Avoiding capital gains tax on a second home involves strategic planning. One method is converting your second home into your primary residence. By living in the home for at least two out of five years prior to selling, you can qualify for an exclusion on capital gains tax—up to $250,000 for individuals and $500,000 for couples. Another strategy is a 1031 exchange, which allows you to defer capital gains tax by reinvesting the proceeds of the sale into a similar property. Gifting or inheriting property can also result in a step-up in basis, reducing or eliminating capital gains tax. Each strategy has its nuances, so consult a tax professional to understand the best approach for your situation. The first thing to remember is that capital gains tax is only applicable when you sell a property for more than its cost basis. If you sell your second home at a loss, there won't be any capital gains tax. The IRS provides some special exemptions under specific circumstances. If you had to sell your second home due to health-related reasons, a change in place of employment, or other unforeseen circumstances, you might be eligible for an exclusion. Gifting or inheriting a property can have distinct capital gains tax implications. The recipient of a gift inherits the donor's cost basis, while inherited property receives a step-up in basis to the fair market value at the time of the owner's death. One of the best strategies to avoid capital gains tax on a second home is to turn it into your primary residence. The IRS provides an exclusion on capital gains tax for the sale of a primary residence—up to $250,000 for single filers and $500,000 for joint filers. To qualify, you must have owned the home and used it as your main residence for at least two of the five years before selling. The capital gains tax exclusion for a primary residence is a powerful tool to avoid taxes. When you sell your primary home, a portion of the profit is excluded from taxable income. As mentioned earlier, if you're a single taxpayer, you can exclude up to $250,000 of gain. Married taxpayers who file jointly can exclude up to $500,000. It's essential, however, to meet the ownership and use tests set by the IRS to avail of this benefit. The IRS allows homeowners to convert a second home into a primary residence to take advantage of the capital gains tax exclusion. However, this requires living in the second home as your main residence for at least two years before selling. You'll need to show proof, such as changing your address on important documents, registering to vote in the new location, and other actions that demonstrate this home is your primary residence. Section 1031 of the Internal Revenue Code allows property owners to defer paying capital gains taxes if they reinvest the proceeds of the sale into a similar type of property in a specified period. These so-called "like-kind exchanges" or "1031 exchanges" can be an effective way to avoid capital gains tax on a second home, but they come with strict rules and timelines that must be followed. Another strategy to avoid capital gains tax on a second home is through gifting or inheritance. When a property is gifted, the recipient inherits the donor's basis. When the property is later sold, capital gains tax is due on the difference between the selling price and the donor's basis. In contrast, an inherited property gets a step-up in basis, which means the new basis is the fair market value of the property at the time of the owner's death. This can significantly reduce or eliminate any potential capital gains tax when the property is sold. Tax-loss harvesting involves selling investments that have lost value to offset capital gains on other investments. If you have other capital assets that have declined in value, you may sell these to offset the capital gain on your second home. This strategy can be particularly useful in years when you have high capital gains, such as when you sell a second home. The laws and regulations surrounding capital gains tax on a second home are complex. For this reason, it's recommended to consult with a tax professional or a financial advisor who understands these rules. They can provide personalized advice based on your circumstances and help you devise a tax plan that minimizes your capital gains tax obligation. There are several tax-advantaged investment strategies that you can use to mitigate capital gains tax. These include investing in tax-deferred retirement accounts, such as 401(k)s or IRAs, or using 529 plans or Health Savings Accounts (HSAs) that offer tax-free growth. Investing in tax-advantaged accounts can help offset the impact of capital gains tax on your second home sale. Creating a comprehensive tax plan involves understanding your overall tax situation and planning strategies to minimize your tax liability. A tax plan might involve combining the earlier strategies, such as converting a second home into a primary residence, using tax-loss harvesting, or investing in tax-advantaged accounts. It also involves staying informed about tax law changes that could impact your situation. It's important to understand the difference between tax evasion and tax avoidance. Tax avoidance involves using legal strategies to minimize your tax bill, such as those discussed in this article. On the other hand, tax evasion involves illegal activities to avoid taxes, such as underreporting income or inflating deductions. While it's smart to avoid unnecessary taxes legally, evading taxes can lead to severe penalties. Engaging in improper tax avoidance or tax evasion can lead to serious consequences, including financial penalties and possible criminal charges. These penalties can far outweigh any tax savings. Therefore, it's essential to ensure any tax strategy you use to avoid capital gains tax on your second home is legal and correctly implemented. Understanding capital gains tax on a second home encompasses a variety of approaches, from turning the property into a primary residence to engaging in a 1031 exchange or even capitalizing on the gift and inheritance rules. Exceptional circumstances can also influence tax obligations, and understanding these can significantly impact your financial planning. Professional consultation is advised to navigate the complex rules surrounding capital gains tax and to formulate a comprehensive tax plan that fits your situation. It's crucial to recognize the line between legal tax avoidance and illegal tax evasion, understanding that the latter can lead to severe consequences. In essence, mitigating capital gains tax on a second home requires strategic, informed planning, and a keen awareness of the laws and regulations in place.How to Avoid Capital Gains Tax on a Second Home: Overview

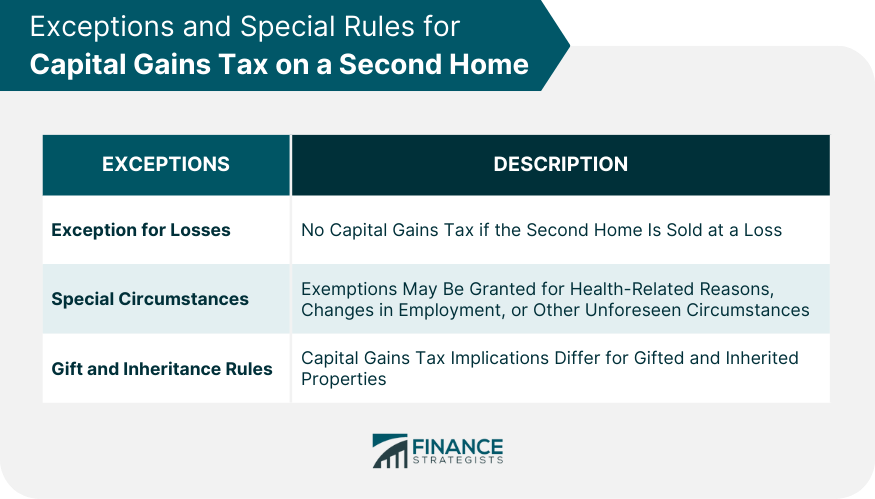

Exceptions and Special Rules for Capital Gains Tax on a Second Home

Exception for Losses

Special Circumstances

Gift and Inheritance Rules

Strategies to Avoid Capital Gains Tax on a Second Home

Use Home as a Primary Residence

Capital Gains Tax Exclusion for Primary Residence

Convert a Second Home Into a Primary Residence

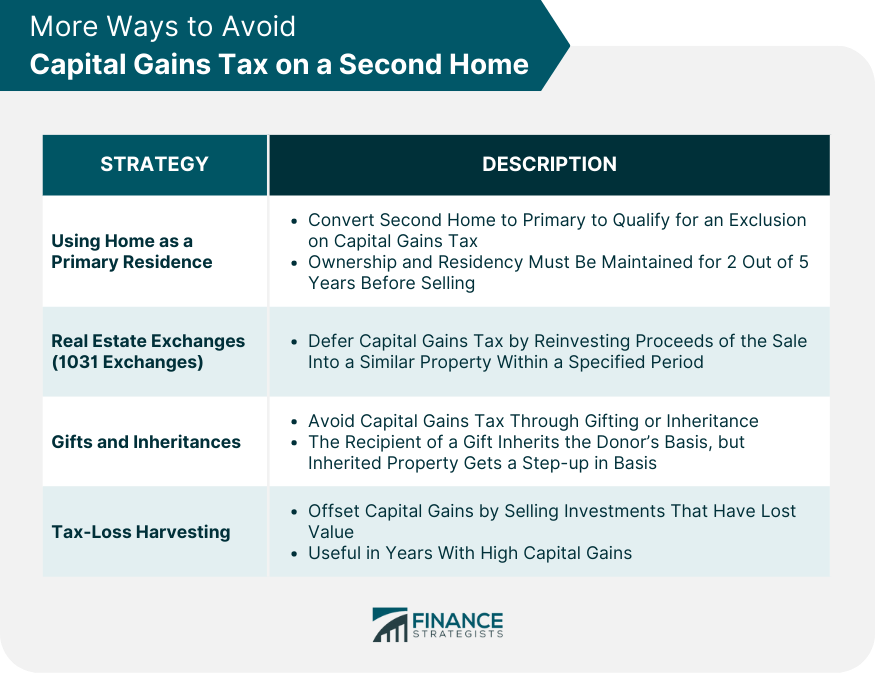

More Ways to Avoid Capital Gains Tax on a Second Home

Real Estate Exchanges (1031 Exchanges)

Gifts and Inheritances

Tax-Loss Harvesting

Role of Tax Planning

Importance of Consultation With a Tax Professional

Tax-Advantaged Investment Strategies

Creating a Comprehensive Tax Plan

Legal Implications of Avoiding Capital Gains Tax on a Second Home

Understand Tax Evasion vs Tax Avoidance

Potential Legal Consequences of Improper Tax Avoidance

Conclusion

How to Avoid Capital Gains Tax on a Second Home FAQs

The capital gains tax on a second home is the tax applied to the profit made from selling the property, which is the difference between the selling price and the purchase price plus any improvements made to the property. The tax rate can vary depending on your income bracket and how long you've owned the property.

Yes, you can avoid capital gains tax on a second home by converting it into your primary residence. You must live in the home as your primary residence for at least two of the five years before selling it to be eligible for the tax exclusion.

A 1031 exchange, also known as a like-kind exchange, allows you to defer capital gains tax on a second home by reinvesting the proceeds of the sale into a similar property. The new property must be identified within 45 days of selling the old property, and the purchase must be completed within 180 days.

Yes, inheriting a second home can help avoid capital gains tax because of a rule known as "step-up in basis". This rule adjusts the value of the home to its fair market value at the time of the original owner's death, potentially reducing the taxable capital gain when the home is sold.

Improperly avoiding capital gains tax on a second home can result in financial penalties and even criminal charges. This includes underreporting income or inflating deductions. It's always advisable to consult with a tax professional to ensure that all strategies used to reduce or avoid taxes are legal and correctly implemented.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.