In real estate, capital gains represent the increased value of a property over its original purchase price or adjusted basis. Essentially, it's the difference between the selling price and the purchase price. For example, if a home bought for $200,000 is sold for $300,000, the capital gain is $100,000. These gains form the basis for taxation and significantly influence investment decisions, particularly when considering selling a property. Whether the gain is categorized as short-term or long-term depends on the property holding duration. If held for a year or less, the gains are short-term and taxed at the regular income tax rate. However, if the property is held for over a year, the gains are long-term, usually taxed at a more favorable rate. This distinction is crucial in tax planning as informed selling decisions can greatly affect tax liabilities. Not all home expenses increase the property's adjusted basis. Routine maintenance and repairs, like painting or fixing a leak, don’t count. However, substantial improvements, like building an additional room or renovating the kitchen, can be added to the basis, reducing the overall capital gain when selling. These significant improvements not only elevate the value and appeal of the property but also offer tax benefits. For rental properties, depreciation offers tax benefits during ownership. However, when selling, the IRS requires a "recapture" of the depreciation deducted, which is then taxed at a specific rate. This means that while depreciation can provide yearly tax relief, it can also increase your tax bill when selling the property. Many investors are caught off guard by this, especially if they've heavily relied on depreciation to reduce taxable income during ownership. One of the significant benefits for homeowners is the primary residence exemption. If you've lived in your home for at least two of the last five years, you might be eligible to exclude up to $250,000 of the capital gain from taxes (or $500,000 if married filing jointly). This can lead to substantial tax savings, especially for homeowners in fast-appreciating areas. To capitalize on this, homeowners should be mindful of the time they live in the property, ensuring they meet the minimum residency requirements. Achieving "real estate professional" status in the eyes of the IRS can provide notable tax benefits, especially for those heavily involved in property ventures. This designation allows individuals to deduct rental property losses and other specific advantages that aren't available to the average investor. However, obtaining this status involves meeting stringent IRS criteria, including the number of hours spent on real estate activities. Named after Section 1031 of the U.S. tax code, this strategy allows real estate investors to defer paying capital gains taxes. By reinvesting proceeds from a property sale into another "like-kind" property, the capital gains tax can be postponed. However, there are stringent rules and timelines to abide by, so careful planning is essential. Furthermore, choosing the right "like-kind" property and ensuring all the procedural steps are correctly executed is critical for the successful execution of a 1031 exchange. Transforming an investment property into your primary home can allow you to leverage the primary residence exemption when you sell. However, the exemption will only apply to the years the property was used as a primary residence, and not when it was an investment. So, the timeline of occupancy versus rental can greatly influence the potential tax savings. This strategy involves selling a property at a loss to offset gains from another property sale. For instance, if you have a $50,000 gain from one property sale but a $20,000 loss from another, you only pay capital gains tax on the net gain of $30,000. Regularly assessing your property portfolio and being proactive in offsetting gains can be a significant benefit of tax-loss harvesting. Documentation is pivotal. Keeping detailed records of home improvements, purchase-related costs, and other expenses can reduce your capital gain when you sell. Such records help ensure you take advantage of every eligible deduction. Regularly updating and organizing these records can streamline the selling process and help you swiftly address any inquiries from the IRS. Many believe that every property sale automatically results in a taxable event. However, as mentioned earlier, there are exclusions like the primary residence exemption. Plus, capital losses from one sale can offset gains from another. Knowledge of these nuances can empower homeowners and investors to make more informed decisions and possibly avoid unexpected tax bills. Different properties can attract different tax rates. While primary residences might benefit from exclusions, rental properties can be subject to depreciation recapture. The type of property, its use, and how long it's been held can all influence the applicable tax rate. Thus, being cognizant of the varying tax implications based on property type can be crucial for tax planning. While the 1031 exchange allows for tax deferral, it doesn't apply to primary residences and has specific rules. Simply buying another property doesn't mean you can avoid the capital gains tax. Many individuals mistakenly believe this blanket rule applies, often leading to surprise tax obligations. Navigating capital gains tax in real estate can be complex, yet essential for investment strategies and financial planning. Factors like the holding duration, significant property improvements, depreciation recapture, and specific tax exclusions or exemptions can all influence the ultimate tax bill. Strategies like the 1031 Exchange, converting an investment property into a primary residence, and tax-loss harvesting can offer opportunities to reduce or defer capital gains tax. Furthermore, understanding common misconceptions can prevent costly mistakes and unexpected tax liabilities. It's crucial for homeowners and real estate investors to stay informed about these factors and strategies, and when necessary, seek professional advice. To proactively manage and optimize your tax liabilities, consider investing in expert tax planning services. Explore the benefits of professional guidance today, ensuring your real estate decisions align with your broader financial goals.Understanding Capital Gains Tax on Real Estate

Factors Influencing Capital Gains in Real Estate

Improvements and Their Effects

Depreciation Recapture

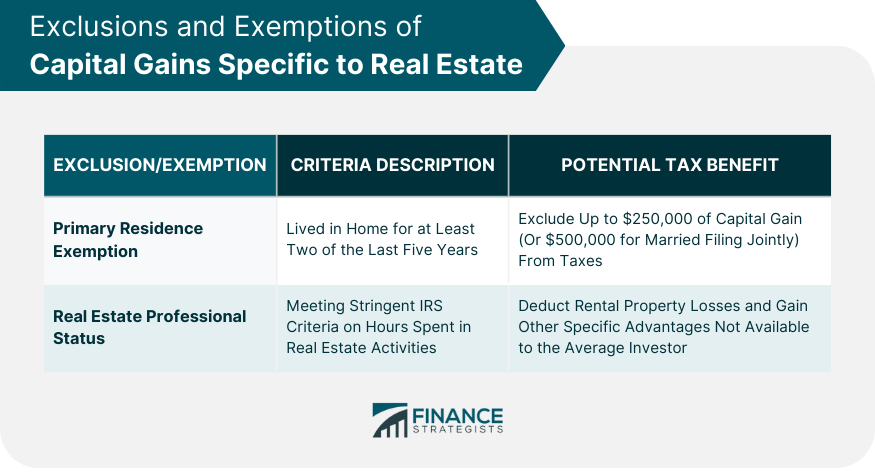

Exclusions and Exemptions of Capital Gains Specific to Real Estate

Primary Residence Exemption

Real Estate Professional Status

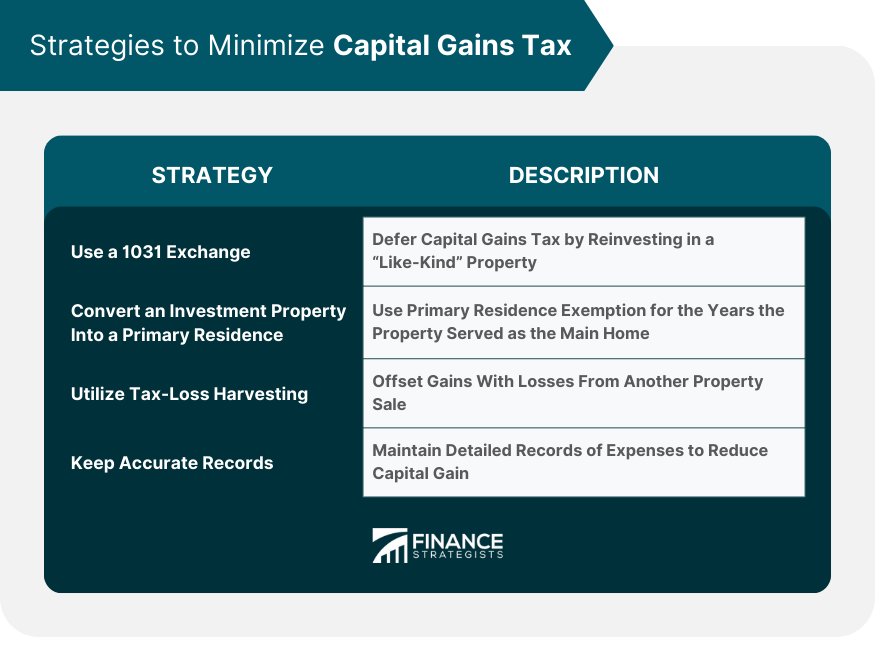

Strategies to Minimize Capital Gains Tax

Use a 1031 Exchange

Convert an Investment Property Into a Primary Residence

Utilize Tax-Loss Harvesting

Keep Accurate Records

Common Misconceptions About Capital Gains Tax in Real Estate

Every Property Sale Results in a Capital Gains Tax

Tax Rate Is the Same for All Types of Properties

You Can Always Avoid Capital Gains Tax by Buying a New Property

Bottom Line

Capital Gains Tax on Real Estate FAQs

It's a tax levied on the profit made from selling property, calculated by subtracting the purchase price from the selling price.

Short-term gains (property held for a year or less) are taxed at regular income rates, while long-term gains (held for more than a year) often have favorable tax rates.

Yes, a primary example is the primary residence exemption, which allows some homeowners to exclude a portion of their capital gain from taxes.

A 1031 exchange lets investors defer capital gains tax by reinvesting sale proceeds into another "like-kind" property, following specific rules.

Yes, such as believing every property sale incurs capital gains tax or that all property types have the same tax rate.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.