Underwriting capacity, in the context of insurance, refers to the maximum amount of risk that an insurance company is willing and able to underwrite or assume. This limit is established based on the company's financial resources, regulatory constraints, and risk appetite. The concept of underwriting capacity is crucial in understanding the ability of an insurer to accept new business, manage risk, and generate profits. Underwriting capacity serves as the foundation for operations in the insurance industry. It dictates the amount of risk an insurer can accept from policyholders and directly influences its revenue through premiums. Without adequate underwriting capacity, insurers cannot fulfill their risk-bearing function effectively, potentially leading to insolvency. Moreover, underwriting capacity represents an insurer's competitiveness in the market. With greater capacity, an insurer can write more policies, attract a broader customer base, and diversify its risk. The amount of available capital is a fundamental determinant of an insurer's underwriting capacity. More capital allows an insurer to accept more risk. However, capital isn't unlimited; insurers need to maintain sufficient reserves to cover potential claims, meet regulatory requirements, and ensure business continuity. Therefore, they must carefully manage their capital to optimize their underwriting capacity. Regulatory bodies impose rules and restrictions on the amount of risk that insurers can undertake relative to their capital and reserves. These requirements aim to safeguard policyholders and ensure the solvency of insurers. Consequently, insurers need to factor regulatory requirements into their underwriting capacity calculations. Market conditions significantly affect underwriting capacity. For instance, during periods of high demand for insurance coverage, insurers may choose to increase their underwriting capacity to capitalize on the favorable market. Conversely, in times of economic downturns or increased risk, insurers might restrict their underwriting capacity to maintain financial stability. Reinsurance, which is insurance for insurers, plays a vital role in determining underwriting capacity. By transferring a portion of their risks to reinsurers, insurance companies can increase their underwriting capacity, underwrite more policies, and spread their risks. However, the availability and cost of reinsurance depend on market conditions, which in turn influence the underwriting capacity of insurers. Gross underwriting capacity refers to the total amount of risk an insurer can assume before considering reinsurance. It is typically calculated based on the insurer's capital and reserves, and the riskiness of the policies it underwrites. To determine gross underwriting capacity, insurers analyze their financial statements, risk models, and business plans. Net underwriting capacity, on the other hand, takes into account the effect of reinsurance. When insurers cede risk to reinsurers, they free up part of their underwriting capacity, allowing them to underwrite more policies. Thus, net underwriting capacity is usually higher than gross underwriting capacity. The extent to which reinsurance affects underwriting capacity depends on the type and terms of the reinsurance agreement. For instance, a quota share reinsurance agreement, in which the reinsurer assumes a fixed percentage of every policy written, directly increases the insurer's underwriting capacity. On the other hand, an excess of the loss reinsurance agreement, which only comes into play for exceptionally large claims, might not significantly increase underwriting capacity. Insurers also need to adjust their underwriting capacity based on market conditions. For instance, during a hard market characterized by high premium rates and limited coverage availability, insurers may choose to increase their underwriting capacity to maximize their profits. Conversely, during a soft market with lower premiums and broader coverage, insurers might decrease their underwriting capacity to limit their exposure to risk. These adjustments require careful market analysis and strategic decision-making. The underwriting capacity of an insurer heavily influences its pricing strategy. Insurers with larger underwriting capacities can accept more risks, enabling them to offer competitive prices and increase their market share. Conversely, those with smaller capacities may have to charge higher premiums to compensate for the limited volume of risks they can accept. Furthermore, insurers might adjust their pricing based on the types of risks they are willing to assume. If an insurer's underwriting capacity is large enough to accommodate higher-risk policies, it may charge higher premiums to offset the potential claims. Underwriting capacity directly impacts policy premiums. Higher underwriting capacity means an insurer can underwrite more policies and spread its risks more widely, potentially allowing for lower premium rates. On the other hand, limited underwriting capacity may lead to higher premiums as the insurer needs to earn enough from a smaller number of policies to cover potential claims and operational costs. When underwriting capacity is constrained, either by lack of capital, regulatory restrictions, or high reinsurance costs, insurers are forced to be selective in the risks they accept. In such scenarios, insurers might increase premium rates to cover the heightened risk concentration in their portfolio. This could result in higher prices for policyholders, especially for those presenting higher risk profiles. Reinsurance plays a critical role in expanding an insurer's underwriting capacity. By ceding part of their risks to reinsurers, insurers can reduce their potential liabilities and free up capital, allowing them to underwrite more policies. This is especially important for insurers operating in high-risk segments or catastrophic lines of business, where a single event could generate massive losses. Different types of reinsurance agreements have different impacts on underwriting capacity. Proportional reinsurance agreements, such as quota share and surplus share, provide a direct increase in underwriting capacity as a proportion of each risk is passed to the reinsurer. Non-proportional reinsurance, like excess of loss agreements, protects the insurer against extreme losses. While these agreements don't directly increase underwriting capacity, they enhance the insurer's financial stability, indirectly supporting a higher capacity. Reinsurance brings both benefits and risks. On the positive side, it allows insurers to underwrite more business, diversify their risk, and stabilize their financial results. However, it also introduces the risk of dependency on reinsurers. If a reinsurer fails to meet its obligations, the insurer may face financial strain. Insurers also bear the risk of rising reinsurance costs, which could reduce their underwriting capacity. In life insurance, underwriting capacity is influenced by the insurer's financial strength, longevity risks, and the nature of the policies offered. The long-term nature of these policies requires a careful assessment of the insurer's capacity to meet future liabilities. Actuarial science, which involves statistical analysis of life expectancy and morbidity rates, plays a crucial role in determining this capacity. In health insurance, underwriting capacity depends on a range of factors, including the insurer's capital, the health profiles of potential policyholders, and the cost of healthcare. Health insurers often need to manage their underwriting capacity carefully, especially given the unpredictability of healthcare costs and regulatory changes in many jurisdictions. Underwriting capacity in property and casualty (P&C) insurance is largely influenced by the insurer's capital, the nature of the risks insured, and the level of reinsurance. Given the potential for significant losses from a single event, like a natural disaster, P&C insurers often rely heavily on reinsurance to manage their underwriting capacity. Specialty insurance covers unique or high-risk areas not typically covered by standard insurance policies. Given the higher risks involved, underwriting capacity in this segment is often more limited. Insurers need to assess the unique risks associated with each specialty line and adjust their underwriting capacity accordingly. Risk diversification is a key strategy for managing underwriting capacity. By spreading risks across various types of policies, geographical locations, and customer segments, insurers can mitigate the potential impact of a single adverse event. A diversified risk portfolio can help maintain a stable underwriting capacity and reduce the likelihood of large-scale losses. Catastrophe modeling plays a vital role in managing underwriting capacity, particularly in property and casualty insurance. These sophisticated mathematical models simulate the potential financial losses from catastrophic events such as earthquakes, hurricanes, or floods. By understanding potential exposures through catastrophe modeling, insurers can set appropriate underwriting capacity levels for certain risks, adjust their reinsurance purchase, and strategically price their policies. This ensures they maintain adequate financial resources to cover potential catastrophic losses. There are various techniques insurers use to manage risks to their underwriting capacity. They may adjust premium rates based on the perceived risk levels of policyholders. They can also limit coverage for high-risk areas or categories, reducing their potential exposure. Purchasing reinsurance is another common strategy. Through a sound risk management approach, insurers can maintain a healthy underwriting capacity while protecting their financial stability. Underwriting capacity is integral to the functioning of insurance companies, dictating the amount of risk they can shoulder. Determined by factors such as available capital, regulatory requirements, market conditions, and reinsurance availability, it directly impacts an insurer's operations and market competitiveness. Calculation methods include gross underwriting capacity, net underwriting capacity, and adjustments for reinsurance and market conditions. Its influence on insurance pricing is substantial, with larger underwriting capacities enabling more competitive prices. Reinsurance can be an effective tool for expanding underwriting capacity, although it introduces dependencies. Different insurance types, including life, health, casualty, and specialty insurance, each have unique considerations regarding underwriting capacity. Ultimately, successful risk management, encompassing risk diversification and catastrophe modeling, is vital to maintaining a healthy underwriting capacity, promoting financial stability, and enabling insurers to fulfill their risk-bearing role effectively.What Is Underwriting Capacity?

Factors Influencing Underwriting Capacity

Available Capital

Regulatory Requirements

Market Conditions

Reinsurance Availability

Methods of Calculating Underwriting Capacity

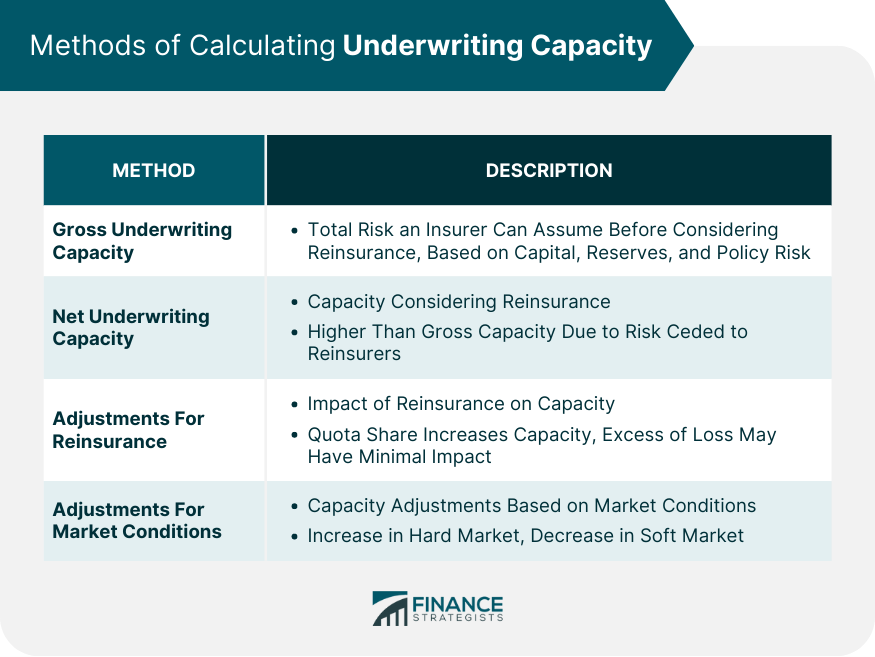

Gross Underwriting Capacity Calculation

Net Underwriting Capacity Calculation

Adjustments for Reinsurance

Adjustments for Market Conditions

Underwriting Capacity and Insurance Pricing

Pricing Strategy Based on Underwriting Capacity

Impact of Underwriting Capacity on Policy Premiums

Capacity Constraints and Their Effects on Insurance Pricing

Reinsurance and Underwriting Capacity

Role of Reinsurance in Increasing Underwriting Capacity

Types of Reinsurance Agreements Impacting Underwriting Capacity

Risks and Benefits of Using Reinsurance to Increase Underwriting Capacity

Underwriting Capacity in Various Types of Insurance

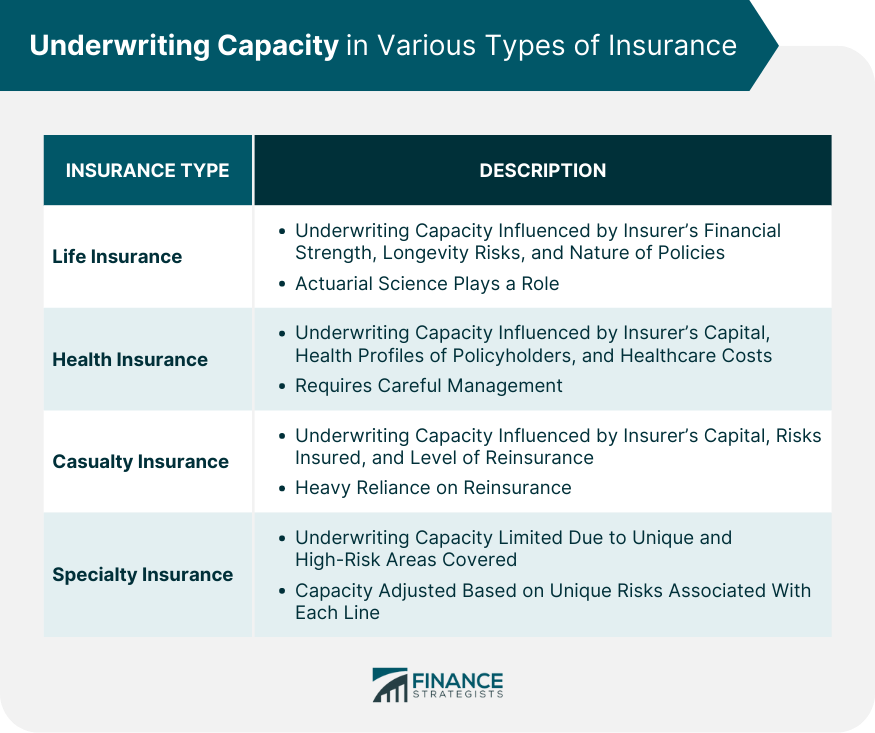

Life Insurance

Health Insurance

Casualty Insurance

Specialty Insurance

Risk Management and Underwriting Capacity

Risk Diversification and Its Impact on Underwriting Capacity

Role of Catastrophe Modeling in Managing Underwriting Capacity

Techniques for Managing Risks to Underwriting Capacity

Final Thoughts

Underwriting Capacity FAQs

Underwriting capacity is the maximum amount of risk that an insurance company can accept or underwrite. It's based on the insurer's financial resources, regulatory constraints, and risk appetite.

Reinsurance allows insurers to pass on a portion of their risk to another insurer, effectively increasing their underwriting capacity. It allows insurers to write more policies and diversify their risk.

Factors that influence underwriting capacity include available capital, regulatory requirements, market conditions, and the availability and cost of reinsurance.

Risk management is crucial in underwriting capacity because it allows insurers to balance the need to generate revenue with the need to avoid levels of risk that could threaten their financial stability.

Underwriting capacity has a direct impact on insurance pricing. Insurers with larger underwriting capacities can accept more risks, allowing them to offer competitive prices. Limited underwriting capacity may lead to higher premiums as insurers need to compensate for the smaller number of policies they can underwrite.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.