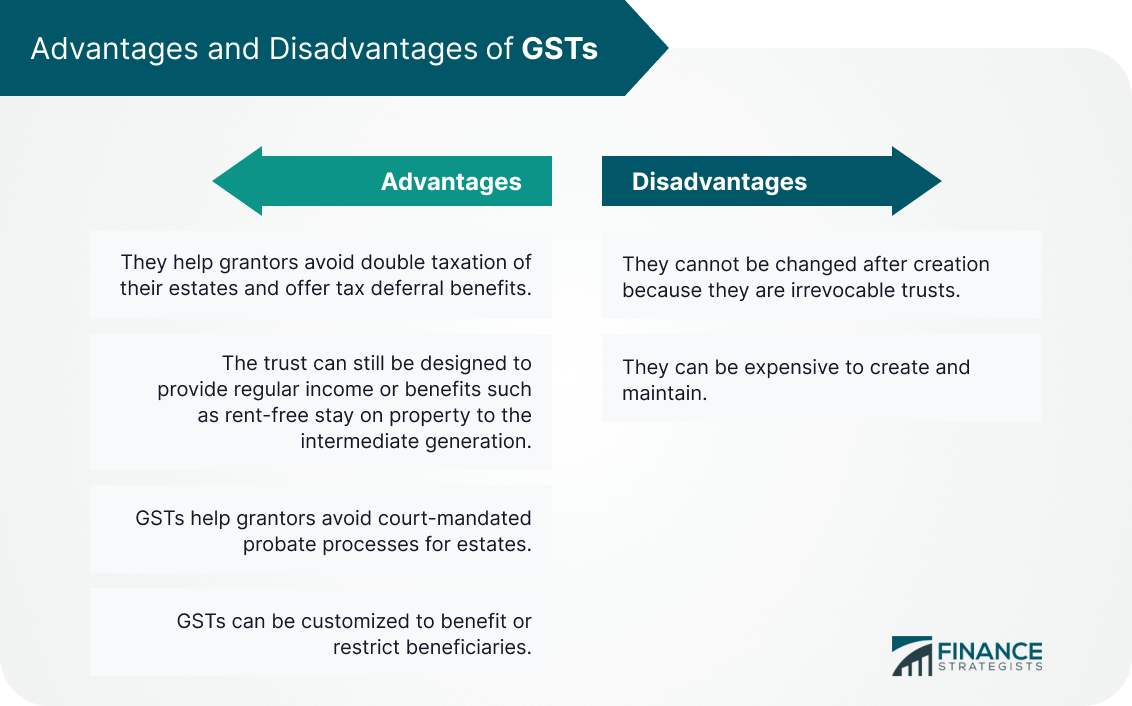

Generation-skipping trusts (GSTs) are irrevocable trusts designed for beneficiaries who are, at least, 37.5 years younger than the grantor and may or may not be related to them. GSTs are used by high net worth individuals to pass on wealth to their grandchildren and avoid double taxation of their estate. GSTs are subject to taxes known as generation-skipping transfer taxes (GSTTs). The tax rates can run as high as 40% of the total estate. The main advantage of GSTs is tax benefits. They help grantors avoid double taxation. They also offer other benefits of a trust: multiplication of income with tax deferrals and probate avoidance. Have questions about Generation-Skipping Trusts? Click here. Generation-skipping trusts are used by individuals to pass on wealth to their grandchildren or grand nieces or nephews. It is not necessary for beneficiaries to be related to the grantor, however. Any person younger by more than 37.5 years of age than the grantor can be assigned as a beneficiary. GSTs are useful to avoid double taxation of grantor estates. The federal estate tax exemption limit in 2026 is $15 million (up from $13.99 million in 2025), meaning all estates below that amount are not required to pay taxes. The estate tax can be a headache for the very wealthy because they end up paying it twice – once when wealth is passed on from beneficiaries to their progeny and again when the same estate is passed onto the beneficiary’s progeny. To avoid double taxation, the grantor can fashion a GST that skips a generation to pass wealth directly to the grandchildren. The grantor will relinquish ownership of the assets contained in the trust. The intermediate beneficiary – the grantor’s children – is not liable for taxes from the estate because they do not own the assets. The final beneficiary owns the assets and pays taxes on it when they inherit it from the trust. Therefore, the estate tax is paid only once across three generations. The U.S. Congress created the Generation-Skipping Transfer Tax in 1986 with an exemption of $1 million in 1986. Estates that were above the exemption limit were liable for taxes. The exemption limit has increased and decreased with subsequent administrations. For example, under the Clinton administration, it was indexed to inflation for the first time and resulted in increments of $10,000. The 2026 federal tax exemption limit is $15 million, meaning all estates that are below this amount are not liable for taxes. Estates above that amount are taxed at the top rate of 40%. Generation skipping trusts are similar to dynasty trusts in that both are instruments to pass on wealth between generations. Both also provide significant tax benefits because they help grantors avoid estate taxes. Generation skipping trusts, however, are limited in their tenure and allow for passage of wealth only a generation apart. For example, a grantor can only pass on wealth to a person or relative who is 37.5 years younger than her. In contrast, dynasty trusts enable passage of wealth between multiple generations. For example, the grantor can pass on wealth to an immediate beneficiary who can, then, pass on wealth to their offspring. Before you begin with the process to create a GST, it is important to note that it is a complicated one. It is a wise idea to seek out legal help to create a watertight trust. The process to create a generation skipping trust is similar to that of a regular trust. While GSTs are designed to skip a generation, they can still provide benefits and regular income to the skipped generation through judicious use of special powers of appointment. You can also customize GSTs. For example, you can insert provisions that allow the intermediate beneficiary to control distribution of the trust’s income to themselves. You can also insert conditions to restrict spending in the case of profligate beneficiaries. The advantages of GSTs are as follows: The disadvantages of GSTs are as follows: ‘Basics of Generation-Skipping Trusts

GST and Taxes

GSTs and Dynasty Trusts

How to Create a GST

Advantages and Disadvantages of GSTs

Generation-Skipping Trusts FAQs

Generation-skipping trusts (GSTs) are irrevocable trusts designed for beneficiaries who are, at least 37.5 years younger than the grantor and may or may not be related to them.

The main advantage of a GST is that it helps avoid double taxation of estates. Besides this, they also help avoid probate and can be customized.

Generation-skipping trusts are designed to skip a generation i.e., the actual beneficiaries are the second generation from the grantor.

The grantor will relinquish ownership of the assets contained in the trust. The intermediate beneficiary – the grantor’s children – is not liable for taxes from the estate because they do not own the assets. The final beneficiary owns the assets and pays taxes on it when they inherit it from the trust. Therefore, the estate tax is paid only once across three generations.

The 2026 federal tax exemption limit is $15 million (up from $13.99 million in 2025), meaning all estates that are below this amount are not liable for taxes. Estates above that amount are taxed at the top rate of 40%.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.