A trust is a legal arrangement that allows individuals or entities to manage their assets and distribute them to beneficiaries. It involves three parties: the grantor, who creates the trust; the trustee, who manages the trust assets; and the beneficiaries, who receive the trust assets. Trusts can be used for a variety of purposes, including estate planning, tax planning, asset protection, and charitable giving. Trusts are an essential tool in managing and protecting assets, and it's crucial to understand how they work. Trusts are essential for estate planning. They help ensure that assets are distributed according to the grantor's wishes and can help avoid the time-consuming and expensive probate process. Probate is the legal process of administering a deceased person's estate, which can be lengthy and costly. Trusts can also help minimize estate taxes, which can significantly reduce the amount of assets passed on to beneficiaries.

Trusts can also be used to provide for family members or other loved ones, particularly those with special needs, by establishing a special needs trust that provides for their care without jeopardizing government benefits. Asset protection is another essential use of trusts. Trusts can shield assets from creditors and lawsuits, making them an essential tool for individuals in high-risk professions or those who may be subject to legal action. Trusts can also protect assets from divorce or bankruptcy proceedings. Additionally, trusts can help maintain privacy by keeping assets out of the public record, as trust documents are not generally available to the public. By using trusts, individuals can take control of their assets and ensure that they are protected and distributed according to their wishes. Trusts involve three parties: the grantor, the trustee, and the beneficiaries. The grantor is the person who creates the trust and transfers assets into the trust. The trustee is the person or institution that manages the trust assets and distributes them to the beneficiaries according to the terms of the trust. The beneficiaries are the individuals or organizations that receive the trust assets. To create a trust, the grantor must draft a trust document that specifies the terms of the trust, including the assets to be transferred, the beneficiaries, and the conditions for distributing the assets. The trust must also be funded, which means transferring assets to the trust. Trust assets can include real estate, stocks, bonds, and cash. The trustee is responsible for managing and investing the assets, and distributing them to the beneficiaries according to the terms of the trust document. Trusts can be created during the grantor's lifetime, which is known as a living trust, or after their death, which is known as a testamentary trust. Living trusts can be revocable or irrevocable. Revocable trusts allow the grantor to change or cancel the trust, while irrevocable trusts cannot be changed or revoked. There are several different types of trusts available, each with its own unique purpose and benefits. Living trusts are created during the grantor's lifetime and can be revocable or irrevocable. Revocable living trusts are the most common type of living trust and allow the grantor to change or revoke the trust at any time. Irrevocable living trusts, on the other hand, cannot be changed or revoked once they are created. Living trusts are commonly used for estate planning, asset protection, and probate avoidance. Testamentary trusts are established through a will and become effective after the grantor's death. Unlike living trusts, testamentary trusts are subject to probate and are typically used for specific purposes, such as providing for minor children or disabled beneficiaries. Revocable trusts can also be established through a will and become effective after the grantor's death. Irrevocable trusts are trusts that cannot be changed or revoked once they are established. Irrevocable trusts are commonly used for tax planning, asset protection, and charitable giving. Special needs trusts are designed to provide for beneficiaries with disabilities without disqualifying them from receiving government benefits. Charitable trusts are established to support charitable organizations or causes and can provide significant tax benefits to the grantor. A trust is a legal arrangement where one party holds property for the benefit of another party. There are several benefits to setting up a trust, which we will explore in this section. One of the primary benefits of a trust is the avoidance of probate. Probate is the legal process of settling a person's estate after they die. It involves validating the will, identifying and appraising assets, paying debts and taxes, and distributing the remaining assets to the beneficiaries. Probate can be time-consuming, expensive, and public. With a trust, however, the assets are already in the trust and can be distributed to the beneficiaries without going through probate. Another benefit of a trust is asset protection. With a trust, you can protect your assets from creditors, lawsuits, and other potential threats. This is because the assets in the trust are technically owned by the trust and not by the individual. As a result, they are shielded from potential liabilities and can be distributed according to the terms of the trust. Trusts can also be useful for tax planning. There are several types of trusts that can help reduce or eliminate estate taxes, gift taxes, and income taxes. For example, a grantor-retained annuity trust (GRAT) can be used to transfer assets to beneficiaries while minimizing gift taxes. A charitable remainder trust (CRT) can be used to donate assets to a charity while still receiving income from the assets during your lifetime. Trusts can also be helpful for incapacity planning. With a revocable living trust, for example, you can appoint a successor trustee to manage your assets in the event that you become incapacitated. This can help ensure that your assets are managed according to your wishes, even if you are unable to make decisions for yourself. Trusts can also provide privacy. Unlike wills, which are public documents, trusts are private. This means that the terms of the trust and the assets within it are not a matter of public record. This can be important for individuals who value their privacy and want to keep their financial affairs confidential. Finally, trusts can be very flexible. They can be tailored to meet the specific needs of the individual and can be used for a wide range of purposes. For example, a special needs trust can be used to provide for a person with disabilities without jeopardizing their eligibility for government benefits. A spendthrift trust can be used to protect assets from a beneficiary who may not be financially responsible. Overall, trusts offer a lot of flexibility in how assets are managed and distributed. While trusts offer many benefits, there are also some drawbacks to consider. In this section, we will explore some of the potential downsides of setting up a trust. One of the biggest drawbacks of trusts is the cost of setting them up and maintaining them. Trusts can be complex legal documents that require the assistance of an attorney. The cost of setting up a trust will vary depending on the type of trust, the complexity of the document, and the attorney's fees. In addition, trusts may require ongoing maintenance, such as filing tax returns or updating the trust document, which can also be costly. Another potential drawback of trusts is the loss of control. Once assets are transferred into a trust, they are no longer owned by the individual. Instead, they are owned by the trust, which is managed by a trustee. This means that the individual may have limited control over how the assets are managed and distributed. While the trustee is obligated to follow the terms of the trust document, there may be some restrictions on how the assets can be used. In some cases, setting up a trust may limit access to trust assets. For example, if a person sets up an irrevocable trust, they cannot change the terms of the trust or access the assets in the trust without the permission of the trustee. This can be problematic if the individual needs access to the assets but cannot get permission from the trustee. It's important to carefully consider the terms of the trust and the potential limitations on access to the assets before setting up a trust. Finally, trusts can be subject to complex legal requirements. For example, certain types of trusts may require annual tax returns, or may require that certain actions be taken by a specific deadline. Failing to comply with these requirements can result in penalties or other legal consequences. It's important to work with an experienced attorney when setting up a trust to ensure that all legal requirements are met. While trusts offer many benefits, they are not for everyone. It's important to carefully consider the potential drawbacks before deciding to set up a trust. One of the most significant drawbacks is the cost of setting up and maintaining a trust, which can be substantial. Additionally, trusts may limit access to assets, and may result in a loss of control over those assets. However, for many individuals, the benefits of a trust outweigh the drawbacks. When considering a trust, it's important to work with an experienced estate planning attorney who can help you understand the options and guide you through the process. An attorney can help you choose the right type of trust for your needs, draft a clear and effective trust document, and ensure that all legal requirements are met. Overall, trusts can be a powerful tool for estate planning, tax planning, and asset protection. However, they require careful consideration and planning. If you are considering setting up a trust, it's important to work with a knowledgeable and experienced attorney who can help you navigate the process and ensure that your goals are met.What Is a Trust?

Purpose of Trusts

How Trusts Work

Types of Trusts

Living Trusts

Testamentary Trusts

Revocable Trusts

Irrevocable Trusts

Special Needs Trusts

Charitable Trusts

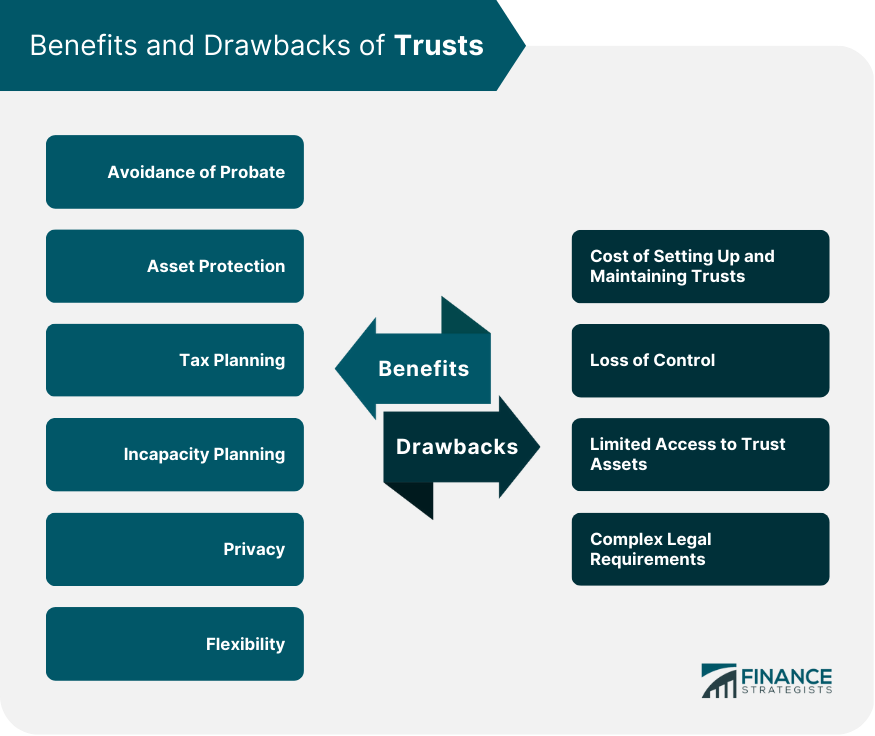

Benefits of Trusts

Avoidance of Probate

Asset Protection

Tax Planning

Incapacity Planning

Privacy

Flexibility

Drawbacks of Trusts

Cost of Setting Up and Maintaining Trusts

Loss of Control

Limited Access to Trust Assets

Complex Legal Requirements

Final Thoughts

Trusts FAQs

A trust is a legal arrangement where one party holds property for the benefit of another party. The person who creates the trust is known as the "grantor," the person who manages the trust is known as the "trustee," and the person who benefits from the trust is known as the "beneficiary."

Some benefits of a trust include avoiding probate, protecting assets from creditors, reducing or eliminating taxes, planning for incapacity, providing privacy, and offering flexibility in managing and distributing assets.

The cost of setting up a trust varies depending on the type of trust and the complexity of the document. It's important to work with an experienced attorney to ensure that the trust is set up correctly and all legal requirements are met.

Choosing the right type of trust depends on your specific goals and needs. An experienced attorney can help you understand the options and choose the right type of trust for your situation.

Whether or not you can change the terms of a trust depends on the type of trust. With a revocable living trust, the terms can be changed at any time. With an irrevocable trust, the terms cannot be changed without the permission of the trustee. It's important to carefully consider the terms of the trust before setting it up to ensure that they meet your long-term goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.