A 403(b) rollover to a 401(k) is a financial strategy wherein you transfer your retirement savings from a 403(b) plan to a 401(k) plan. The 403(b) plan is commonly offered to employees of public schools, certain tax-exempt organizations, and ministers. In contrast, the 401(k) plan is generally provided by private sector employers. The "rollover" refers to the direct transfer of funds from the 403(b) to the 401(k) account without incurring immediate tax consequences. The primary purpose of such a rollover is typically due to a job change or the pursuit of enhanced investment options. It's an essential tool that allows individuals to consolidate their retirement savings, streamline account management, diversify investment options, and potentially lower the associated fees. It's crucial, however, to approach this strategy with care, considering factors like potential tax implications and early withdrawal penalties. To initiate a 403(b) rollover to a 401(k), you first need to confirm that your 401(k) plan accepts such transfers. Then, you'll typically need to contact the 403(b) plan administrator to start the process. They can provide a distribution form, which you'll complete and return. Funds can be transferred either directly or indirectly. A direct rollover, or trustee-to-trustee transfer, is where the funds move from your 403(b) account directly to your 401(k) without you touching the money. An indirect rollover means the funds are sent to you, and you have 60 days to deposit them into your 401(k). In a direct rollover, there are typically no immediate tax consequences because the money remains within a tax-advantaged retirement account. An indirect rollover, on the other hand, can trigger a mandatory 20% withholding for taxes, which you'll have to replace from your pocket to complete the full rollover within the 60-day window. Before moving funds, assess your 401(k) plan's quality. Look at the fees, investment options, and other features. If your 401(k) plan doesn't match up to your 403(b) in these areas, the rollover might not be beneficial. While rollovers are generally non-taxable events, missteps (like missing the 60-day window for indirect rollovers) can trigger unexpected tax liabilities. It's crucial to understand the tax implications fully. If you have an outstanding loan in your 403(b), you'll need to repay it before rolling over, or it will be treated as a taxable distribution. Additionally, if you're 73 or older, you'll need to take your required minimum distribution before conducting a rollover. Before initiating a rollover, thoroughly review your existing plans. Understand the fees, investment options, and potential penalties of each plan. Speak with a financial advisor before making any decisions. They can provide personalized advice based on your unique financial situation and goals. Once you've completed your due diligence and decided to proceed, you can initiate the rollover. If you're transferring directly, coordinate with your plan administrators. For an indirect rollover, remember the 60-day window and mandatory withholding. One significant advantage of rolling a 403(b) into a 401(k) is the potential for a wider range of investment options. While 403(b) plans often limit investment choices primarily to annuities and mutual funds, 401(k) plans can offer a broader array of investments. Moving funds from a 403(b) to a 401(k) also streamlines your retirement savings. It's easier to manage and keep track of one account instead of several, especially when implementing a comprehensive investment strategy. Many 401(k) plans, especially those offered by large employers, often have access to institutional-class funds that offer lower expense ratios than the retail-class funds commonly found in 403(b) plans. If you choose to conduct an indirect rollover and fail to deposit the funds into your 401(k) within 60 days, the IRS can consider the money as a distribution, subjecting it to income taxes and potentially a 10% early withdrawal penalty if you're under 59½ years old. While 403(b) plans allow for withdrawals if you're 55 or older and no longer with your employer, 401(k) plans typically require you to be at least 59½. This could limit your financial flexibility if you retire early. Not all 401(k) plans accept rollovers from 403(b) plans. It's crucial to verify this before initiating the process to avoid unnecessary complications and potential tax liabilities. A 403(b) rollover to a 401(k) allows retirement savers to consolidate their assets and potentially diversify their investment options. While the process generally involves the direct transfer of funds with no immediate tax implications, it's vital to understand the various mechanics, including the initiation process and different transfer mechanisms. Potential advantages of this rollover include a broadened investment scope, a streamlined retirement portfolio, and potentially lower fees. Nevertheless, one must also consider the associated challenges, such as the risk of early withdrawal penalties, limited withdrawal flexibility, and transfer restrictions. Before initiating a rollover, it's crucial to scrutinize both plans' details, understand the tax impact, and consult with a financial advisor. Being mindful of these factors can help ensure a successful transition toward a financially secure retirement.What Is a 403(b) Rollover to 401(k)?

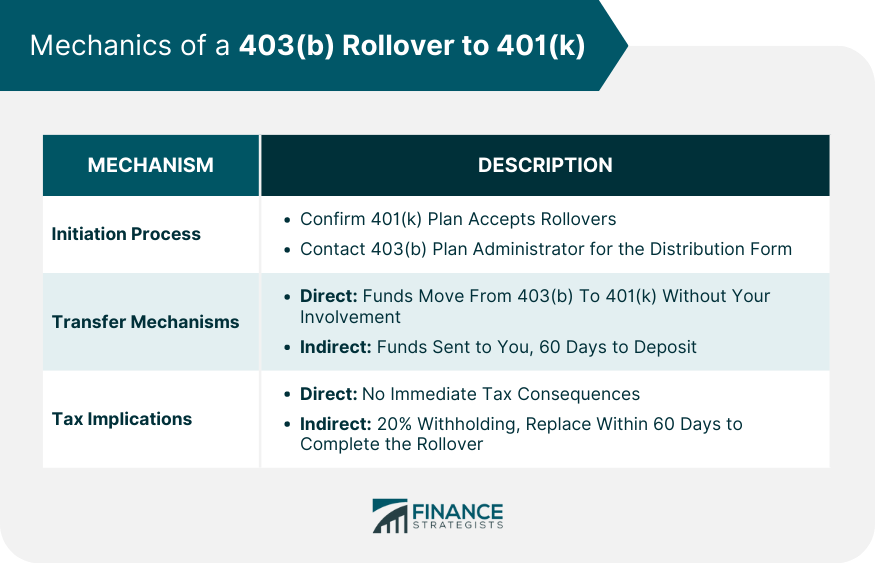

Mechanics of a 403(b) Rollover to 401(k)

Initiation Process

Transfer Mechanisms

Tax Implications

Key Considerations in a 403(b) Rollover to 401(k)

Evaluating the Quality of the 401(k) Plan

Understanding the Tax Impact

Effect on Loans and Required Minimum Distributions

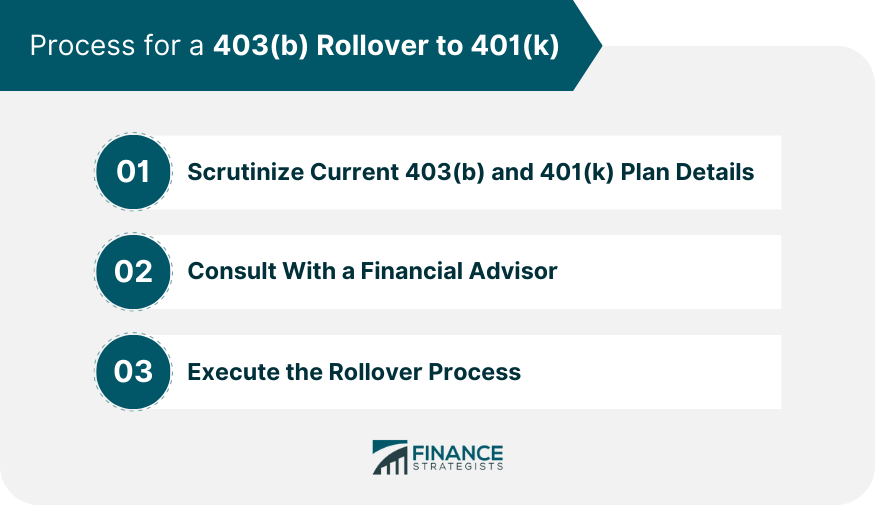

Process for a 403(b) Rollover to 401(k)

Scrutinize Current 403(b) and 401(k) Plan Details

Consult With a Financial Advisor

Execute the Rollover Process

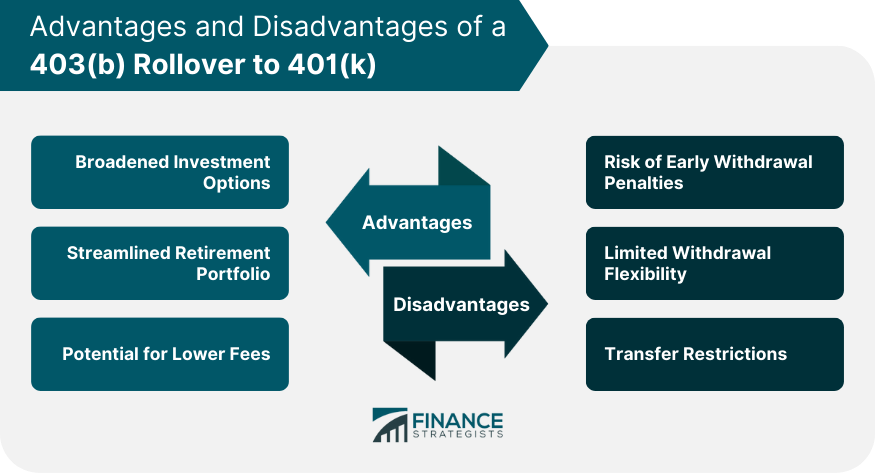

Advantages of a 403(b) Rollover to 401(k)

Broadened Investment Options

Streamlined Retirement Portfolio

Potential for Lower Fees

Disadvantages of a 403(b) Rollover to 401(k)

Risk of Early Withdrawal Penalties

Limited Withdrawal Flexibility

Transfer Restrictions

Conclusion

403(b) Rollover to 401(k) FAQs

Yes, you can, but it depends on whether your current 401(k) plan allows for "in-service" rollovers. Not all plans permit this, so you will need to check with your plan administrator.

Generally, there are no immediate tax consequences when performing a direct rollover because the funds remain within a tax-advantaged account. However, indirect rollovers, where the funds are briefly given to you, trigger a mandatory 20% withholding for taxes, which you'll need to replace if you want to avoid tax penalties.

Early withdrawal penalties generally don't apply to direct rollovers as the funds aren't technically distributed to you. However, if you do an indirect rollover and fail to deposit the funds into your 401(k) within 60 days, it's considered a distribution and may be subject to taxes and a 10% early withdrawal penalty if you're under 59½.

Yes, partial rollovers are allowed. You can choose to roll over a specific amount and leave the rest in your 403(b) plan. It's worth noting that any amount not rolled over may be subject to taxes and penalties, depending on your age and the type of rollover.

In this case, it may not be advantageous to roll over your 403(b) to your 401(k). You should consider other factors, such as fees, ease of management, and your overall financial strategy. Always consult with a financial advisor before making such decisions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.