A grantor trust is a term used to describe any trust in which the grantor or the creator of the trust maintains ownership, authority, and control over the trust's assets or income. In a grantor trust, the grantor retains the right to choose who receives income, to vote or influence the vote on shares held by the trust, to supervise the investment of trust funds, and to terminate the trust. Due to the grantor's continued ownership and authority, the income and assets of the trust are subject to the grantor's individual tax rate, which is often lower than trust tax rates.

Grantor trusts operate according to the rules set by the Internal Revenue Service (IRS). Trusts established by a grantor may be revocable or irrevocable. The grantor may make modifications to the trust and its assets. Beneficiaries may be added or changed also. The grantor is allowed to name a successor trustee(s) to take over the administration of the trust in the event they become unable to do so due to mental incapacity or other reasons. They will remain responsible for any taxes due on the trust. A grantor trust may be suitable when the grantor wants to transfer assets to their children but wishes to keep control over these assets and the tax liability during their lifetime. This type of trust operates by giving the grantor discretion over the administration and distribution of the trust's assets. Below is a list of the various types of grantor trusts: The simplest type of grantor trust is a revocable living trust. It is created during the grantor's lifetime and can be terminated or amended at any time by the grantor. The grantor is typically also the trustee, meaning they have control over how the trust's assets are managed and distributed. This trust is frequently used by people to avoid probate, which may be costly and time-consuming. Revocable trusts do not shield your assets from creditors as they are subject to revision or termination at any time. A GRAT is a type of irrevocable trust used to minimize estate taxes. Assets are transferred to the trust by the grantor. The grantor retains the right to receive an annuity, or fixed payments, for a set period of time. Once the term ends, the remaining assets are distributed to the beneficiaries free of estate taxes. A QPRT is an estate planning method that allows the grantor to transfer their primary residence or vacation home to the trust. The grantor can exclude the value of the residence from their tax liabilities. This is particularly advantageous if the grantor has a luxurious estate that they want to transfer to future generations or their beneficiaries. Certain requirements must be met in order to qualify for the transfer tax savings, which are covered under IRC 2702 and related laws. An intentionally defective grantor trust is a type of estate planning that can benefit wealthy clients. The trust is treated as separate from the grantor when it comes to federal estate and gift taxes, but it is still treated like the grantor owns it for federal income tax purposes. It allows the trust's grantor to pay the income taxes on the trust's assets while still enabling the transferred assets to grow free of estate taxes and without being constrained by income taxes. There are numerous benefits to a grantor trust. When a creditor wins a judgment against you, they will not be able to seize the assets included in the trust because you are not the owner of those assets. A disadvantage of creating grantor trusts is the possible income tax issues. Creating a grantor trust presupposes you have the financial means to cover income taxes on trust assets while you are still alive. If the trust asset's value considerably rises, you can experience issues filing your taxes if you do not have enough cash on hand. The regulations governing grantor trusts may also be subject to change. While trusts founded before the enactment of the new law would be protected from the change, any assets subsequently transferred would be incorporated in the grantor's taxable estate. The Internal Revenue Code sections 671 through 679 outline the grantor trust rules. These sections describe how these trusts should operate. The power of the grantor is defined in these rules. The grantor trust rules explain how the trust should function. Specifications on how the trust's assets will be administered following the grantor's death are also indicated. Some grantor trust rules enumerated by the IRS are listed below: The grantor of the trust is responsible for declaring the trust's revenue in his own income. It is necessary to file Form 1041, U.S. Income Tax Form for Estates and Trusts. The grantor must mark the checkbox on the form indicating that the trust is a grantor-type trust. This informs the IRS that the grantor is including the trust's revenue on his personal tax return. Someone who wants to preserve wealth and minimize tax might consider a grantor trust. Additionally, an individual who wants to protect his or her assets against legal actions from creditors can also benefit from this. Grantor trust can be helpful for individuals who are considering transferring assets over a long period. Having a grantor trust might make sense for those who want to avoid the probate procedure. Even though some grantor trusts are irrevocable trusts, a grantor trust differs from an irrevocable trust in the sense that it is disregarded as a tax entity. Given this status, all taxable income earned by the grantor during their lifetime—or at least until the trust's assets are returned to the beneficiaries—is attributable to them. The major distinctions between a grantor trust and an irrevocable trust are listed below. A grantor trust is a type of trust in which the person who created the trust retains ownership of the trust's assets and property. The IRS grantor trust rules dictate how grantor trusts should be operated. Rules on beneficiary designations, what can be done with the income, and who can borrow are outlined in the IRS rules. There are several types of grantor trusts, such as revocable living trusts, grantor retained annuity trusts and others. A grantor trust can offer many advantages over other types of trusts, but there are also some disadvantages to keep in mind. Grantor trusts can be helpful for individuals who want to minimize taxes and preserve wealth. However, grantor trusts also come with the responsibility of paying taxes on the trust assets. A financial advisor can help weigh options before deciding if a grantor trust is suitable for an individual’s needs.What Is a Grantor Trust?

How Does a Grantor Trust Work?

Types of Grantor Trust

Revocable Living Trust

Grantor Retained Annuity Trust (GRAT)

Qualified Personal Residence Trust (QPRT)

Intentionally Defective Grantor Trust (IDGT)

Advantages of Grantor Trust

As the grantor is paying taxes on the trust's income, it enables the trust's assets to grow tax-free.Disadvantages of Grantor Trust

Grantor Trust Rules

Grantor Trust Filing Requirements

Who Needs a Grantor Trust?

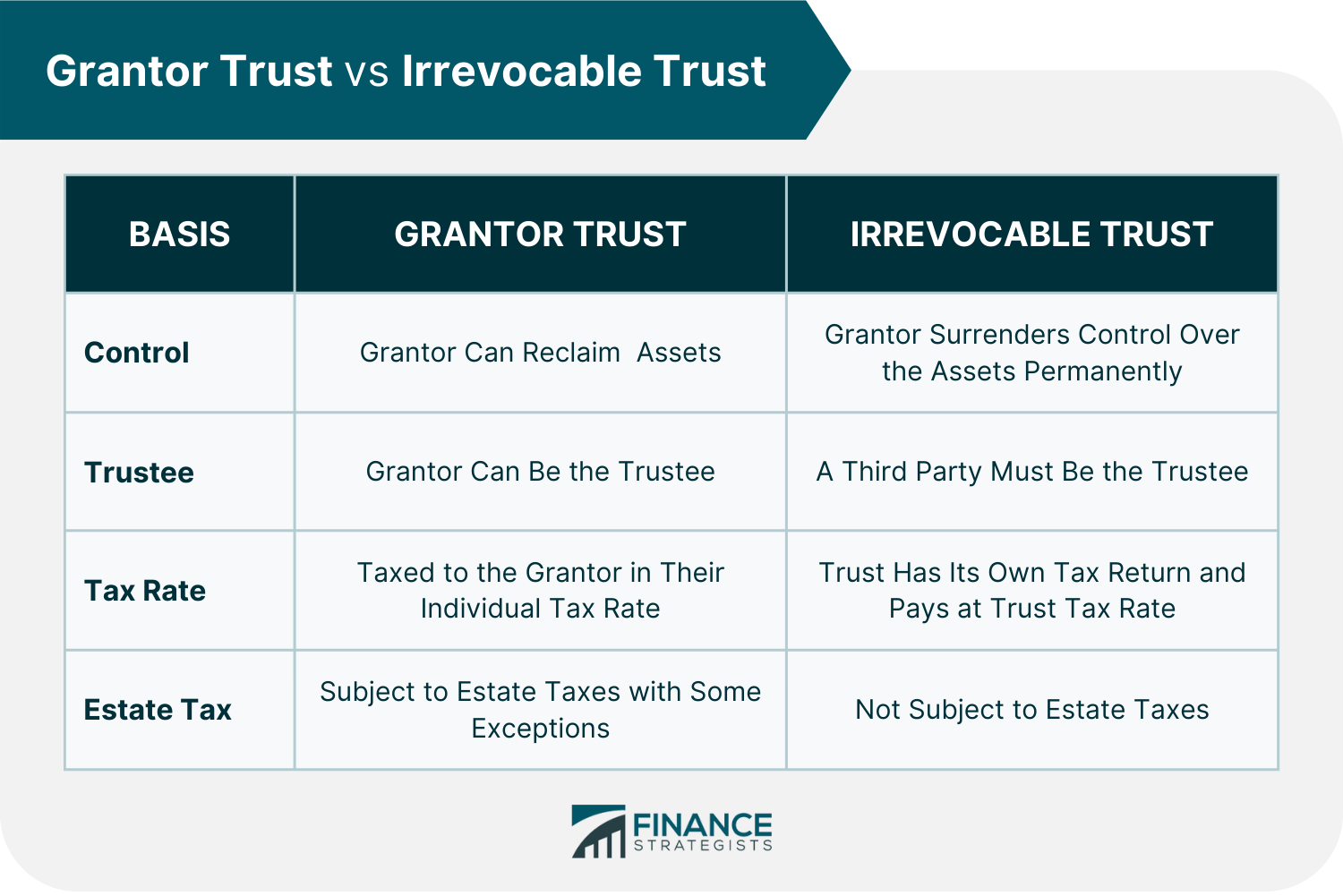

Grantor Trust vs Irrevocable Trust

The Bottom Line

Grantor Trust FAQs

A grantor trust is a kind of trust in which the trust creator or the grantor retains ownership of the trust's assets and property.

The person who created the trust or the grantor controls a grantor trust. The grantor can make modifications to the trust at any time and has the power to revoke the trust.

A grantor is the one who creates and finances a trust. A trust is a legal arrangement used in estate planning to transfer the grantor's property and funds after death. Moreover, trusts can be established to manage assets during a person's lifetime.

The grantor is recognized as the owner of the assets. The trust is not considered an independent tax entity; therefore, all income is taxable to the grantor.

The purpose of a grantor trust is to enable the grantor to safeguard the wealth he or she has acquired in a trust that offers asset protection for the beneficiaries, lowers the beneficiaries' eventual tax burden, and removes the assets from the grantor's taxable estate after death.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.