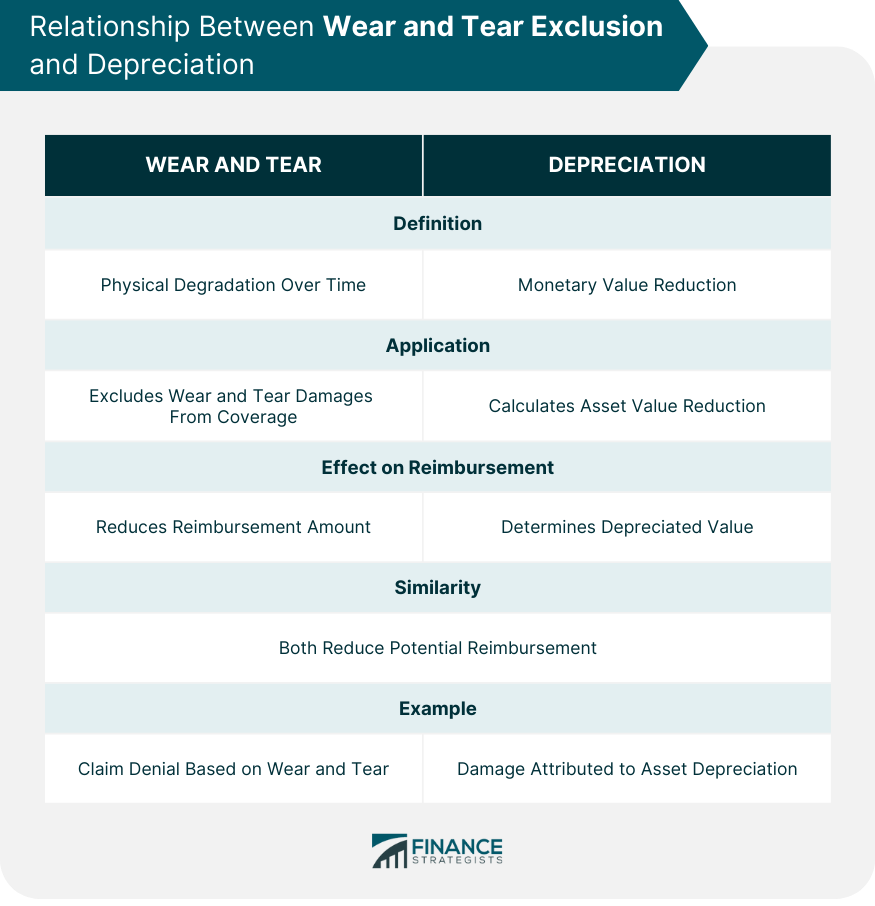

Wear and Tear Exclusion refers to a common provision in insurance policies that excludes coverage for damage caused to assets, property, or equipment due to normal use over time. This exclusion underlines the principle that insurance is not meant to cover predictable, gradual degradation but rather unforeseen, sudden, and accidental incidents. Understanding the concept of Wear and Tear Exclusion is critical for both individuals and businesses. Policyholders must be aware of what their insurance policy covers and what it excludes. It helps them manage their risks, anticipate potential liabilities, and make informed decisions about asset management, maintenance strategies, and insurance needs. The fundamental principle behind the Wear and Tear Exclusion is that insurance is designed to protect against unexpected losses, not routine maintenance or predictable wear and tear. In other words, it’s not a maintenance contract. Therefore, if a machine in a factory breaks down because it has not been properly maintained over the years, the insurance company will likely not cover the loss. Wear and Tear Exclusion significantly impacts policyholders as it can lead to denied claims. If a loss is classified as wear and tear, the insurer won't cover it. As a result, the financial burden of replacing or repairing the damaged item falls on the policyholder. This makes it crucial for policyholders to differentiate between damage due to wear and tear and damage due to sudden, unforeseen incidents. Virtually all tangible assets, from buildings and cars to machinery and household items, are subject to Wear and Tear Exclusion. For instance, in home insurance, if your roof leaks due to years of weather exposure, that's considered wear and tear and is excluded from coverage. Similarly, in car insurance, mechanical breakdowns due to mileage accumulation would not be covered. The wording of a Wear and Tear Exclusion clause may vary, but it typically includes phrases like "We will not pay for damage caused by or resulting from wear and tear, marring, deterioration..." These terms clearly communicate the insurer's intent to exclude losses due to long-term use or neglect. While both wear and tear and depreciation relates to the diminishing value of an asset over time, they differ in their application. Wear and tear pertain to physical degradation that can lead to functional impairment. On the other hand, depreciation is an accounting concept that represents the monetary value reduction of an asset over its useful life. However, they are similar in the sense that they both reduce the potential reimbursement amount in case of a claim. For instance, an insurance company might pay only the depreciated value of an item rather than the replacement cost, particularly in cases of actual cash value (ACV) policies. Depreciation plays a key role in how insurers apply Wear and Tear Exclusion. If an asset has significantly depreciated due to prolonged use, insurers may argue that any damage is due to wear and tear rather than an insurable, sudden event. For example, if an old, heavily used HVAC system breaks down, an insurer might deny the claim on the basis of the Wear and Tear Exclusion, suggesting the system failed due to its age and prolonged use. The effect of the Wear and Tear Exclusion on claim settlements can be significant. When a claim is filed, the insurance company will conduct an investigation to determine the cause of the damage. If it's found that the damage was due to gradual deterioration over time or lack of maintenance, the claim could be denied based on the Wear and Tear Exclusion. This could lead to substantial out-of-pocket expenses for the policyholder. Consider a case where a homeowner files a claim for roof damage. The insurer's assessment determines that the damage was due to decades of weather exposure, making it a wear and tear issue. Thus, the claim is denied, leaving the homeowner to bear the cost of a new roof. Another example is in auto insurance, where an owner of an older car files a claim for an engine failure. The insurer's inspection shows that the engine failure was due to the accumulation of mileage over time. The claim gets denied under the Wear and Tear Exclusion, leaving the owner with hefty repair or replacement costs. In property insurance, the Wear and Tear Exclusion is applied to physical assets such as buildings and equipment. For instance, if a piece of machinery fails due to years of usage without proper maintenance, the claim for the repair or replacement of the machinery will be denied. Auto insurance policies usually exclude wear and tear. This means any mechanical failures due to aging, high mileage, or lack of regular maintenance are not covered. This is why routine maintenance, such as oil changes, tire replacements, and brake work, is essential for vehicle owners. In homeowners insurance, wear and tear is a common exclusion. Damages to homes resulting from aging or neglect, like roof leaks from years of weather exposure or plumbing issues from old pipes, are typically not covered. Business insurance, including property, liability, and business interruption policies, also excludes wear and tear. Equipment breakdowns or infrastructure failures resulting from a lack of regular maintenance or simply aging are usually not covered. Regular maintenance of assets can help minimize the risk of damage classified as wear and tear. Regular upkeep can extend the life of assets, preventing damages that could lead to denied claims. Keeping records of these maintenance activities can be helpful if there's a dispute about the cause of damage. Conducting regular inspections can identify potential issues before they become significant problems. Early detection of wear and tear can allow for repairs that may prevent more extensive damage in the future. Purchasing coverage that matches the risk profile and needs of your assets is also important. For example, buying replacement cost coverage instead of actual cash value coverage can ensure you get the full cost to replace an item, not just its depreciated value. Disputes often arise between insurers and policyholders over whether the damage is due to wear and tear or a covered peril. Policyholders may argue that damage was sudden and accidental, while insurers may contend it's due to gradual deterioration. Different courts have interpreted the Wear and Tear Exclusion in various ways, leading to a body of case law on the subject. For example, in some cases, courts have found in favor of policyholders when the wear and tear led to a sudden, unforeseen event. These legal decisions continue to shape the application of Wear and Tear Exclusion in insurance policies. Wear and Tear Exclusion is a key component of insurance policies, excluding coverage for damage caused to assets from normal usage over time. This exclusion has considerable implications on claim settlements and can lead to denied claims if damages are attributed to wear and tear. The exclusion is a common feature in various types of insurance, including property, auto, homeowners, and business insurance. Wear and Tear Exclusion plays a significant role in managing risks and making informed decisions about insurance coverage and asset management. Regular maintenance, timely inspections, and appropriate insurance coverage can help in mitigating risks associated with this exclusion. However, the application of Wear and Tear Exclusion often leads to disputes between insurers and policyholders due to different legal interpretations. To navigate the complexities of Wear and Tear Exclusion and other insurance matters, seeking professional guidance from an insurance broker can be beneficial.What Is Wear and Tear Exclusion?

Role of Wear and Tear Exclusion in Insurance Policies

General Principle

How It Impacts Policyholders

Specifics of Wear and Tear Exclusion

Items Typically Affected by Wear and Tear Exclusion

Typical Wording of a Wear and Tear Exclusion Clause

Relationship Between Wear and Tear Exclusion and Depreciation

Differences and Similarities

How Depreciation Affects Wear and Tear Exclusion

Impact of Wear and Tear Exclusion on the Claim Process

How Wear and Tear Exclusion Affects Claim Settlements

Case Studies Illustrating the Impact of Wear and Tear Exclusion

Wear and Tear Exclusion in Different Types of Insurance

Property Insurance

Auto Insurance

Homeowners Insurance

Business Insurance

How to Mitigate Risks Associated With Wear and Tear Exclusion

Proper Maintenance and Record-Keeping

Regular Inspections

Adequate Insurance Coverage

Controversies and Legal Issues Surrounding Wear and Tear Exclusion

Disputes Between Insurers and Policyholders

Legal Interpretations and Case Law

Final Thoughts

Wear and Tear Exclusion FAQs

Wear and Tear Exclusion refers to a common provision in insurance policies that excludes coverage for damage caused to assets due to normal use over time.

If the insurer determines that the damage to an insured item is due to wear and tear, the claim could be denied, leaving the policyholder to bear the cost of repair or replacement.

Wear and Tear Exclusion is commonly found in many types of insurance policies, including property, auto, homeowners, and business insurance.

Regular maintenance and inspections, along with adequate insurance coverage, can help mitigate the impact of Wear and Tear Exclusion.

Yes, disputes often arise between insurers and policyholders over whether the damage is due to wear and tear or a covered peril. These cases often hinge on legal interpretations and existing case law on Wear and Tear Exclusion.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.