Estate planning is the process of arranging the management and disposal of a person's estate during their life and at and after death. It incorporates the will, taxes, insurance, property, and trusts to ensure that an individual's assets are distributed according to their wishes and that tax liabilities are minimized. Estate planning is a crucial step for families to protect their wealth and ensure a smooth transition of assets. Without proper planning, a substantial portion of the wealth might end up in the hands of unintended beneficiaries or be eroded due to heavy taxes. When it comes to the wealthy, estate planning takes on a new layer of complexity. Factors such as multiple revenue streams, ownership of business interests, international assets, complex family dynamics, and the desire for philanthropy necessitate bespoke estate planning strategies.

These serve as fundamental blueprints for how a person's assets will be distributed upon their passing. A will provides a basic outline of how assets should be divided, but trusts offer more robust control over asset distribution. For wealthy families, trusts can provide an array of advantages such as privacy, minimizing estate taxes, and potentially protecting assets from creditors. There are many types of trusts, each serving different purposes, and the choice often depends on the specific needs and circumstances of the family. These policies, particularly when housed in an irrevocable life insurance trust, can provide liquidity to cover estate taxes and other expenses after death. This ensures that assets won't have to be sold under unfavorable conditions to meet tax obligations. Additionally, life insurance can also be a means of creating wealth for the next generation in a tax-efficient manner, particularly for those families where much of the wealth is tied up in illiquid assets such as businesses or real estate. Estate and gift taxes can erode the wealth of a family if not properly planned for. Strategies for minimizing these taxes might include gifting during life to utilize the annual gift tax exclusion, setting up charitable trusts, or creating family limited partnerships or LLCs. Tax laws are complex and often changing, making professional advice essential in this aspect of estate planning. This not only fulfills their desire to give back to the community but can also provide significant tax benefits. Charitable trusts, for example, can remove assets from the taxable estate while providing a lifetime income stream to the donor. Donor-advised funds offer an immediate tax deduction while allowing the donor to recommend grants from the fund over time. Family limited partnerships (FLPs) or family limited liability companies (LLCs) can serve multiple purposes in an estate plan. They allow for the centralized management of family assets, which can be particularly beneficial for families owning substantial real estate or business interests. They also provide a degree of asset protection from creditors and can be used to consolidate family wealth. Moreover, they might offer tax benefits in the form of valuation discounts for gift and estate tax purposes. A well-thought-out plan will ensure a smooth transition of control upon the owner's retirement, incapacity, or death, thereby preserving the value of the business. It can also help prevent family disputes by clearly outlining who will take over the business and how the transition will occur. A succession plan might include buy-sell agreements funded by life insurance, gifting of business interests, or even sale to an employee stock ownership plan (ESOP). A well-crafted estate plan can safeguard the family's assets against potential financial risks such as lawsuits, creditors, or ex-spouses in the case of divorce. Trust structures, for example, provide a protective shield for the assets, ensuring that the wealth accumulated over generations stays within the family and is utilized according to the family's intentions. High-net-worth families can face considerable estate taxes, which can erode the value of the inheritance. However, through effective use of estate planning tools such as trusts, gifting strategies, and life insurance policies, families can significantly reduce or even eliminate estate and gift taxes. For instance, annual tax-free gifting allows wealthy families to pass on a portion of their wealth during their lifetime, reducing the size of their taxable estate. Affluent families often have unique wishes and goals for their wealth, such as providing for a special needs family member, ensuring the continuity of a family business, or supporting charitable causes. A comprehensive estate plan, complete with wills and various types of trusts, allows wealthy families to dictate exactly how, when, and to whom their assets will be distributed. Succession planning, a vital component of estate planning, ensures that the business continues to thrive under new leadership. A clear and legally sound succession plan can prevent potential disputes that could destabilize the business and can also provide tax efficiencies during the transition. Whether the legacy is a family business, a philanthropic endeavor, or a significant piece of property, an estate plan ensures that the family's wishes are respected and fulfilled. This preservation of the family's values and impact can be a source of unity and pride for future generations. The process requires attention to detail and knowledge of intricate tax laws, estate laws, and financial regulations. The complexity multiplies when there are diverse types of assets involved, such as international assets, business holdings, or complex financial instruments. Not only does this complexity demand significant expertise, but it also makes the process time-consuming. Time needs to be invested in crafting a comprehensive plan, periodically reviewing it, and modifying it as the personal circumstances or laws change. Engaging the services of professionals like estate planning attorneys, financial advisors, CPAs, and insurance advisors can be expensive, but their expertise is often crucial in creating an effective estate plan. Additionally, costs may be incurred in setting up and maintaining structures like trusts, LLCs, or insurance policies, which form a part of many estate plans for wealthy families. Tax laws and estate laws are not set in stone; they change over time, influenced by various factors such as the political climate, economic conditions, and policy objectives of the government of the day. Therefore, what seems like an efficient estate plan today might not be as advantageous tomorrow if the laws change. For instance, shifts in estate tax exemptions or rates can significantly impact the tax efficiency of an estate plan. This involves introspective consideration of what you want to happen to your wealth after you're gone. Do you want to pass it down to the next generation intact, or do you want to distribute it among different causes and investments? How do you see your family's role in the businesses or investments you've established? Do you have any specific philanthropic causes you wish to support? Your objectives will be the foundation upon which your estate plan is built, and thus, the clarity of these goals is crucial. This team typically includes an estate planning attorney, a certified public accountant (CPA), a financial advisor, an insurance advisor, a trust officer, and possibly a family business consultant. These professionals, each an expert in their respective field, will collaborate to ensure that your estate plan optimally meets your objectives while complying with all relevant legal and tax regulations. Estate planning is not a one-time task but a dynamic process that needs to reflect changes in your personal circumstances, your asset portfolio, and the legal and regulatory environment. For example, the birth of a new family member, the acquisition or disposal of a significant asset, or a change in estate tax laws could all necessitate a review and update of your estate plan. While discussions about estate planning can sometimes be sensitive, clear and open communication with your heirs can prevent misunderstandings and potential disputes in the future. It's beneficial for your heirs to understand the structure and reasoning behind your estate plan, their roles and responsibilities, and the professionals they can turn to for guidance. Family meetings, possibly facilitated by a family business consultant or a family wealth advisor, can provide a forum for these discussions. These attorneys specialize in wills, trusts, probate, and estate planning. They guide the creation of estate planning documents and ensure legal compliance. By working closely with an attorney, families can ensure their estate plan is valid, clear, and aligned with current legislation. Moreover, in the event of complex family dynamics or litigation, an estate planning attorney can provide invaluable legal advice and representation. Certified Public Accountants (CPA) can help families structure their estate in a way that minimizes estate, gift, and income tax liabilities. They also help with annual tax filings, keeping track of changes in tax laws, and advising on the tax implications of various estate planning strategies. Financial advisors help families manage and grow their wealth, thus directly influencing the size of the estate. They provide advice on investment strategies, risk management, and overall wealth preservation. For wealthy families, a financial advisor might also coordinate with other team members on issues such as estate liquidity needs, the financial aspects of business succession, and the integration of life insurance into the estate plan. An insurance advisor can help assess the need for life insurance, the right type and amount of coverage, and the most effective ways of policy ownership and beneficiary designation. Their responsibilities can include managing trust assets, overseeing investment portfolios, and making distributions to beneficiaries according to the trust's terms. For wealthy families with multiple or complex trusts, a trust officer can provide essential expertise to ensure these legal arrangements operate smoothly and effectively. They can help create succession plans, manage family dynamics within the business context, advise on business valuation and restructuring, and work closely with other team members to integrate the business aspects into the overall estate plan. This professional guidance is invaluable in facilitating a smooth business transition and preventing future disputes. Estate planning is crucial for wealthy families to protect their assets, minimize taxes, and facilitate a smooth transition of wealth. By utilizing elements such as wills, trusts, life insurance, tax planning, philanthropy, family limited partnerships, and business succession planning, affluent families can effectively manage and distribute their wealth according to their goals and intentions. Estate planning provides benefits such as wealth preservation, reduced taxes, controlled wealth distribution, facilitated business transitions, and legacy assurance. While there are complexities, costs, and potential legislative changes involved in estate planning for wealthy families, these drawbacks can be addressed through careful consideration and collaboration with a team of professionals. Estate planning attorneys, CPAs, financial advisors, insurance advisors, trust officers, and family business consultants play essential roles in creating and maintaining effective estate plans that comply with current laws and regulations. By establishing clear objectives, collaborating with professionals, regularly updating plans, and communicating openly with heirs, affluent families can navigate the intricacies of estate planning, preserve their wealth, and ensure a lasting legacy for future generations.Overview of Estate Planning

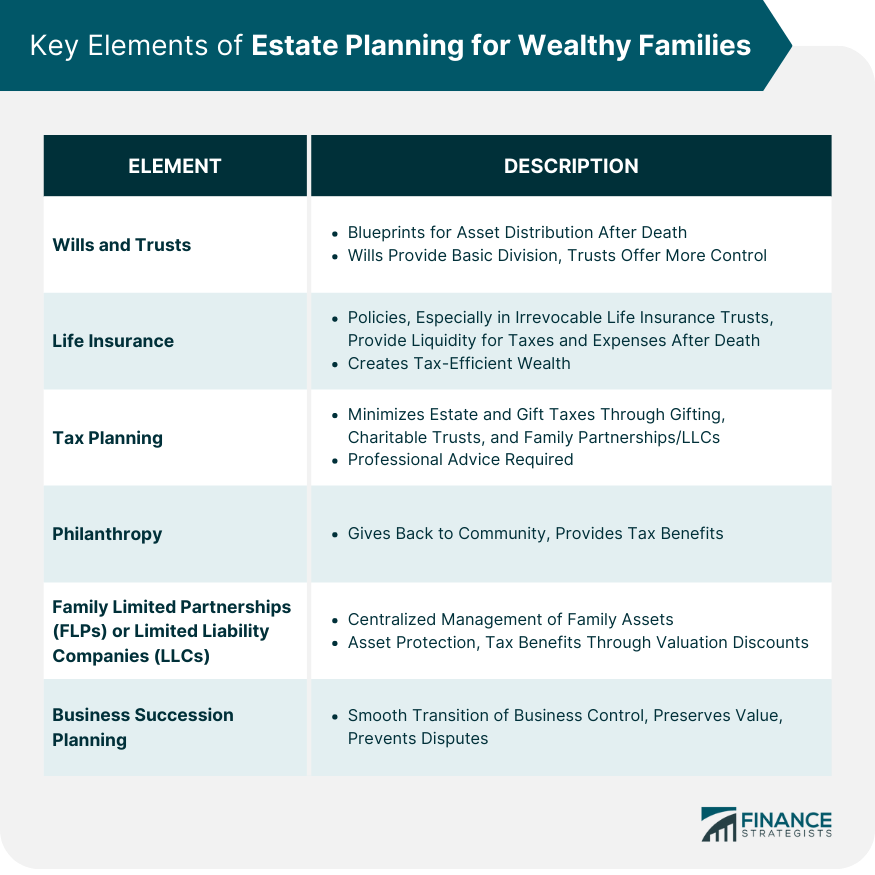

Key Elements of Estate Planning for Wealthy Families

Wills and Trusts

Life Insurance

Tax Planning

Philanthropy

Family Limited Partnerships or Limited Liability Companies

Business Succession Planning

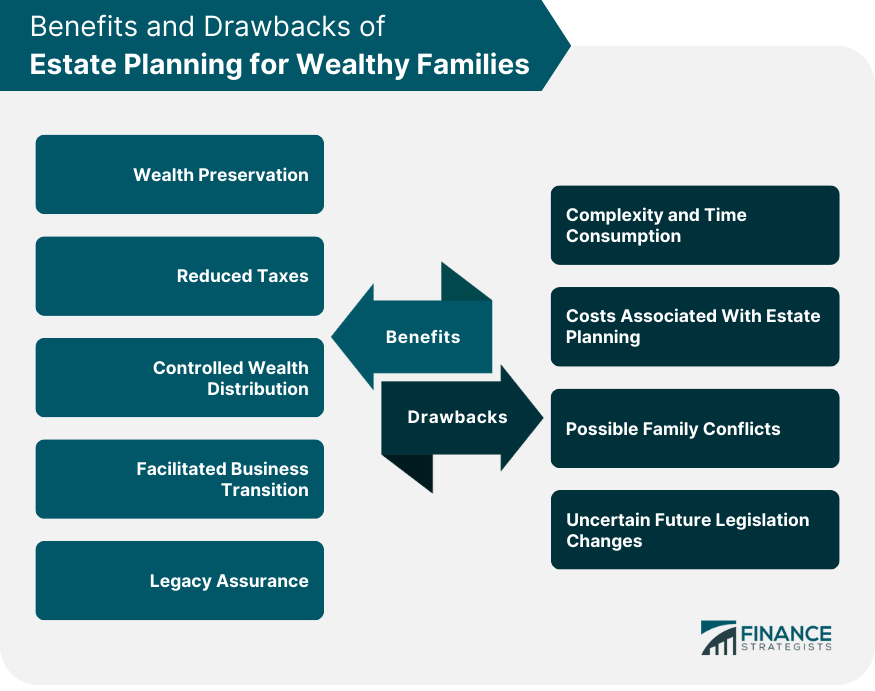

Benefits of Estate Planning for Wealthy Families

Wealth Preservation

Reduced Taxes

Controlled Wealth Distribution

Facilitated Business Transition

Legacy Assurance

Drawbacks of Estate Planning for Wealthy Families

Complexity and Time Consumption

Costs

Future Legislation Changes

How to Approach Estate Planning as a Wealthy Family

Establish Clear Objectives

Collaborate With Professionals

Regularly Update Your Estate Plan

Communicate With Heirs

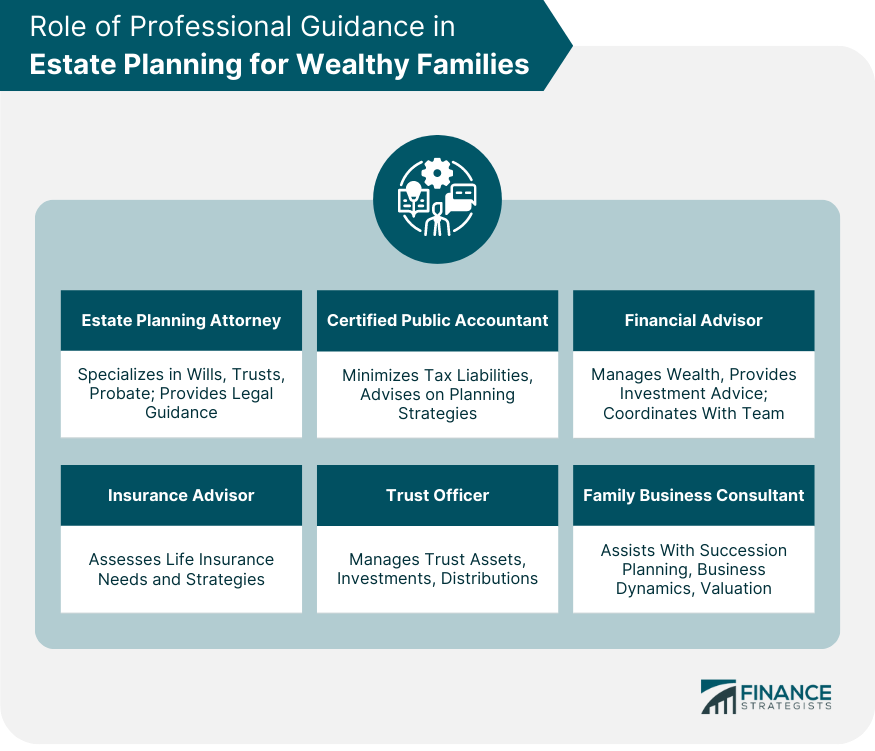

Role of Professional Guidance in Estate Planning for Wealthy Families

Estate Planning Attorney

Certified Public Accountant

Financial Advisor

Insurance Advisor

Trust Officer

Family Business Consultant

Final Thoughts

Estate Planning for Wealthy Families FAQs

Estate planning is important for wealthy families to protect their assets, minimize tax liabilities, ensure a smooth transition of wealth, and preserve their family legacy for future generations.

Key elements of estate planning for wealthy families include wills and trusts, life insurance, tax planning strategies, philanthropy, family limited partnerships or limited liability companies, and business succession planning.

Estate planning can help minimize taxes for wealthy families through strategies such as gifting during life to utilize the annual gift tax exclusion, setting up charitable trusts, creating family limited partnerships or LLCs, and utilizing life insurance policies held in irrevocable life insurance trusts.

Yes, professional guidance is crucial for estate planning. Estate planning attorneys, CPAs, financial advisors, insurance advisors, trust officers, and family business consultants provide expertise in their respective fields to create effective estate plans, ensure compliance with legal and tax regulations, and address the unique needs and goals of wealthy families.

Estate planning is an ongoing process. While the initial creation of an estate plan is important, it should be regularly reviewed and updated to reflect changes in personal circumstances, asset portfolios, and legal and regulatory environments. Births, deaths, marriages, acquisitions, disposals, and changes in tax laws are some events that may trigger the need for an estate plan review and update.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.