Trust tax planning is a crucial aspect of financial and estate planning that involves using trusts to minimize tax liabilities and maximize wealth preservation. A trust is a legal arrangement in which one party, known as the grantor or settlor, transfers assets to another party, known as the trustee, to hold and manage for the benefit of one or more beneficiaries. Trust tax planning encompasses the various strategies and considerations for establishing and managing trusts to achieve specific tax and financial objectives. Trusts can be used for various purposes, including asset protection, income shifting, and charitable giving. Trust tax planning is important for several reasons. First, it can help individuals and families reduce their overall tax burden by taking advantage of various tax benefits associated with trusts. For example, certain types of trusts can be used to shift income to beneficiaries in lower tax brackets, thereby reducing the overall tax liability. Second, trust tax planning plays a key role in estate planning by helping individuals and families preserve and transfer wealth to future generations tax-efficiently. Trusts can also be used to avoid the probate process, which can be time-consuming and costly.

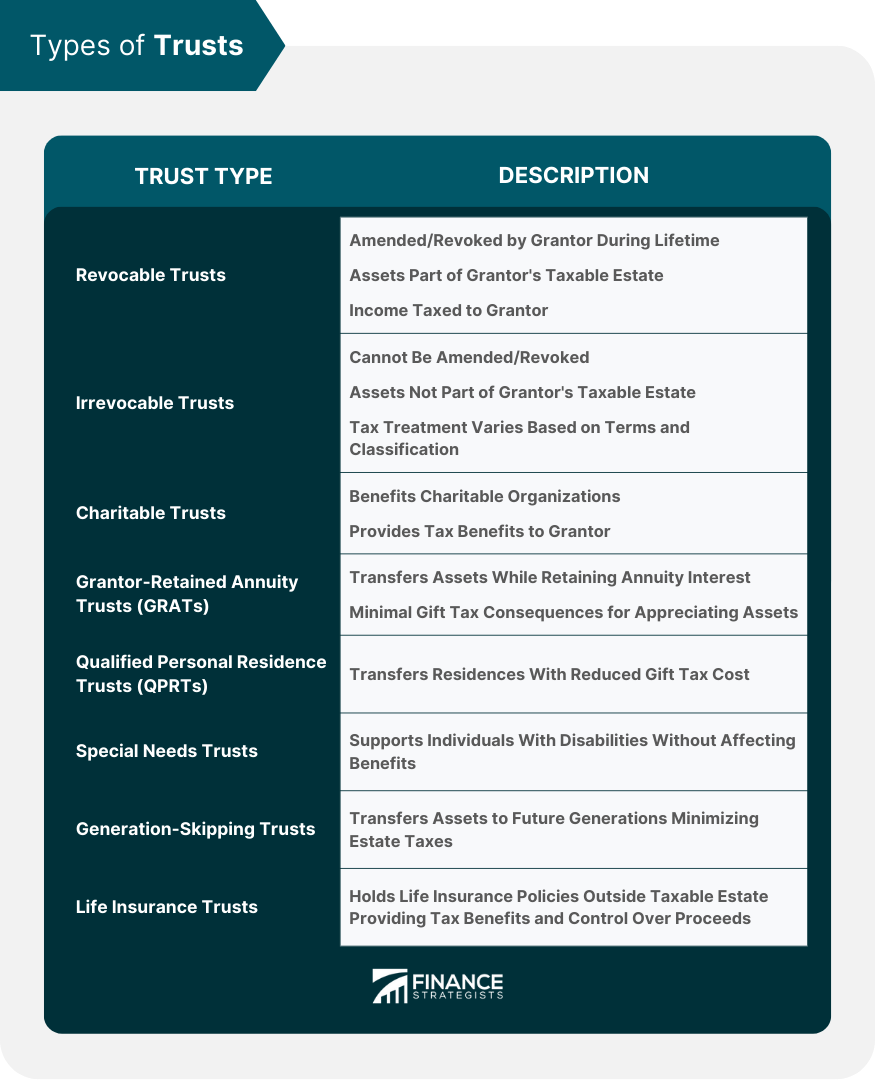

Revocable trusts, also known as living trusts, are trusts that can be amended or revoked by the grantor during their lifetime. The grantor retains control over the assets in the trust and can make changes to the trust terms or beneficiaries as needed. Because the grantor retains control, the assets in a revocable trust are considered part of the grantor's taxable estate for estate tax purposes. Additionally, income generated by the trust assets is typically taxed to the grantor. In contrast to revocable trusts, Irrevocable trusts cannot be amended or revoked once established. The grantor relinquishes control over the assets placed in the trust, and the trust becomes a separate legal entity. As a result, the assets in an irrevocable trust are generally not considered part of the grantor's taxable estate, which can provide significant estate tax benefits. The tax treatment of income an irrevocable trust generates depends on the trust's specific terms and whether it is classified as a grantor or non-grantor trust for tax purposes. Several specialized types of trusts can be used for specific tax planning purposes. Charitable trusts, for example, are irrevocable trusts established to benefit charitable organizations. These trusts can provide the grantor income tax and estate tax benefits. Grantor-retained annuity trusts (GRATs) allow the grantor to transfer assets to beneficiaries while retaining an annuity interest for a specified term. GRATs can be an effective tool for transferring appreciating assets with minimal gift tax consequences. Qualified personal residence trusts (QPRTs) are used to transfer personal residences to beneficiaries at a reduced gift tax cost. Other specialized trusts include special needs, generation-skipping, and life insurance trusts, each with unique tax considerations and benefits. Trusts are generally required to obtain a tax identification number, known as an Employer Identification Number (EIN), from the Internal Revenue Service (IRS). The EIN is used to identify the trust for tax reporting purposes. To obtain an EIN, the trustee must complete and submit IRS Form SS-4, "Application for Employer Identification Number." It is important to note that revocable trusts generally do not need a separate EIN during the grantor's lifetime, as the trust's income and deductions are reported on the grantor's individual income tax return using the grantor's Social Security number. Trusts are subject to income taxation, and trust income tax rules can be complex. Trusts are generally required to file an annual income tax return using IRS Form 1041, "U.S. Income Tax Return for Estates and Trusts." Trusts may be subject to taxation on their undistributed income, and beneficiaries may be taxed on income distributed to them from the trust. The concept of distributable net income (DNI) is central to trust income taxation, as it determines the amount of income taxable to the trust and the amount taxable to the beneficiaries. DNI is generally defined as the trust's total income minus certain deductions and expenses. Trusts can play a significant role in estate and gift tax planning. By transferring assets to an irrevocable trust, a grantor can remove those assets from their taxable estate, potentially reducing estate tax liability. Trusts can also be used to leverage the federal estate and gift tax exemption, which allows individuals to transfer a certain amount of assets free of estate and gift tax. Additionally, trusts can be structured to minimize or avoid generation-skipping transfer (GST) tax, which applies to transfers to beneficiaries who are more than one generation below the grantor. Income shifting is a tax planning strategy that involves transferring income-producing assets to individuals or entities in lower tax brackets. Trusts can be an effective tool for income shifting, particularly when the beneficiaries are in lower tax brackets than the grantor. For example, a grantor can establish a trust to benefit their children or grandchildren and transfer income-producing assets to the trust. The income generated by the trust assets may be taxed at the beneficiaries' lower tax rates. Grantor trusts, in which the grantor is treated as the owner of the trust assets for income tax purposes, can also be used for income shifting, depending on the grantor's tax situation. Asset protection is a key consideration in trust tax planning. By transferring assets to an irrevocable trust, a grantor can protect those assets from creditors and legal claims. Trusts can also provide protection in the event of divorce or other legal disputes. When selecting a trust for asset protection purposes, it is important to consider the specific terms of the trust and the laws of the jurisdiction in which it is established. Some jurisdictions offer greater asset protection benefits than others, and certain types of trusts may provide stronger protection than others. Trusts can be an effective tool for charitable giving, providing both tax benefits and the opportunity to support charitable causes. Charitable remainder trusts (CRTs) and charitable lead trusts (CLTs) are two common types of charitable trusts. CRTs provide the grantor or other non-charitable beneficiaries with an income stream for a specified period, with the remainder of interest passing to charity. Conversely, CLTs provide an income stream to charity for a specified period, with the remainder of interest passing to non-charitable beneficiaries. Both CRTs and CLTs offer income, estate, and gift tax benefits. Trusts are a fundamental component of estate planning, allowing individuals and families to tax-efficiently transfer wealth to future generations. Trusts can be used to minimize estate taxes, maximize wealth transfer, and provide for the management and distribution of assets according to the grantor's wishes. Trusts can also be used to avoid probate, which can be a lengthy and costly process. By carefully structuring and funding trusts, individuals and families can achieve their estate planning goals while preserving their legacy for future generations. Properly funding a trust is critical in the trust tax planning process. Failure to properly fund a trust can result in unintended tax consequences and may undermine the trust's intended purpose. For example, if a grantor establishes a trust for asset protection purposes but fails to transfer assets to the trust, the assets may remain vulnerable to creditors and legal claims. Best practices for funding a trust include ensuring that assets are properly titled in the name of the trust and that the trust is adequately funded to achieve its objectives. It is also important to periodically review and update the trust's funding to account for changes in assets and circumstances. Choosing a competent and trustworthy trustee is essential to the success of a trust. The trustee manages the trust assets, distributes them to beneficiaries, and fulfills various fiduciary duties. A trustee's actions can have significant tax implications, and failure to fulfill fiduciary duties can result in legal liability. When selecting a trustee, grantors should consider factors such as the trustee's experience, expertise, and ability to act impartially. It may also be beneficial to appoint a co-trustee or successor trustee to ensure continuity of trust management. Drafting trust documents is a complex task that requires careful attention to detail and a thorough understanding of trust law and tax regulations. Common mistakes in drafting trust documents include ambiguous language, failure to address contingencies and omission of key provisions. These errors can lead to disputes among beneficiaries, unintended tax consequences, and other issues that may undermine the trust's effectiveness. Working with a qualified attorney specializing in trust and estate planning is important to avoid these pitfalls. A well-drafted trust document should clearly outline the trust's terms, specify the trustee's powers and duties, and address potential scenarios that may arise during the trust's administration. Trust tax planning is valuable for individuals and families seeking to minimize tax liabilities, protect assets, and achieve their estate planning goals. Grantors can make informed decisions that align with their financial objectives by understanding the different types of trusts, the basics of trust taxation, and the various strategies available for trust tax planning. Trust tax planning is a dynamic process that requires ongoing review and adjustment to account for changes in tax laws, asset values, and personal circumstances. Given the complexity of trust tax planning, seeking professional advice from qualified legal and tax services professionals is important. An experienced attorney can help draft trust documents that accurately reflect the grantor's intentions, while a knowledgeable tax advisor can provide guidance on the tax implications of various trust structures. Ultimately, trust tax planning is a powerful tool for preserving and transferring wealth, and careful planning can help ensure that a grantor's legacy endures for generations to come.What Is Trust Tax Planning?

Types of Trusts

Revocable Trusts

Irrevocable Trusts

Special Types of Trusts

Trust Taxation Basics

Tax Identification Number for Trusts

Trust Income Taxation

Estate and Gift Tax Considerations

Trust Tax Planning Strategies

Income Shifting Strategies

Asset Protection Strategies

Charitable Giving Strategies

Estate Planning Strategies

Common Trust Tax Planning Pitfalls

Improper Trust Funding

Trustee Selection and Duties

Trust Document Drafting Errors

Conclusion

Trust Tax Planning FAQs

Trust tax planning is a strategy that involves the use of trusts to minimize tax liabilities, protect assets, and manage wealth distribution. Trusts can be structured in various ways to achieve different tax advantages, such as reducing estate taxes, avoiding probate, and providing for efficient wealth transfer.

Trust tax planning can help reduce estate taxes by removing assets from your estate. When you transfer assets into a trust, they are no longer considered part of your taxable estate. This can significantly reduce the estate tax that may be due upon death. Certain types of trusts, like irrevocable life insurance trusts, can be particularly effective for this purpose.

When planning for income tax, it's important to understand that trusts are separate taxable entities with their own tax brackets, often higher than individual tax brackets. Therefore, the type of trust you choose, its structure, and the timing of income distributions can significantly impact the overall tax liability.

Yes, trust tax planning can be an effective tool for charitable giving. For example, a charitable remainder trust (CRT) allows you to donate assets to the trust and receive an income stream for a certain period. At the end of that period, the remaining assets go to the charity. This strategy provides immediate tax benefits, an income stream, and ultimately benefits the charity.

While trust tax planning can offer significant benefits, it has potential downsides. Trusts can be complex and costly to establish and maintain. They also require you to give up some control over the assets you transfer into them, particularly in the case of irrevocable trusts. Additionally, tax laws are subject to change, which could impact the effectiveness of trust tax strategies. Therefore, working with a knowledgeable advisor is crucial when implementing trust tax planning strategies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.