Retirement income tax withholding refers to the process of deducting taxes from retirement income payments upfront. When individuals receive retirement income, such as pensions, annuities, or distributions from 401(k)s or individual retirement accounts (IRAs), taxes may be withheld by the payer or the financial institution responsible for distributing the funds. The purpose of retirement income tax withholding is to ensure that individuals meet their tax obligations to the government. By withholding a portion of the retirement income upfront, the payer helps the recipient satisfy their tax liability, making it more convenient and efficient for individuals to pay their taxes. It's important to note that retirement income tax withholding is not the final tax liability. It serves as an estimate or prepayment of taxes, and the actual tax liability is determined when the individual files their annual income tax return. If too much tax is withheld, the individual may receive a refund, and if too little is withheld, they may owe additional taxes. For instance, distributions from 401(k) plans and IRAs are typically taxed as ordinary income. On the other hand, Roth 401(k) and Roth IRA distributions are generally tax-free, provided certain conditions are met. Pensions and annuities are often taxable but may also have a portion that is considered a return of after-tax contributions, which is not taxed. Your total income also affects your tax rate. This includes not only your retirement income but any other income you have as well, such as income from a job, rental income, investment income, Social Security benefits, etc. The more income you have, the higher your tax bracket may be, which means more tax could be withheld. The five filing statuses are single, married filing jointly, married filing separately, head of household, or qualifying widow(er) with a dependent child. Each of these statuses corresponds to different tax brackets, with different income levels needed to reach higher tax rates. For instance, a single filer will generally reach a higher tax bracket with less income than someone who is married and filing jointly. This, in turn, impacts the amount of tax that needs to be withheld from your retirement income. Prior to 2020, you could claim allowances on your W-4 to adjust your tax withholding. Each allowance you claimed reduced the amount of money that would be withheld for taxes. However, the IRS redesigned the W-4 form in 2020, and it no longer uses allowances. Instead, the new form asks for specific dollar amounts for things like income tax credits, non-wage income, itemized and other deductions, and total annual taxable wages. If you live in a state that has an income tax, you may need to have state income tax withheld from your retirement income as well. The rate at which this is done depends on your state's tax laws. For some types of income, your age may affect how much tax is withheld. For example, if you take distributions from a traditional IRA before age 59½, you may be subject to an additional 10% early withdrawal penalty. Social Security benefits serve as a primary source of income for many retirees. These benefits are generally based on an individual's work history and are paid out monthly. While some recipients may not owe taxes on their Social Security benefits, others may have to pay taxes on a portion of their benefits, depending on their income and filing status. Pensions typically come from defined benefit plans provided by employers. Similarly, annuities are contracts purchased from insurance companies that guarantee a stream of income for a specified period or for life. Both pension and annuity payments may be subject to income tax withholding. Contributions to these accounts are made pre-tax, and taxes are deferred until funds are withdrawn during retirement. Withdrawals, including required minimum distributions (RMDs), are generally subject to income tax withholding. Roth IRAs and Roth 401(k)s are retirement savings accounts that offer tax-free growth and withdrawals. Unlike traditional IRAs and 401(k)s, contributions to these accounts are made with after-tax dollars. Qualified distributions from Roth accounts are tax-free, while non-qualified distributions may be subject to taxes and penalties. Investment income is another potential source of retirement income, which can include interest, dividends, and capital gains from stocks, bonds, and other investment vehicles. The taxation of investment income varies depending on the type of income and the individual's overall financial situation. Some retirees may choose to continue working part-time or engage in self-employment activities to supplement their retirement income. This income is subject to income tax withholding and may require retirees to make estimated tax payments on a quarterly basis. You will need to consider your total income, the standard or itemized deductions you qualify for, and any tax credits that might apply to you. It's important to be as accurate as possible in estimating your tax liability to avoid underpaying or overpaying. Underpaying taxes could result in a large unexpected bill at tax time while overpaying means you're unnecessarily tying up funds that could be used elsewhere. Your financial situation and tax laws can change from year to year. As such, it's crucial to review your tax withholding regularly and make adjustments as needed. Factors such as changes in your total income, new tax laws, or personal life change like marriage, or the death of a spouse can all necessitate adjustments to your tax withholding. Early withdrawals from retirement accounts like 401(k)s and IRAs before the age of 59 ½ are usually subject to an additional 10% penalty on top of the regular income tax. This can significantly increase your tax liability. Therefore, it's best to avoid early withdrawals if possible and consider other sources of funds if you need money before reaching the age of 59 ½. Social Security benefits and certain other types of retirement income allow for voluntary tax withholding. This means you can choose to have a certain percentage of your benefit withheld for taxes. Opting for voluntary withholding can help manage your tax bill by spreading out the payments over the year, preventing a large tax bill at the end of the year. If you have income that's not subject to withholding, such as from self-employment or investments, you may need to make quarterly estimated tax payments. You will need to balance these payments with your other tax withholdings to ensure you're not underpaying or overpaying taxes. Tax planning can be a complex process, especially when dealing with multiple income streams. A tax professional or a financial advisor can help you navigate this complexity. They have the knowledge and experience to understand how different types of income are taxed and can help you optimize your tax situation. They can also stay updated on any changes in tax laws and advise you accordingly. Retirement income tax withholding streamlines the tax payment process and facilitates efficient compliance by deducting taxes upfront. However, it's crucial to understand that it is only an estimate or prepayment, with the actual tax liability determined during the annual income tax return filing. Several factors influence retirement income tax withholding, including the type of retirement income, total income, filing status, number of allowances, state of residence, and age. These factors impact the tax rate and the amount of tax to be withheld from retirement income sources such as Social Security benefits, pension and annuity payments, traditional and Roth IRAs, investment income, and part-time work or self-employment income. To ensure proper tax withholding, individuals should accurately estimate their tax liability, regularly monitor and adjust their withholding based on changes in financial situations and tax laws, and avoid early withdrawals from retirement accounts to prevent penalties and higher tax liabilities. Seeking professional guidance from tax professionals or financial advisors can provide valuable assistance in navigating the complexities of tax planning, optimizing tax situations, and staying updated on tax law changes. What Is Retirement Income Tax Withholding?

Factors Affecting Retirement Income Tax Withholding

Retirement Income Type

Total Income

Filing Status

Number of Allowances

State of Residence

Age

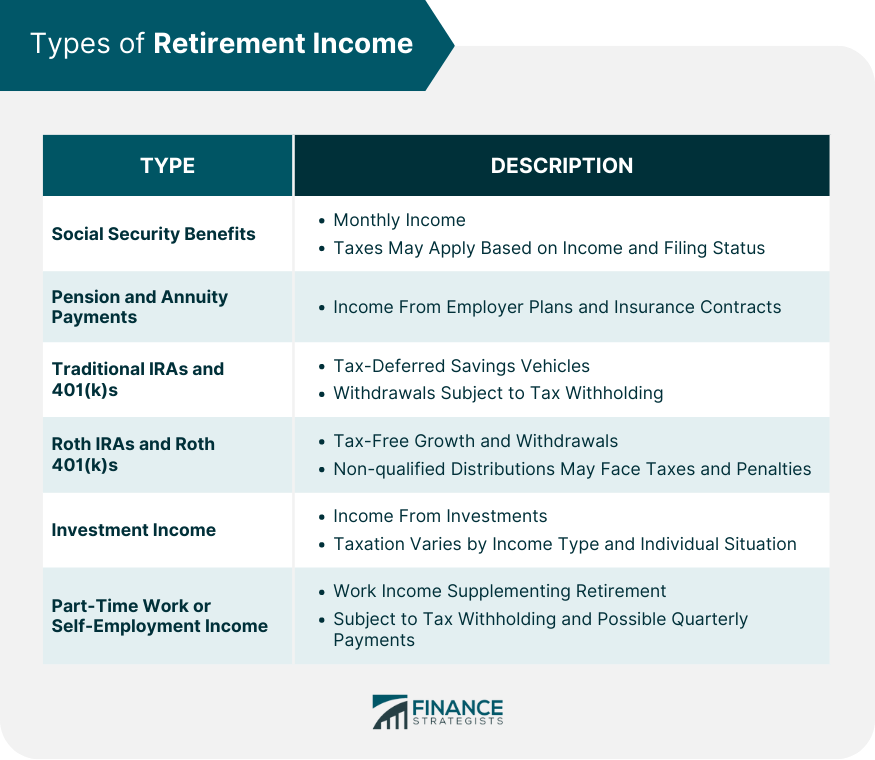

Types of Retirement Income

Social Security Benefits

Pension and Annuity Payments

Traditional IRAs and 401(k)s

Roth IRAs and Roth 401(k)s

Investment Income

Part-Time Work or Self-Employment Income

Best Practices for Retirement Income Tax Withholding

Estimate Tax Liability

Monitor and Adjust Withholding

Avoid Early Withdrawals

Opt for Voluntary Withholding

Balance Withholdings and Quarterly Payments

Consider Professional Guidance

Final Thoughts

Retirement Income Tax Withholding FAQs

Retirement income tax withholding is the process of deducting federal and state income taxes from various sources of retirement income, such as Social Security benefits, pensions, and IRAs. Retirees need to understand tax withholding to effectively manage their financial obligations and avoid potential penalties for under-withholding.

Retirement income tax withholding on Social Security benefits is voluntary, and recipients can request withholding by completing IRS Form W-4V. This form allows retirees to choose a specific percentage (7%, 10%, 12%, or 22%) to be withheld from their monthly payments.

Yes, pension and annuity payments are generally subject to retirement income tax withholding. Retirees can provide withholding instructions by completing IRS Form W-4P, which allows them to choose a fixed-dollar amount or a percentage to be withheld from each payment.

Withdrawals from traditional IRAs and 401(k)s, including required minimum distributions (RMDs), are generally subject to retirement income tax withholding. Unless a retiree provides specific withholding instructions, the payer must withhold 10% of the distribution amount for federal income taxes.

Retirees may need to adjust their retirement income tax withholding in response to changes in income, filing status, or significant life events such as marriage, the birth of a child, or retirement. Adjusting tax withholding can help retirees avoid under-withholding penalties and ensure they pay their taxes effectively throughout the year.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.