwill is the excess value of the purchase price over the fair market value of tangible assets and identifiable intangible assets. For the buyer, goodwill becomes a purchased asset with tax implications. From a buyer's perspective, purchased goodwill can be amortized - that is, its cost can be gradually written off as an expense over a certain period of time. In the United States, for instance, the Internal Revenue Service (IRS) allows goodwill to be amortized on a straight-line basis over 15 years. This amortization can reduce the taxable income of the buyer, potentially leading to significant tax savings over time. If the buyer eventually sells the business, the amount of amortized goodwill can influence the capital gains tax liability. The sale price will be compared to the business's adjusted basis - its original purchase price minus the amount of goodwill that has been amortized. Any gain from the sale would be subject to capital gains tax. Buyers must also be mindful of changes in tax laws which can impact how goodwill is treated for tax purposes. Changes that affect the amortization period or how goodwill is recognized could alter the tax implications of buying goodwill. Keeping abreast of current and proposed changes to tax laws is thus a critical aspect of managing the tax implications of buying goodwill. Goodwill is an intangible asset that represents the excess of a business's purchase price over the fair market value of its net tangible assets. It can encompass factors such as customer relationships, brand reputation, and intellectual property, among others. When a business is sold, the value of goodwill is typically a significant component of the transaction. The first step in calculating capital gains tax on goodwill is allocating the purchase price of a business to its various assets, including goodwill. This process, also known as purchase price allocation, involves assigning a portion of the total purchase price to each identifiable asset and liability, with any remaining amount allocated to goodwill. Once the value of goodwill is determined, the next step is to calculate the gain. The gain on goodwill is calculated as the selling price of the goodwill less its original cost (often the cost recognized when the business was originally purchased or established). This gain is what's subject to capital gains tax. The final step involves applying the appropriate capital gains tax rate. For goodwill, this is typically the long-term capital gains tax rate since goodwill is considered a long-term asset. However, the tax rate may vary depending on specific tax laws and the seller's tax status. It's crucial to consult with a tax professional or use updated tax software to ensure the correct tax rate is applied. The calculated capital gains tax on goodwill must be reported on the seller's tax return in the year the business was sold. Specific forms and reporting procedures may apply, depending on the tax jurisdiction. Goodwill plays a significant role in mergers and acquisitions (M&A) as it often makes up a large portion of the purchase price. It can make a company more attractive to potential buyers, and it can also significantly affect the tax implications of the transaction. When a company is sold, the amount of the purchase price attributed to goodwill is taxed as a capital gain. Depending on the holding period of the business, the gain on goodwill could be taxed at either the long-term or short-term capital gains rate. This can have a significant impact on the net proceeds the seller receives from the sale. On the other side, the buyer of a company can amortize the cost of purchased goodwill over a period of 15 years, according to IRS rules. This allows the buyer to reduce their taxable income over time, leading to potential tax savings. However, if the value of the goodwill decreases or becomes impaired, the buyer may be able to claim a tax deduction for the loss. One tax strategy for selling a business with significant goodwill is to use an installment sale. This allows the seller to spread the gain over multiple years, potentially reducing the overall tax burden. However, the seller will need to weigh the tax benefits against the risks of deferring the receipt of the sale proceeds. Another strategy involves choosing the structure of the transaction. In an asset sale, individual assets and liabilities of the business are sold, which often leads to a higher tax bill for the seller but allows the buyer to step-up the basis of the purchased assets. In a stock sale, the seller's shares in the business are sold, resulting in one level of tax and potential tax preferential rates for the seller. Under Section 1031 of the tax code, sellers can defer recognizing capital gains tax on the sale of business assets if they reinvest the proceeds in similar assets within a specific time frame. While this exchange primarily applies to real estate transactions, there's some debate among tax professionals about its applicability to goodwill. The IRS has not provided clear guidance on this matter, adding an additional layer of complexity. The IRS has specific rules and regulations regarding goodwill and how it's treated for tax purposes. Any gain or loss from the sale of goodwill is treated as a capital gain or loss and is subject to the applicable capital gains tax rates. Various court cases and legal precedents impact the treatment of capital gains tax on goodwill. It's crucial for businesses and tax professionals to stay updated on such developments to ensure they are in compliance and are utilizing the most effective tax strategies. Changes in tax laws can have significant impacts on the capital gains tax on goodwill. For instance, changes in the tax rates, holding period requirements, or the definition of goodwill can change the tax implications of selling a business. Businesses must monitor potential tax law changes and adapt their tax strategies accordingly. Capital gains tax on goodwill carries significant implications for both sellers and buyers in business transactions. Goodwill, often a substantial component of a company's value, is taxed as a capital gain upon sale, with tax rates influenced by factors such as holding periods and specific tax laws. Buyers, on the other hand, can amortize the cost of purchased goodwill over 15 years, potentially yielding significant tax savings. Legal and regulatory considerations, including IRS rules, court precedents, and tax law changes, are pivotal to understanding and managing these tax obligations. Strategic approaches, such as installment sales, choosing the transaction structure, and potentially utilizing Section 1031 exchanges, can help mitigate tax liabilities. Given the complexities involved, professional advice is paramount when navigating the capital gains tax landscape related to goodwill.Capital Gains Tax on Goodwill Overview

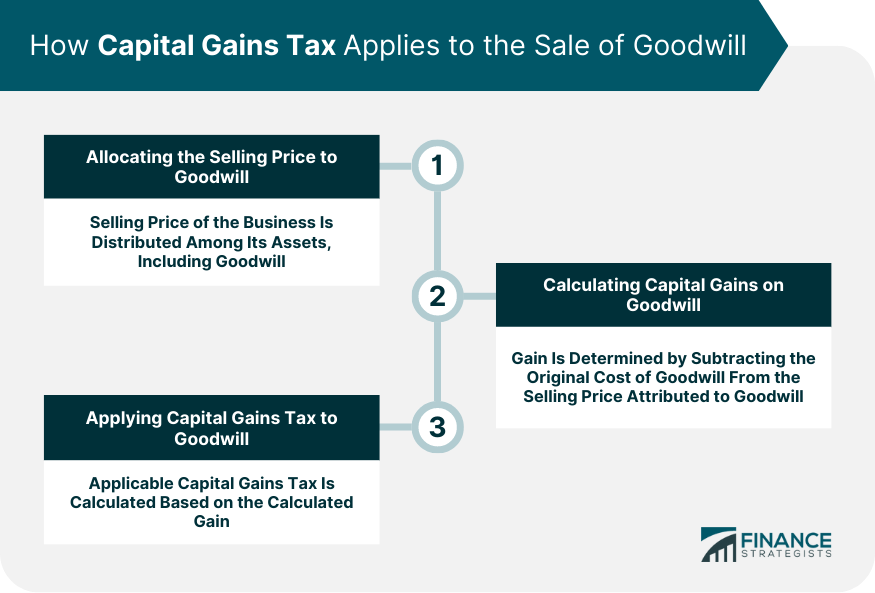

How Capital Gains Tax Applies to the Sale of Goodwill

Allocating the Selling Price to Goodwill

Calculating the Capital Gains on Goodwill

Applying the Capital Gains Tax to Goodwill

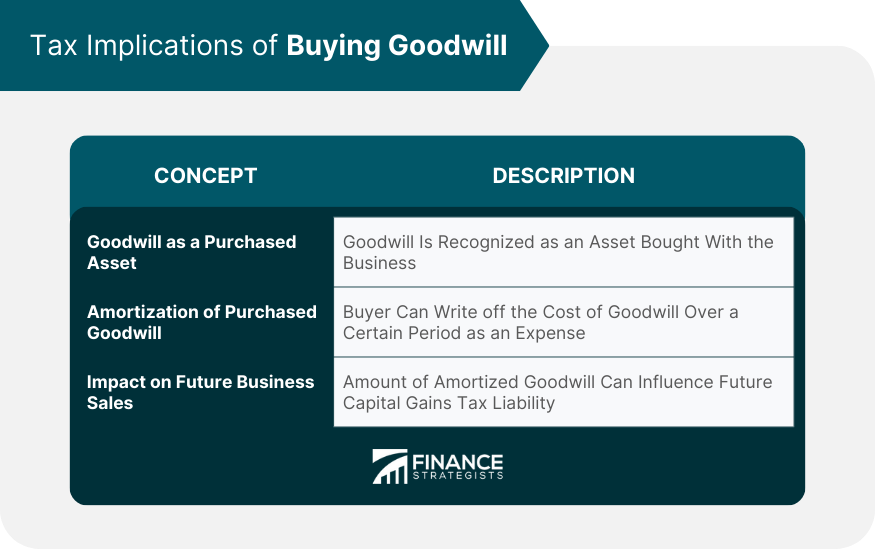

Tax Implications of Buying Goodwill

Goodwill as a Purchased Asset

Amortization of Purchased Goodwill

Impact on Future Sales of the Business

Changes in Tax Laws

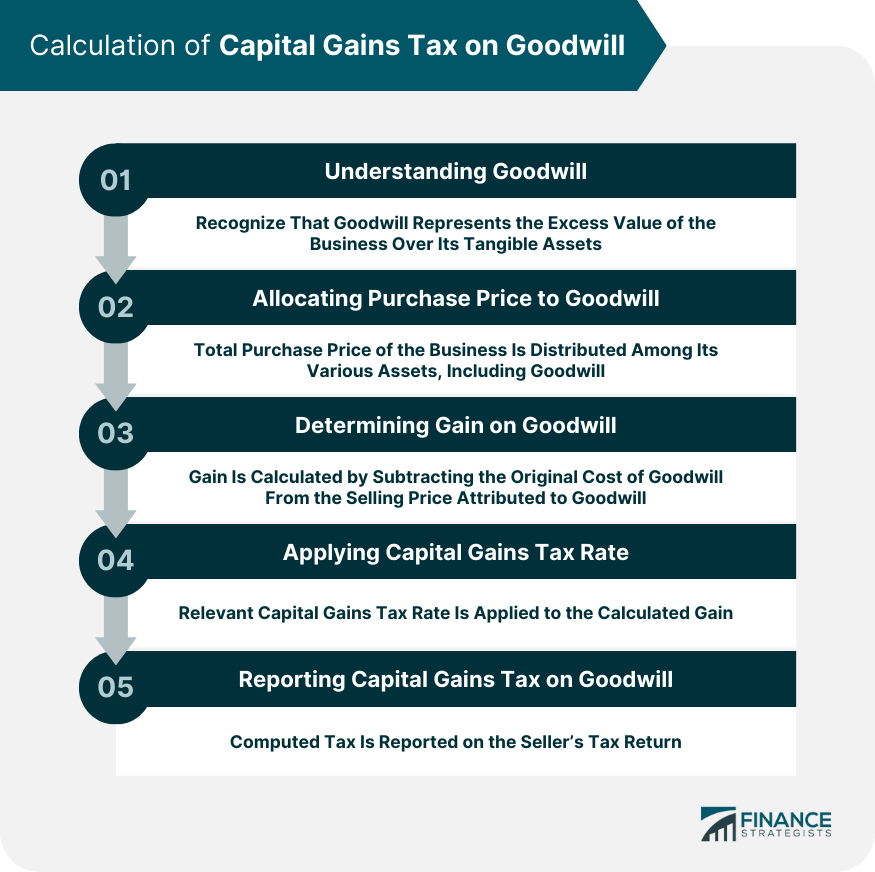

Calculation of Capital Gains Tax on Goodwill

Understanding Goodwill

Allocating Purchase Price to Goodwill

Determining the Gain on Goodwill

Applying the Capital Gains Tax Rate

Reporting the Capital Gains Tax on Goodwill

Impact of Capital Gains Tax on Goodwill in Mergers and Acquisitions

Role of Goodwill in M&A Transactions

Tax Implications for Sellers in M&A Transactions

Tax Implications for Buyers in M&A Transactions

Tax Strategies for Goodwill

Utilizing Installment Sales

Structuring the Transactions as Asset Sales vs Stock Sales

Using Section 1031 Exchanges for Deferring Capital Gains Tax on Goodwill

Legal and Regulatory Considerations of Capital Gains Tax on Goodwill

IRS Rules and Regulations regarding Goodwill and Capital Gains Tax

Recent Legal Cases and Precedents of Capital Gains Tax on Goodwill

Impact of Tax Law Changes on Capital Gains Tax on Goodwill

Conclusion

Capital Gains Tax on Goodwill FAQs

Capital gains tax on goodwill refers to the tax levied on the gain realized from the sale of a business's goodwill. Goodwill is an intangible asset that often makes up a significant portion of a business's value. The gain is calculated as the selling price of the goodwill less its original cost, and the tax is based on this gain.

The capital gains tax on goodwill is calculated in several steps. First, the total selling price of the business is allocated among its various assets, including goodwill. Then, the original cost of the goodwill is subtracted from the allocated selling price to determine the gain. The capital gains tax is then calculated based on this gain and the applicable tax rate.

For sellers, the amount of the sale price attributed to goodwill is subject to capital gains tax. The tax rate will depend on whether the goodwill is considered a short-term or long-term asset. For buyers, they can often treat purchased goodwill as a depreciable asset, reducing their taxable income over time.

Businesses can manage capital gains tax on goodwill effectively by utilizing tax strategies such as installment sales, structuring transactions as asset or stock sales, and potentially using Section 1031 exchanges for deferring capital gains tax. Furthermore, consultation with tax professionals can provide valuable insights and strategies tailored to the specific situation of the business.

Changes in tax laws can significantly impact the capital gains tax on goodwill. For instance, changes in tax rates, holding period requirements, or the definition of goodwill can alter the tax implications of selling or buying a business. Businesses must keep track of potential tax law changes and adapt their strategies accordingly.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.