Nonforfeiture clauses are integral components of certain types of insurance contracts. They protect policyholders by guaranteeing that certain benefits will not be lost even if they stop paying premiums. When an insurance policyholder discontinues premium payments, the policy usually lapses. However, with a nonforfeiture clause, the policyholder can retain a portion of the benefits that they've already paid for, in different forms. Nonforfeiture clauses serve as an essential safeguard for policyholders, mitigating the potential losses resulting from the discontinuation of premium payments. The main advantage is they offer a form of financial security, enabling policyholders to redeem some value from their policy, even if they can't keep up with their premiums. They, thus, enhance the overall value and appeal of an insurance policy, making it a more secure and worthwhile investment for individuals. Nonforfeiture clauses are typically found in long-term contracts, such as life insurance and annuity contracts. The purpose of these clauses is to ensure that policyholders who have been faithfully paying premiums for a significant amount of time don't lose all their benefits if they're no longer able to make payments. These clauses offer policyholders a safety net, providing options for how they can receive a portion of their accrued benefits. The specifics of how these options are determined can vary widely based on the contract's details and the type of insurance product. It's essential to note that nonforfeiture benefits typically do not equate to the total value of premiums paid into the policy. Insurers deduct certain costs, such as administrative fees and mortality charges, before determining the value of nonforfeiture benefits. It's the net amount after these deductions that are used to provide nonforfeiture options. There are several ways a policyholder can opt to receive nonforfeiture benefits, each with its own advantages and drawbacks. This is the simplest and most direct nonforfeiture option. The cash surrender value is the amount the policyholder receives in cash if they decide to terminate the policy prematurely. This amount is usually a portion of the premiums paid, minus any deductions. While this option provides immediate liquidity, it often results in the lowest overall return. Under this option, the policyholder uses the cash surrender value to purchase a fully paid-up policy. The face amount of this new policy will be less than the original policy, but it will require no further premium payments and will remain in force until the policyholder's death. This option is beneficial for those who wish to maintain insurance coverage without further financial obligation. In this case, the policyholder uses the cash surrender value to purchase term insurance for the highest face amount available for a specific period. This allows the policyholder to maintain the full death benefit for a certain period, after which the policy will lapse. This option is suitable for those seeking maximum coverage for a limited time. Some policies allow policyholders to borrow against the cash surrender value of their policies. While this does not terminate the policy, it reduces the death benefit and cash value by the amount of the loan and any accrued interest. Nonforfeiture clauses can be found in several types of insurance products, each with unique considerations. In life insurance policies, nonforfeiture clauses provide the policyholder with options for using the cash value of their policy if they can no longer pay premiums. The specific options available depend on the type of life insurance policy. Whole life policies, for instance, have a cash value that can be used for nonforfeiture benefits, while term life policies do not. In an annuity contract, a nonforfeiture clause ensures that if the annuitant discontinues premium payments, they will receive an amount at least equal to the premiums paid, minus any withdrawals or fees. This sum can either be paid out as a lump sum or used to provide a reduced annuity. Nonforfeiture benefits in long-term care insurance can take different forms. The most common is a shortened benefit period, where the policyholder receives the same daily benefit but for a shorter period. Another option is a reduced daily benefit, where the benefits are paid out for the same duration, but at a lower daily rate. Understanding the financial implications of nonforfeiture clauses can be quite complex, as these clauses interact with several facets of insurance policy economics. Policies with nonforfeiture benefits generally carries higher premiums than those without. The added cost is due to the guaranteed benefits provided, which the insurer must fund. It's crucial for policyholders to balance the potential benefits against the increased upfront costs when deciding whether to opt for a policy with nonforfeiture benefits. The tax implications of nonforfeiture benefits depend on the specific type of insurance policy and the nonforfeiture option chosen. For instance, the cash surrender value received can be taxed if it exceeds the total amount of premiums paid. Policyholders should consult with a tax professional to understand the potential tax consequences fully. Nonforfeiture options can have significant effects on the cash value of insurance policies. In general, any nonforfeiture benefits taken will reduce the cash value of the policy. However, the specific effects depend on the particular nonforfeiture option chosen. Nonforfeiture clauses also impact policy loan options. The cash surrender value of a policy, which forms the basis for nonforfeiture benefits, can also be borrowed against. If a policyholder chooses to take a loan, this would reduce the cash surrender value and, consequently, the available nonforfeiture benefits. Nonforfeiture clauses are also subject to legal regulation and provide certain rights to policyholders. In the United States, insurance is primarily regulated at the state level, and this includes regulations concerning nonforfeiture clauses. These regulations stipulate minimum standards for nonforfeiture benefits and are designed to protect policyholders. Nonforfeiture clauses confer specific rights to policyholders. Essentially, these clauses grant policyholders the right to receive a portion of their benefits even if they discontinue premium payments. It's vital for policyholders to understand these rights and to ensure they're upheld. Despite the regulatory protections, disputes can arise regarding nonforfeiture benefits. These disputes might involve disagreements about the calculation of benefits, the exercise of nonforfeiture options, or the application of these clauses. Depending on the nature of the dispute, resolution might involve negotiation, mediation, or even litigation. Making the most of nonforfeiture clauses requires strategic thinking and careful planning. The decision to choose a policy with a nonforfeiture clause should not be taken lightly. Policyholders need to weigh the benefits of these clauses against the increased cost and consider their financial situation and insurance needs. If a policyholder finds themselves in a position where they can no longer pay premiums, they should carefully evaluate their nonforfeiture options. Each option has different implications, and the best choice will depend on the policyholder's specific circumstances. Given the complexity of nonforfeiture clauses and their implications, it's beneficial for policyholders to seek the advice of financial advisors. These professionals can provide valuable insights and help policyholders make informed decisions about nonforfeiture options. A nonforfeiture clause is an essential provision in insurance contracts that protects policyholders from losing all their benefits if they can no longer continue premium payments. It lays down the framework for preserving some of the policy's value and provides several payout options including cash surrender, conversion to a paid-up policy, extended-term insurance, or policy loans. This clause works by offering policyholders different alternatives based on the cash value accumulated in their policy. However, it's important to note that each option has different implications in terms of the coverage amount, payout period, and potential tax liabilities. With nonforfeiture clauses being an intricate part of insurance policies, it is advisable to engage with an experienced insurance broker who can help guide you through the complexities. This guidance will ensure you make an informed decision that aligns with your financial and coverage needs.What Are Nonforfeiture Clauses?

How a Nonforfeiture Clause Works

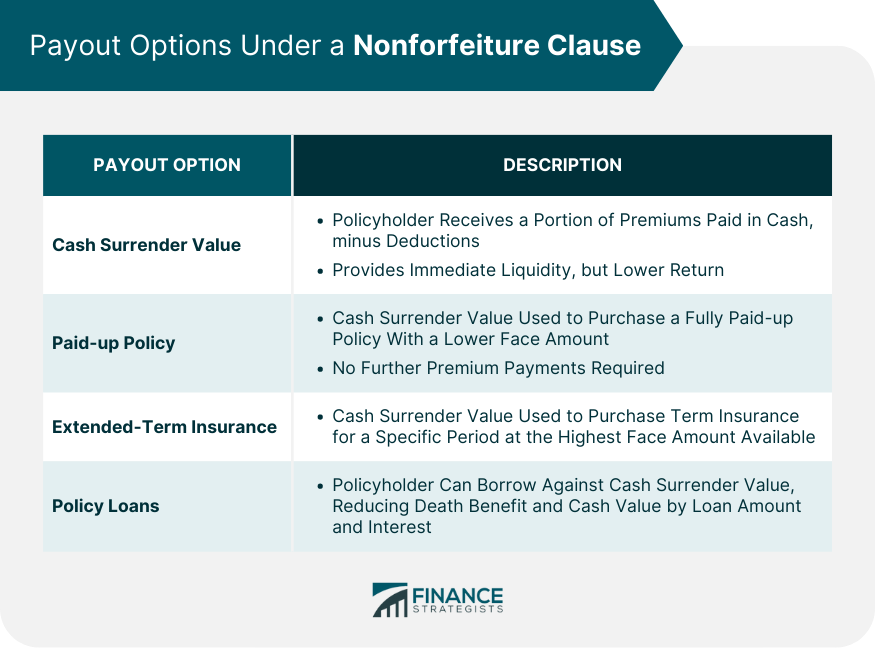

Payout Options Under a Nonforfeiture Clause

Cash Surrender Value

Paid-up Policy

Extended-Term Insurance

Policy Loans

Understanding Nonforfeiture Clauses in Different Contexts

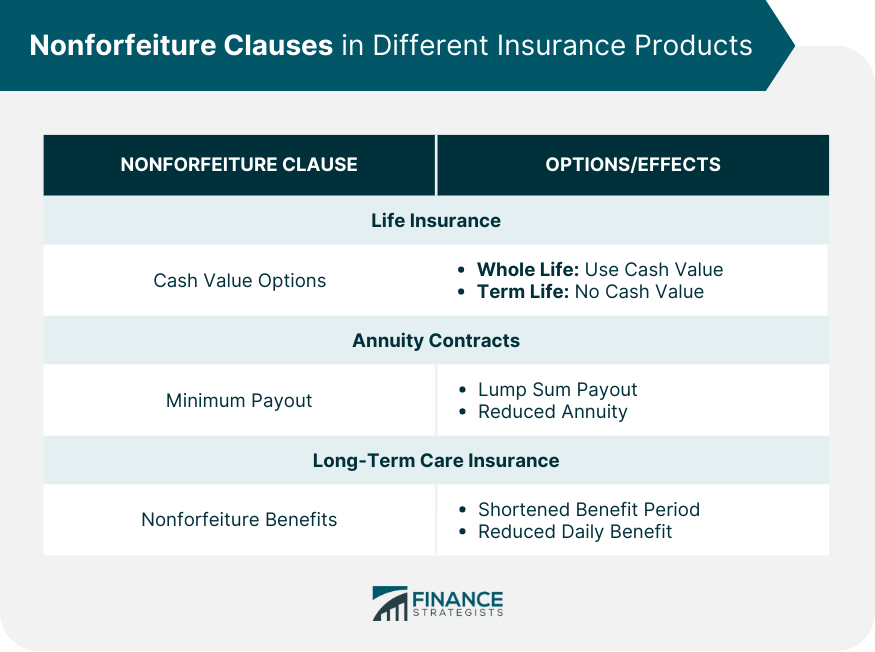

Life Insurance Policies

Annuity Contracts

Long-Term Care Insurance

Financial Implications of Nonforfeiture Clauses

Impact on Policy Premiums

Tax Implications of Nonforfeiture Clauses

Effect on the Cash Value of Policies

Role in Policy Loan Options

Legal Aspects of Nonforfeiture Clauses

State Insurance Regulations Regarding Nonforfeiture Clauses

Legal Rights of Policyholders Under Nonforfeiture Clauses

Nonforfeiture Clause Disputes and Resolutions

Strategic Considerations for Nonforfeiture Clauses

Choosing a Policy With a Nonforfeiture Clause

Evaluating Nonforfeiture Options During Policy Surrender or Lapse

Role of Financial Advisors in Nonforfeiture Decisions

Final Thoughts

Nonforfeiture Clauses FAQs

A nonforfeiture clause is a provision in certain insurance policies that allows policyholders to receive some benefits even if they stop paying premiums.

A nonforfeiture clause works by giving policyholders different options to utilize the accumulated cash value of their policy if they cannot continue premium payments. These options may include a cash surrender, conversion to a paid-up policy, or extended-term insurance.

The common payout options under a nonforfeiture clause include the cash surrender value, a paid-up policy, extended-term insurance, and policy loans.

Yes, the choices you make under a nonforfeiture clause can significantly impact your policy's cash value. For example, if you opt for a cash surrender, the cash value of your policy will be paid out to you, thereby reducing your policy's cash value to zero.

No, nonforfeiture clauses are typically included in whole life and certain types of health insurance policies. They are not generally found in term life insurance policies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.