A withdrawal plan is a financial strategy that enables individuals to access their investments or savings over a specific period, providing them with a steady stream of income during their retirement years or other times of reduced income. This approach helps people to manage their finances effectively by ensuring that they have a reliable source of funds to meet their expenses. A well-designed withdrawal plan is essential for retirees, as it helps them to maintain their desired lifestyle without having to rely solely on social security or other sources of income. By having a withdrawal plan in place, individuals can optimize the use of their accumulated wealth and minimize the risk of outliving their savings. Additionally, a withdrawal plan can provide peace of mind and financial stability during uncertain times. A Systematic Withdrawal Plan (SWP) is a popular method that allows investors to withdraw a fixed amount from their investment portfolio at regular intervals, such as monthly or annually. This approach helps to ensure a steady income stream and can be particularly useful for retirees who want to maintain a consistent lifestyle. Additionally, an SWP can offer the advantage of dollar-cost averaging, which helps to mitigate market volatility and provides a more predictable income. A lump sum withdrawal plan involves taking out a large portion, or the entire amount, of an investment at once. This method can be useful for individuals who require a substantial sum of money for a specific purpose, such as buying a house or starting a business. However, withdrawing a large sum at once may have tax implications and could potentially deplete one's savings quickly, leaving them with insufficient funds to meet future needs. A periodic withdrawal plan is similar to a systematic withdrawal plan but allows for more flexibility in terms of the withdrawal frequency and amount. With a periodic withdrawal plan, individuals can choose to withdraw funds on a semi-annual, annual, or even an ad-hoc basis, depending on their financial needs. This approach can be useful for those who have irregular income patterns or who want greater control over their withdrawals. An ad-hoc withdrawal plan offers the most flexibility, as it allows individuals to withdraw funds from their investment portfolio whenever they need to. This approach can be beneficial for people who have unpredictable expenses or who prefer to maintain full control over their finances. However, ad-hoc withdrawals can make it challenging to budget effectively and may increase the risk of depleting savings too quickly. When developing a withdrawal plan, it is essential to consider one's age and life expectancy. This information can help determine the appropriate withdrawal rate and the length of time the plan should cover. A longer life expectancy requires a more conservative withdrawal strategy to ensure that savings last throughout one's lifetime. Risk appetite plays a crucial role in determining the appropriate withdrawal plan. Individuals with a higher risk tolerance may be comfortable with a more aggressive withdrawal strategy, which could potentially yield higher returns. On the other hand, those with a lower risk appetite might prefer a more conservative approach to ensure financial stability and minimize the risk of outliving their savings. A thorough understanding of one's current financial situation is crucial when creating a withdrawal plan. This includes considering factors such as existing debts, monthly expenses, and other financial commitments. By evaluating these aspects, individuals can determine the amount they need to withdraw and create a plan that meets their specific financial needs. When devising a withdrawal plan, it is essential to keep long-term financial goals in mind. These goals could include purchasing a home, funding a child's education, or traveling during retirement. By aligning the withdrawal plan with these objectives, individuals can ensure that they have the necessary funds to achieve their desired outcomes. Taxes can have a significant impact on the effectiveness of a withdrawal plan. Different types of investments and withdrawal strategies may have varying tax consequences. Therefore, it is vital to understand the tax implications of each withdrawal plan option and choose a strategy that minimizes the overall tax burden. The first step in creating a withdrawal plan is to determine the amount needed to cover living expenses and achieve long-term financial goals. This process may involve creating a detailed budget, factoring in inflation, and considering potential changes in spending patterns during retirement or periods of reduced income. Once the withdrawal amount has been determined, individuals must decide which type of withdrawal plan best suits their needs. This decision will depend on factors such as risk appetite, financial goals, and desired level of control over withdrawals. Each of the withdrawal plan types discussed earlier (SWP, lump sum, periodic, and ad-hoc) offers different benefits and drawbacks, so it is essential to weigh these options carefully. After choosing a withdrawal plan type, individuals must select appropriate investment products to meet their financial objectives. These investments could include stocks, bonds, mutual funds, or annuities. It is crucial to diversify the investment portfolio to minimize risk and maximize potential returns. With a withdrawal plan type and investment products in place, individuals can establish a withdrawal schedule. This schedule should outline the frequency and amount of withdrawals, taking into account factors such as age, life expectancy, and financial goals. It is essential to review the withdrawal schedule periodically and make adjustments as needed to ensure it remains aligned with one's financial objectives. Inflation can erode the purchasing power of money over time, which can significantly impact the effectiveness of a withdrawal plan. When creating a withdrawal plan, individuals should factor in the potential impact of inflation on their investment returns and withdrawal amounts. This may involve adjusting the withdrawal rate or incorporating inflation-protected investments into the portfolio. A withdrawal plan should not be a static document. Instead, it is essential to review and adjust the plan periodically to account for changes in one's financial situation, goals, or market conditions. Regular reviews can help ensure that the withdrawal plan remains on track and continues to meet one's financial needs. A well-structured withdrawal plan can provide a regular income stream, helping individuals maintain their desired lifestyle during retirement or periods of reduced income. This regular income can offer financial stability and peace of mind. A withdrawal plan can facilitate effective budgeting by providing a predictable income stream. This enables individuals to plan their expenses more accurately and make informed decisions about their spending. A carefully designed withdrawal plan can help minimize the risk of outliving one's savings. By determining an appropriate withdrawal rate and adjusting the plan as needed, individuals can ensure that their savings last throughout their lifetime. Withdrawal plans offer a range of options to cater to different financial needs and preferences. This flexibility allows individuals to choose a plan that aligns with their specific circumstances, risk appetite, and long-term financial goals. One of the primary concerns with withdrawal plans is the potential impact of inflation on the purchasing power of the withdrawn funds. If a plan does not adequately account for inflation, the withdrawal amounts may become insufficient to cover living expenses over time. Market fluctuations can impact the value of investments within a withdrawal plan, potentially affecting the amount and sustainability of the income stream. Although diversification can help mitigate this risk, individuals must remain mindful of the potential impact of market volatility on their withdrawal plan. Depending on the type of withdrawal plan and investment products chosen, there may be tax consequences that affect the overall effectiveness of the plan. It is crucial for individuals to understand the tax implications of their chosen withdrawal strategy and make adjustments as necessary to minimize their tax burden. A well-designed withdrawal plan is crucial for ensuring financial stability and maintaining a desired lifestyle during retirement or periods of reduced income. By carefully considering factors such as age, life expectancy, risk appetite, and financial goals, individuals can create a withdrawal plan that meets their specific needs and provides a reliable source of income. Withdrawal plans offer numerous advantages, including providing a regular income, aiding in budgeting, minimizing the risk of outliving savings, and offering flexibility to cater to individual needs. However, there are also potential drawbacks to consider, such as the impact of inflation, market risk, and tax implications. By weighing these factors carefully, individuals can make informed decisions about the best withdrawal plan for their circumstances.What Is a Withdrawal Plan?

Types of Withdrawal Plans

Systematic Withdrawal Plan (SWP)

Lump Sum Withdrawal Plan

Periodic Withdrawal Plan

Ad-Hoc Withdrawal Plan

Factors to Consider Before Creating a Withdrawal Plan

Age and Life Expectancy

Risk Appetite

Current Financial Status

Long-Term Financial Goals

Tax Implications

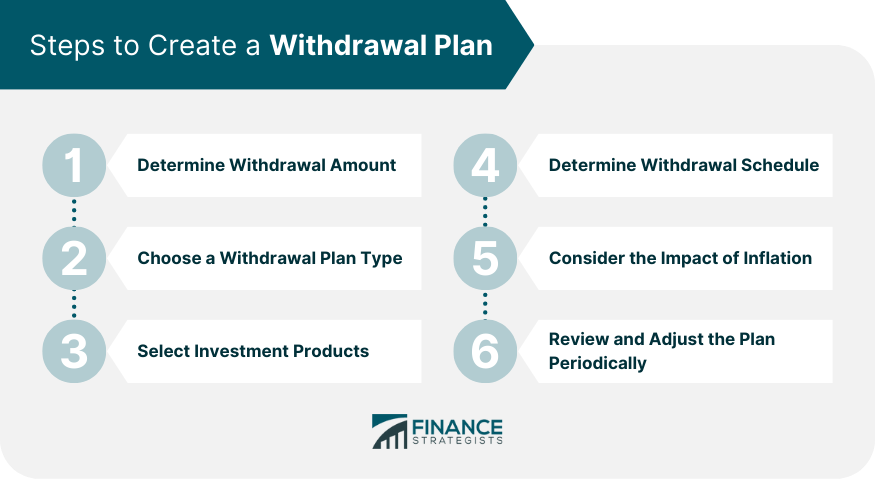

Steps to Create a Withdrawal Plan

Determine Withdrawal Amount

Choose a Withdrawal Plan Type

Select Investment Products

Determine Withdrawal Schedule

Consider the Impact of Inflation

Review and Adjust the Plan Periodically

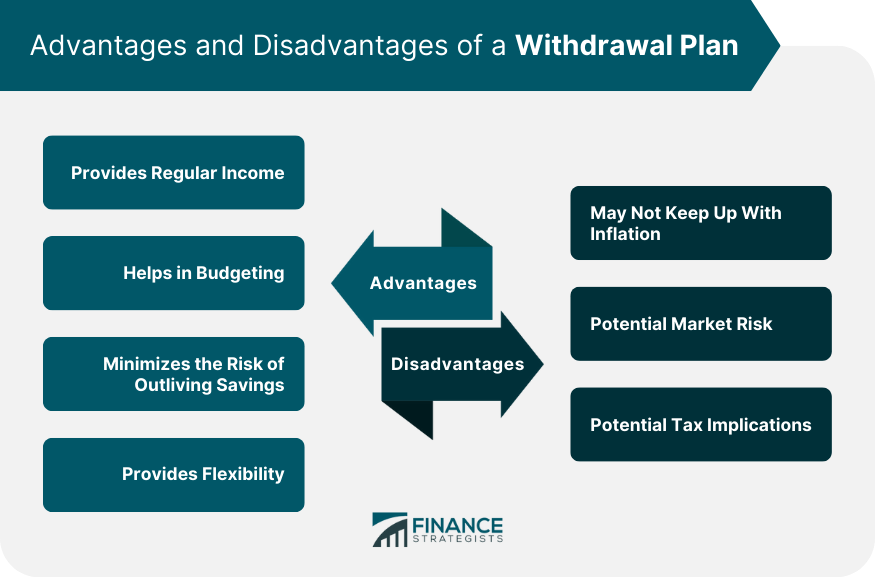

Advantages of a Withdrawal Plan

Provides Regular Income

Helps in Budgeting

Minimizes the Risk of Outliving Savings

Provides Flexibility

Disadvantages of a Withdrawal Plan

May Not Keep Up With Inflation

Potential Market Risk

Potential Tax Implications

Conclusion

Withdrawal Plan FAQs

Withdrawal Plan is a financial strategy that determines how you will withdraw funds from your investments over time.

There are several types of Withdrawal Plans, including Systematic Withdrawal Plan (SWP), Lump Sum Withdrawal Plan, Periodic Withdrawal Plan, and Ad-hoc Withdrawal Plan.

To create a Withdrawal Plan, you should determine the amount to withdraw, choose a withdrawal plan type, select investment products, determine the withdrawal schedule, and consider the impact of inflation.

A Withdrawal Plan can provide regular income, help in budgeting, minimize the risk of outliving savings, and provide flexibility.

Withdrawal Plans may not keep up with inflation, may expose you to potential market risks, and may have potential tax implications.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.