Estate tax exemptions refer to the amount of an estate's value that is not subject to federal or state estate taxes. The exemption amount is determined by the government and can be adjusted based on various economic and political factors. As of 2026, the federal estate tax exemption is $15 million ($13.99 million in 2025) per individual, while some states have their own estate tax with varying exemption amounts. Proper estate planning can help individuals maximize their exemption and minimize their tax liability. Over the years, the federal estate tax exemption amount has changed due to legislative adjustments and economic factors. These changes have generally increased the exemption amount, reducing the number of estates subject to taxation. As of 2026, the federal estate tax exemption stands at $15 million ($13.99 million in 2025) per individual. This means that estates valued at or below this amount are not subject to federal estate tax, while those exceeding this threshold are taxed at a rate that ranges from 18% to 40%. The federal estate tax exemption is adjusted annually for inflation, ensuring that the exemption amount remains relevant as economic conditions change. This allows for a more equitable application of the estate tax and prevents undue hardship on taxpayers. In addition to the federal estate tax exemption, several states also impose their own estate tax with varying exemption amounts. Some states conform to the federal exemption amount, while others set their own, often lower, exemption thresholds. State estate tax exemption amounts can differ significantly from the federal exemption, which is why it is essential for individuals to be aware of the specific exemption thresholds in their state of residence. In some cases, state estate tax exemptions are portable, meaning that a surviving spouse can utilize any unused portion of their deceased spouse's exemption. This can be particularly beneficial in reducing or eliminating state estate tax liabilities. Portability is a feature of the federal estate tax exemption that allows a surviving spouse to claim any unused portion of their deceased spouse's exemption amount, effectively increasing their own exemption. To claim portability, the executor of the deceased spouse's estate must file an estate tax return (Form 706) within nine months of the date of death, even if no estate tax is due. This filing enables the surviving spouse to utilize the unused exemption in the future. Portability can provide significant tax savings for married couples, particularly those with substantial assets. By combining both spouses' exemptions, a couple can shield a larger portion of their estate from taxation. While portability offers numerous benefits, it is essential to note that it only applies to the federal estate tax exemption and may not be available for state estate tax exemptions. Additionally, portability does not extend to other estate planning techniques, such as the use of trusts. One strategy for maximizing the estate tax exemption is to make gifts during one's lifetime. The annual gift tax exclusion allows individuals to gift up to $19,000 per recipient in 2026 (also $19,000 in 2025) without incurring gift tax or reducing their lifetime gift tax exemption. In addition to the annual exclusion, individuals can also make use of the lifetime gift tax exemption. This exemption, which is equal to the federal estate tax exemption, allows individuals to make cumulative gifts above the annual exclusion amount without incurring gift tax or affecting their estate tax exemption. Revocable living trusts can be an effective estate planning tool for maximizing estate tax exemption. These trusts allow individuals to transfer assets into the trust during their lifetime, avoiding probate and providing more control over asset distribution. However, assets in a revocable living trust are still considered part of the grantor's taxable estate for estate tax purposes. Irrevocable trusts can provide even more significant tax benefits, as assets placed in these trusts are removed from the grantor's taxable estate. This can reduce or eliminate estate tax liability while still providing for the grantor's beneficiaries. However, irrevocable trusts cannot be altered or revoked once established, so it's crucial to carefully consider the implications before implementing this strategy. Charitable trusts are another option for maximizing estate tax exemption while also supporting a philanthropic cause. These trusts can be structured to provide income to beneficiaries for a specified period, with the remaining assets ultimately passing to a designated charity. This strategy can reduce estate tax liability and provide significant income tax deductions for the grantor. Family limited partnerships (FLPs) can be used to transfer assets to family members while retaining control over the assets and reducing estate tax liability. FLPs can provide valuation discounts, as the transferred interests may be valued lower due to limited marketability and lack of control, effectively reducing the overall estate value. Grantor retained annuity trusts (GRATs) involve transferring assets into a trust while retaining the right to receive annuity payments for a specified term. At the end of the term, any remaining assets in the trust pass to the beneficiaries. GRATs can be an effective way to transfer asset appreciation to beneficiaries with minimal or no estate tax consequences. Qualified personal residence trusts (QPRTs) involve transferring a personal residence into a trust, with the grantor retaining the right to live in the property for a specified term. After the term, the residence passes to the beneficiaries at a reduced estate tax value. This strategy can be particularly beneficial for individuals with valuable real estate holdings. Certain family farms and businesses may qualify for an additional estate tax exemption, allowing these valuable assets to pass to the next generation with reduced or no estate tax burden. This exemption is intended to preserve family-owned enterprises and protect them from potential financial strain due to estate taxes. Non-resident aliens are subject to U.S. estate tax on their U.S.-situated assets, but they are granted a reduced estate tax exemption of $60,000. Tax treaties with specific countries may provide for a more generous exemption or other benefits, so it's important for non-resident aliens to understand their potential estate tax liability. Transfers of assets between U.S. citizen spouses, either during life or at death, are generally not subject to estate tax due to the unlimited marital deduction. However, transfers to non-citizen spouses may be subject to estate tax, although a generous annual exclusion amount exists for lifetime gifts to non-citizen spouses. The estate tax exemption can significantly impact beneficiaries by reducing or eliminating the estate tax burden, allowing them to inherit assets without the added financial strain of tax liabilities. Maximizing the estate tax exemption may also affect asset distribution among beneficiaries, as individuals may employ various strategies to ensure assets are distributed in a tax-efficient manner. This can include the use of trusts, gifting strategies, and other estate planning techniques to allocate assets among beneficiaries while minimizing estate tax exposure. One critical aspect of estate tax exemption that affects beneficiaries is the step-up in basis. When assets are inherited, their tax basis is "stepped-up" to the fair market value as of the date of the decedent's death. This can minimize or eliminate capital gains tax liability for beneficiaries when they eventually sell the inherited assets, further enhancing the tax benefits of estate tax exemption. Estate tax planning is essential for individuals with substantial assets, as it can help maximize the estate tax exemption and minimize the tax burden on beneficiaries. By understanding the various exemption thresholds, portability, and strategies for maximizing the exemption, individuals can create an effective estate plan that meets their needs and protects their assets for future generations. It is important to review and update estate plans periodically to ensure they remain aligned with one's goals and circumstances. Changes in tax laws, family situations, and financial conditions may necessitate adjustments to the estate plan to optimize tax benefits and protect assets. Given the complexity of estate tax exemption and the various strategies available for maximizing its benefits, it is highly recommended to consult with experienced estate planning professionals, such as attorneys, accountants, and financial advisors. These professionals can provide guidance on the most suitable strategies for one's unique situation and help navigate the often-complex world of estate tax planning.What Are Estate Tax Exemptions?

Estate Tax Exemption Thresholds

Federal Estate Tax Exemption

Historical Exemption Amounts

Current Exemption Amount

Inflation Adjustments

State Estate Tax Exemption

Variations by State

Exemption Amounts

Portability of Exemption

Portability of Estate Tax Exemption

Definition of Portability

Process for Claiming Portability

Benefits of Portability

Limitations of Portability

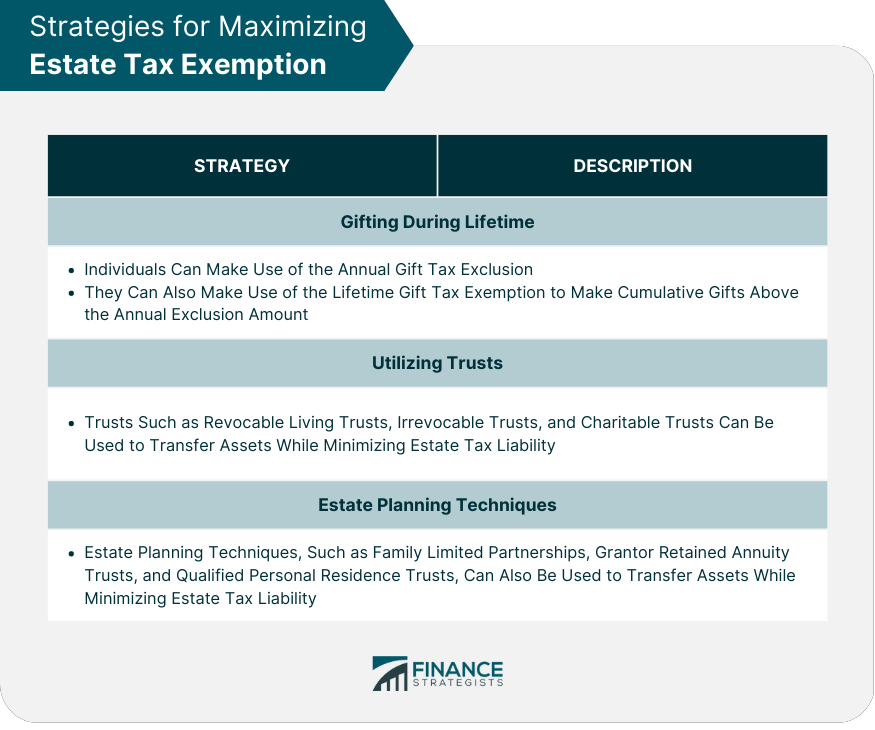

Strategies for Maximizing Estate Tax Exemption

Gifting During Lifetime

Annual Gift Tax Exclusion

Lifetime Gift Tax Exemption

Utilizing Trusts

Revocable Living Trusts

Irrevocable Trusts

Charitable Trusts

Estate Planning Techniques

Family Limited Partnerships

Grantor Retained Annuity Trusts

Qualified Personal Residence Trusts

Estate Tax Exemption in Special Circumstances

Exemption for Family Farms and Businesses

Exemption for Non-resident Aliens

Exemption for Spouses

Impact of Estate Tax Exemption on Beneficiaries

Tax Implications

Asset Distribution

Basis Step-up

Conclusion

Importance of Estate Tax Planning

Periodic Review of Estate Plan

Consulting with Estate Planning Professionals

Estate Tax Exemption FAQs

In 2026, the estate tax exemption is $15 million ($13.99 million in 2025) per individual or $30 million ($27.98 million in 2025) for married couples filing jointly. This means that estates with a value below this amount are exempt from federal estate taxes.

The estate tax exemption is not permanent and may be subject to change. The exemption amount is determined by Congress and may be adjusted based on economic and political factors.

If your estate exceeds the estate tax exemption, the excess amount may be subject to federal estate taxes. The tax rate on the excess amount can be as high as 40%.

Yes, the unused portion of the estate tax exemption can be transferred to a surviving spouse. This is known as portability and allows the surviving spouse to use both their own exemption and the unused portion of their deceased spouse's exemption.

There are several strategies that can be used to reduce estate tax liability, such as gifting, setting up a trust, and using life insurance. It's important to consult with a financial advisor or estate planning attorney to determine the best strategy for your specific situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.