Group life insurance is a type of life insurance coverage offered by employers or other organizations to their employees or members as part of a benefits package. This type of insurance provides financial protection to beneficiaries in the event of the insured individual's death. Group life insurance serves to provide financial security for the insured's dependents in case of their passing. It offers several benefits, including lower premiums due to risk pooling, simplified underwriting, and easy access to coverage for employees or members. Key features of group life insurance include a master policy held by the employer or organization, coverage based on a multiple of the employee's salary or a fixed amount, and automatic enrollment for eligible employees or members. Coverage may also include options for additional voluntary coverage and coverage for dependents. Term life insurance provides coverage for a specified period, usually ranging from one to 30 years. Group term life insurance is the most common type of group life insurance offered by employers, providing affordable coverage with no cash value accumulation. Whole life insurance offers permanent coverage with level premiums and a cash value component. While less common as a group life insurance option, some employers may offer group whole life insurance policies that combine the advantages of group coverage with the benefits of permanent life insurance. Universal life insurance is a type of permanent life insurance with flexible premiums and a cash value component that can grow over time. Although rare in group life insurance offerings, some employers may provide group universal life insurance as an option for employees seeking greater flexibility and investment opportunities. Eligibility for group life insurance typically requires an individual to be an employee or member of the sponsoring organization. Additional criteria may include minimum hours worked per week, length of employment, or membership, and participation in other benefit programs. The enrollment process for group life insurance is generally straightforward, with most eligible employees or members being automatically enrolled. Employees may need to complete an enrollment form, designate beneficiaries, and choose coverage options during an open enrollment period or when first becoming eligible. Coverage for group life insurance usually begins on the effective date specified by the employer or organization. This date may coincide with the employee's hire date, the start of the plan year, or another predetermined date. Premiums for group life insurance are typically based on factors such as the group's demographics, coverage amounts, and the insurer's underwriting guidelines. Group rates are often lower than individual rates due to the risk pooling and economies of scale. Employers may choose to fully or partially subsidize group life insurance premiums, with employees contributing the remaining cost. Employee contributions are usually made through payroll deductions, making the process convenient and seamless. Factors that can impact group life insurance premiums include the group's age distribution, gender makeup, and overall health status. Additionally, the coverage amounts, optional riders, and the financial strength of the insurance provider can also influence premium rates. Basic life insurance coverage typically provides a fixed benefit amount or a multiple of the employee's annual salary. This base coverage is generally provided at no cost or a minimal cost to the employee and serves as a foundation for financial protection. Some group life insurance plans offer optional additional coverage that employees can purchase to supplement their basic coverage. This voluntary coverage allows employees to tailor their life insurance benefits to better suit their individual needs and circumstances. Dependent coverage is an optional feature of group life insurance plans that allows employees to extend coverage to their spouse, domestic partner, or children. This coverage provides financial protection for the employee's dependents in the event of their passing. Accidental death and dismemberment (AD&D) coverage is an optional rider that provides additional benefits in the event of an accidental death or specific injuries resulting from an accident. This coverage can provide added financial protection for employees and their families in case of unforeseen accidents. The tax treatment of group life insurance premiums and benefits may vary depending on factors such as the employer's contributions, the amount of coverage, and local tax laws. Generally, employer-paid premiums for basic coverage are tax-deductible for the employer and not considered taxable income for the employee. However, benefits received by beneficiaries are typically tax-free. Group life insurance is subject to various legal and regulatory requirements, such as state insurance regulations, federal laws, and ERISA guidelines. Employers and insurers must comply with these requirements to ensure the proper administration and management of group life insurance plans. Employers and insurers are required to provide clear and accurate information about group life insurance coverage to employees and plan participants. This may include plan documents, summary plan descriptions, and any required notices or disclosures related to eligibility, enrollment, and coverage details. One of the main advantages of group life insurance is that it offers lower premium rates compared to individual life insurance policies. This is because insurers spread the risk across a large group of individuals, allowing them to offer more affordable coverage. As a result, employees can obtain life insurance coverage at a lower cost than they would typically find in the individual market. Another advantage of group life insurance is that it often involves simplified underwriting processes, which means employees can obtain coverage without undergoing extensive medical underwriting. This is particularly beneficial for employees with pre-existing medical conditions who might otherwise struggle to secure affordable life insurance coverage. In many cases, employees may not even be required to provide any medical information to obtain coverage. Group life insurance provides easy access to coverage for employees, as it is usually offered as part of a benefits package. Employees can simply enroll in the plan during the designated enrollment period, often without needing to complete any lengthy applications or provide medical information. This streamlined process makes obtaining life insurance coverage more convenient and accessible for employees. Offering group life insurance as part of a comprehensive benefits package can help employers attract and retain top talent. Employees value the financial protection that life insurance provides for themselves and their families, making it an appealing benefit. By offering group life insurance, employers demonstrate their commitment to employee well-being and financial security, which can positively impact employee satisfaction and loyalty. One disadvantage of group life insurance is that it often provides limited customization options for employees. Unlike individual life insurance policies, which can be tailored to suit an individual's specific needs and preferences, group life insurance typically offers a standard level of coverage with few optional features. As a result, employees may find that the coverage provided by their group life insurance plan does not fully meet their unique financial protection requirements. Another downside of group life insurance is that employees may lose their coverage when they leave their employer. This can be a significant concern for individuals who rely on their group life insurance as their primary source of financial protection. While some plans offer conversion options that allow employees to transition their coverage to an individual policy upon leaving their job, this process can be costly and may result in higher premiums. Group life insurance can have tax implications for high-income employees or those with large coverage amounts. Employer-paid premiums for group life insurance coverage above a certain threshold are generally considered taxable income for the employee, which can result in an increased tax liability. Employees should consult with a tax professional to determine how their group life insurance coverage may impact their taxes. Finally, employees participating in a group life insurance plan may be limited in their choice of insurers and policy features due to the nature of the group coverage. Employers typically select a single insurance provider for their group life insurance plan, and employees may not have the option to choose a different insurer or select alternative policy features. This lack of choice can be a disadvantage for employees who have specific preferences or needs that are not met by their employer's chosen plan. Group life insurance and individual life insurance differ in several ways, including cost, coverage options, and policy features. While group life insurance is generally more affordable, it may provide limited coverage options and features compared to individual policies, which can be tailored to meet specific needs and preferences. When deciding between group and individual life insurance policies, employees should consider factors such as their financial needs, coverage options, cost, and portability of coverage. It may be beneficial for some individuals to maintain both group and individual policies to ensure adequate financial protection for their families. Group life insurance plays a vital role in providing financial security for employees and their families. As a component of a comprehensive benefits package, group life insurance can help attract and retain top talent while offering valuable protection to employees. Employers and employees should carefully evaluate group life insurance options, taking into consideration factors such as coverage amounts, optional riders, and cost-sharing arrangements. This evaluation will help ensure that group life insurance plans provide the necessary financial protection and align with the needs and preferences of employees. Both employers and employees must balance the costs and coverage of group life insurance plans to ensure optimal benefits and protection. By considering factors such as premiums, coverage options, and tax implications, employers and employees can make informed decisions about group life insurance and create a supportive benefits package that meets the diverse needs of the workforce. Group life insurance should be considered as a component of an individual's overall financial planning strategy. While it provides essential protection for employees and their families, it's important to evaluate how it complements other life insurance policies, retirement savings, and investments to ensure comprehensive financial security.What Is Group Life Insurance?

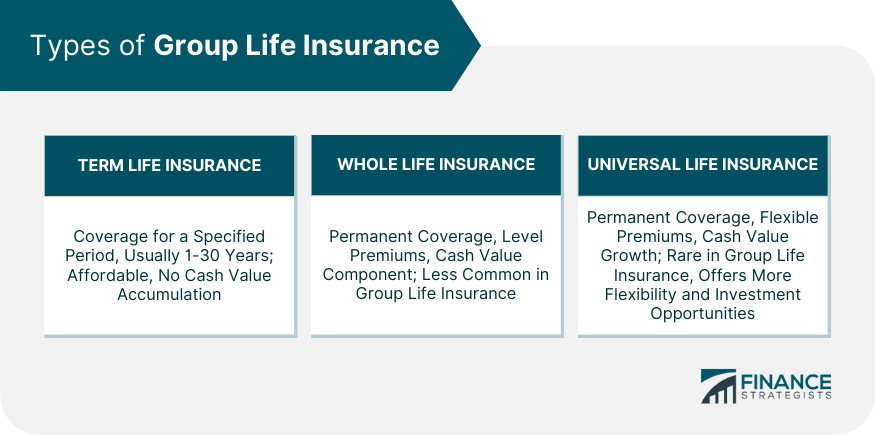

Types of Group Life Insurance

Term Life Insurance

Whole Life Insurance

Universal Life Insurance

Eligibility and Enrollment of Group Life Insurance

Eligibility Criteria

Enrollment Process

Coverage Commencement

Premiums and Cost Sharing of Group Life Insurance

Premium Calculation

Employer and Employee Contributions

Factors Affecting Premiums

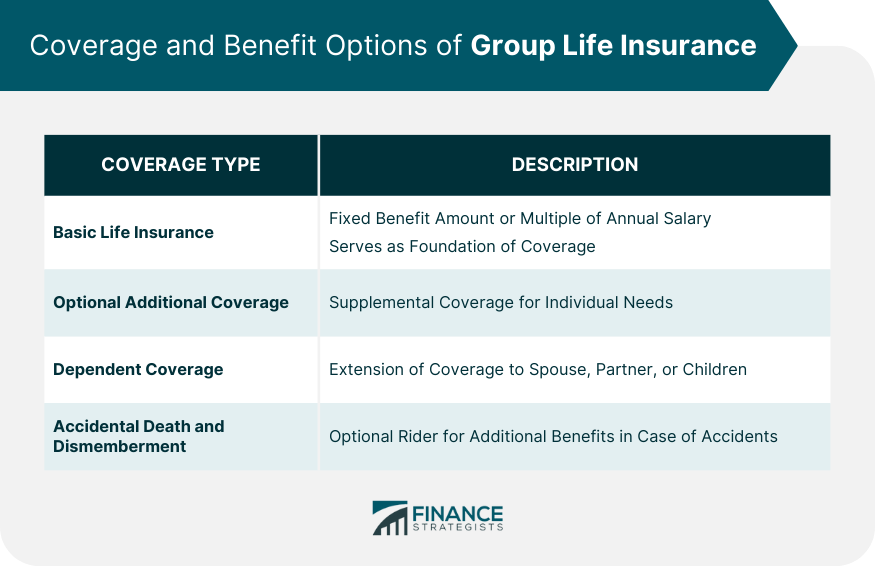

Coverage and Benefit Options of Group Life Insurance

Basic Life Insurance Coverage

Optional Additional Coverage

Dependent Coverage

Accidental Death and Dismemberment (AD&D) Coverage

Legal and Regulatory Requirements

Tax Treatment of Premiums and Benefits

Legal and Regulatory Framework

Disclosure Requirements

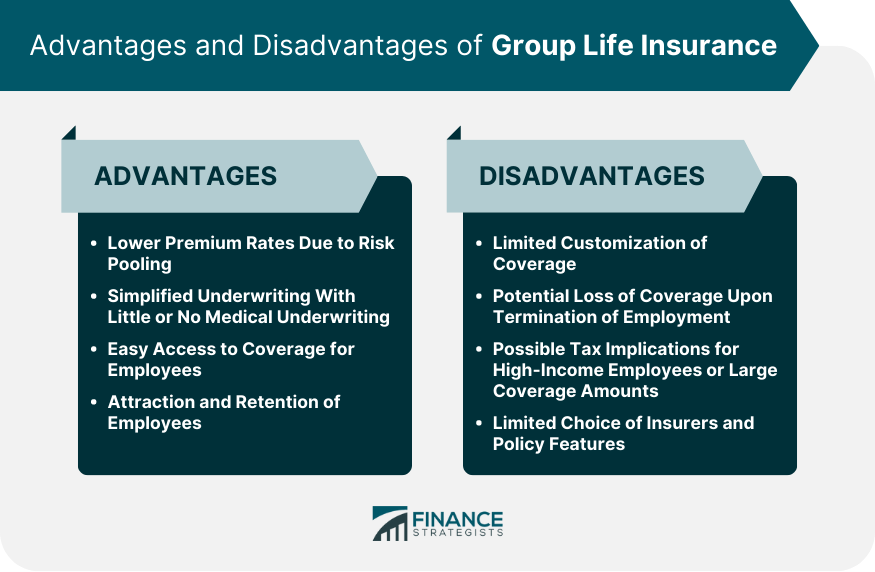

Advantages of Group Life Insurance

Lower Premium Rates Due to Risk Pooling

Simplified Underwriting With Little or No Medical Underwriting

Easy Access to Coverage for Employees

Attraction and Retention of Employees

Disadvantages of Group Life Insurance

Limited Customization of Coverage

Potential Loss of Coverage Upon Termination of Employment

Possible Tax Implications for High-Income Employees or Large Coverage Amounts

Limited Choice of Insurers and Policy Features

Comparing Group Life Insurance With Individual Life Insurance

Differences in Cost, Coverage, and Features

Factors to Consider When Choosing Between Group and Individual Policies

Final Thoughts

Group Life Insurance FAQs

Many group life insurance policies offer a conversion feature that allows employees to convert their coverage to an individual policy upon leaving their employer. This conversion typically does not require a medical exam but may result in higher premiums due to the loss of group discounts.

Employees may have the option to increase their group life insurance coverage by purchasing additional voluntary coverage or by participating in optional programs such as dependent coverage or AD&D coverage. However, the availability of increased coverage and the limits on additional coverage will depend on the specific group life insurance plan.

When enrolling in a group life insurance plan, employees will be asked to designate a beneficiary or beneficiaries who will receive the death benefit in the event of their passing. Beneficiaries can be individuals, trusts, or organizations, and employees should carefully consider their choice to ensure their wishes are accurately reflected.

If an employer changes group life insurance providers, employees may be automatically enrolled in the new provider's plan. However, employees should review the new plan's coverage options, premiums, and features to ensure they understand any changes to their coverage and benefits.

Group life insurance benefits are generally not considered taxable income for the beneficiary. However, there may be tax implications for employees if their coverage exceeds certain limits or if the employer pays a portion of the premiums for additional voluntary coverage. Employees should consult a tax professional to determine their specific tax situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.