The waiver of premium for payer benefit is a type of insurance rider that ensures the continuation of the policy even if the policyholder, due to a severe illness or injury, becomes unable to pay the premiums. The policyholder's incapacity could stem from a debilitating accident, a severe illness, or any medical condition that incapacitates them from carrying out regular duties and, by extension, their capacity to earn and pay the premiums. The waiver of premium for payer benefit in a life insurance policy plays a crucial role in securing the insured's financial stability. It ensures the continuation of life insurance coverage without premium payments during a period of significant hardship when the policyholder is unable to earn an income. Without this rider, the inability to pay premiums could lead to the policy lapse, leaving the policyholder and their beneficiaries without the safety net that life insurance provides. The conditions that trigger the waiver of premium for payer benefit vary depending on the specifics of the policy. Typically, this rider activates when the policyholder becomes totally disabled and is unable to work. The definition of "total disability" differs among insurers, but it often requires the policyholder to be entirely incapable of working in their regular occupation or any occupation for which they are qualified. Some policies might necessitate a waiting period of six months of total disability before the waiver is in effect. To invoke the waiver of premium for payer benefit, the policyholder usually has to submit proof of their disability to the insurer. The insurance company may require medical documentation, proof of job loss due to disability, or other relevant records. Once the insurer verifies the total disability, they will suspend the requirement for premium payments for as long as the policyholder remains disabled, according to the terms of the policy. While the waiver of premium for payer benefit can provide valuable financial protection, there are often limitations and exclusions. For example, insurers typically impose an age limit, after which the rider can no longer be activated. Additionally, certain types of disabilities might not be covered, and exclusions may apply for disabilities resulting from specific activities or conditions, such as war, participation in dangerous hobbies, or pre-existing conditions. The cost of adding a waiver of premium for payer benefit to an insurance policy is usually expressed as a small percentage increase to the policy's base premium. The specific cost can depend on factors like the policyholder's age, health status, occupation, and the policy's face amount. Though it represents an additional expense, the potential benefits it brings can significantly outweigh the cost, particularly in unforeseen circumstances that lead to disability. The waiver of premium for payer benefit generally results in a higher policy premium compared to a similar policy without the rider. However, in the event of the policyholder's disability, the effect is dramatically reversed. Under the waiver, no further premiums are required, thus preserving the policyholder's cash flow during a financially challenging period. The economic value of a waiver of premium for payer benefit is best understood through various scenarios. For a young, healthy individual, the probability of becoming disabled might seem low, making the rider's cost appear unnecessary. However, the financial impact of losing income due to disability can be significant, making the rider a worthwhile investment. For someone middle-aged with dependents, the economic value of this benefit becomes even more apparent. If they become disabled, the waiver ensures that their life insurance policy remains in force, providing continued financial protection for their dependents. For individuals nearing retirement, the value of the rider might decrease due to the reduced term of the policy and the proximity to the rider's age limit. However, if they have significant responsibilities or debts, maintaining the rider could still be valuable to ensure the continued validity of their life insurance coverage. While both the waiver of premium for payer benefit and the disability income rider provides benefits in the event of a disability, they serve different purposes. The waiver of premium for payer benefit ensures that your life insurance policy stays in force without the need for further premium payments. On the other hand, a disability income rider provides a monthly income to the policyholder if they become disabled and can no longer work. In other words, the waiver of premium for payer benefit maintains the existing death benefit and any other policy benefits for the beneficiaries, while the disability income rider provides direct financial support to the policyholder. The waiver of premium for payer benefit is often compared with the critical illness rider, another common insurance policy add-on. While both riders waive premium payments under certain conditions, the critical illness rider typically comes into play when the policyholder is diagnosed with a critical illness as defined by the policy. It may pay out a lump sum that can be used at the policyholder's discretion, possibly even to pay the insurance premiums. However, the critical illness rider usually doesn't require the policyholder to be totally disabled. The main advantage of choosing a waiver of premium for payer benefit is that it ensures your life insurance policy remains active even if you can't pay the premiums due to disability. This provides peace of mind and financial security for your beneficiaries. However, it does not offer direct financial assistance to the policyholder during their disability. In contrast, riders like the disability income rider or critical illness rider can provide direct financial support to the policyholder, helping to cover daily living expenses or medical costs. However, these riders usually don't keep the insurance policy active if the policyholder can't continue paying the premiums. The legal provisions concerning the waiver of premium for payer benefit differ across jurisdictions. However, it is standard for insurance contracts to include clauses specifying the conditions under which the rider can be invoked, the proof required, and the implications for the policy and premiums. It is crucial for policyholders to understand these provisions when purchasing the rider. Insurance regulators oversee the provision of the waiver of premiums for payer benefits. They set the standards for transparency, documentation, and the resolution of claims disputes. Insurance companies must comply with these regulations to offer this rider. Regulatory oversight aims to protect policyholders and ensure fair treatment. Consumers have several rights and protections concerning the waiver of premiums for payer benefits. They have the right to receive clear and comprehensive information about the rider, including its cost, benefits, and exclusions. In the case of a dispute, policyholders have the right to a fair hearing and appeal process. Before purchasing the rider, understand its terms and conditions, including the definitions of disability, the waiting period, and any exclusions. This understanding helps to manage expectations and prepare for potential scenarios. If you become disabled and need to invoke the rider, ensure you keep thorough medical records and any other documentation required by your insurer. This practice will aid the smooth processing of your claim. Regularly review your insurance policy and the attached riders, including the waiver of premium for payer benefit. As your financial situation and health status change, you might need to adjust your insurance coverage. Consider seeking advice from a financial advisor or insurance professional. They can provide personalized advice based on your situation, helping you make informed decisions about your life insurance coverage and the appropriateness of various riders, including the waiver of premium for payer benefit. The waiver of premium for payer benefit is an insurance rider that ensures your life insurance policy remains active, even if you're unable to continue premium payments due to disability. It works by stepping in when a policyholder's capacity to work and earn is compromised by a severe illness or injury, thereby waiving the need for further premium payments. The financial implications of this rider include an increased initial policy premium; however, its value becomes overwhelmingly apparent when faced with a disabling condition that prevents income generation. As this rider could significantly impact your financial security and that of your dependents, it's vital to understand its terms and conditions. Insurance choices are deeply personal and situation-dependent, making it crucial to seek advice tailored to your circumstances. Reach out to a trusted insurance broker who can guide you through the complexities of life insurance and the waiver of premiums for payer benefits.What Is a Waiver of Premium for Payer Benefit?

How the Waiver of Premium for Payer Benefit Works

Conditions That Trigger the Waiver of Premium for Payer Benefit

Process of Invoking the Waiver of Premium for Payer Benefit

Limitations and Exclusions

Financial Implications of a Waiver of Premium for Payer Benefit

Cost of Adding to an Insurance Policy

Impact on Policy Premiums

Economic Value of a Waiver of Premium for Payer Benefit in Various Scenarios

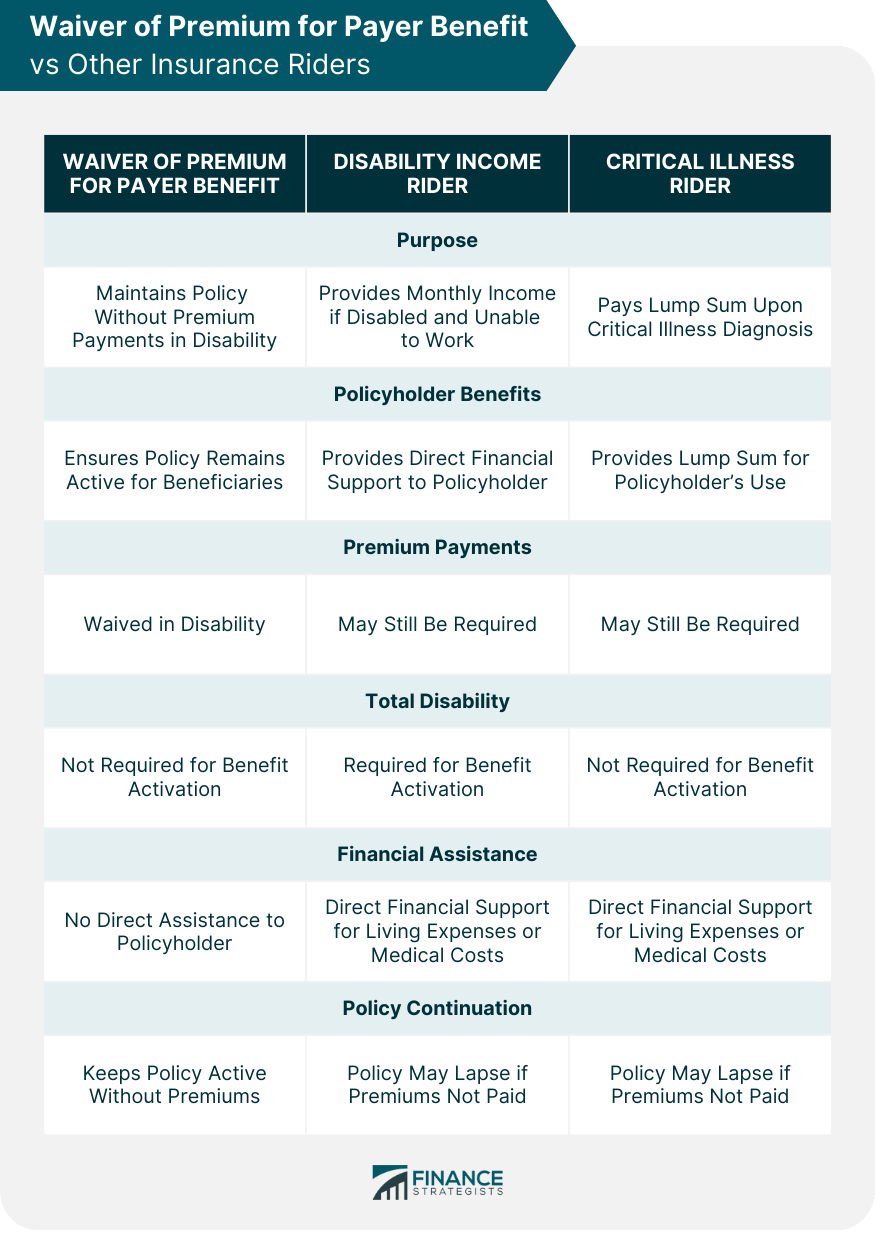

Comparison Between Waivers of Premium for Payer Benefit and Other Insurance Riders

Disability Income Rider

Critical Illness Rider

Pros and Cons vs Other Riders

Legal and Regulatory Aspects of Waivers of Premium for Payer Benefit

Legal Provisions

Regulatory Oversight and Compliance

Consumer Rights and Protections

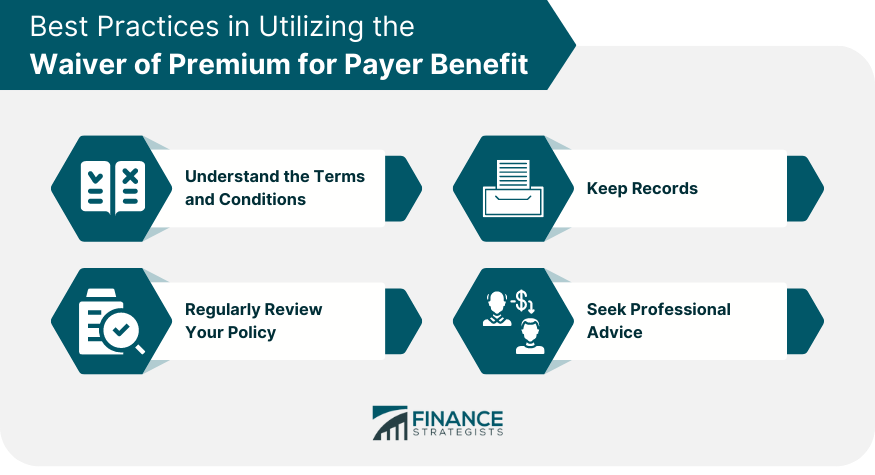

Best Practices in Utilizing the Waiver of Premium for Payer Benefit

Understand the Terms and Conditions

Keep Records

Regularly Review Your Policy

Seek Professional Advice

Final Thoughts

Waiver of Premium for Payer Benefit FAQs

The waiver of premium for payer benefit is an insurance rider that maintains your life insurance coverage without requiring further premium payments if you become disabled.

If the policyholder becomes disabled and cannot work, this rider waives the need for further premium payments, ensuring that the life insurance policy remains active.

Although adding this rider results in a slightly higher policy premium, it provides financial security by maintaining your insurance coverage without further premium payments in the event of a disability.

There are limitations and exclusions, such as certain types of disabilities not being covered and an age limit for invoking the benefit.

The waiver of premium for payer benefit is typically offered as an optional rider by most life insurance providers.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.