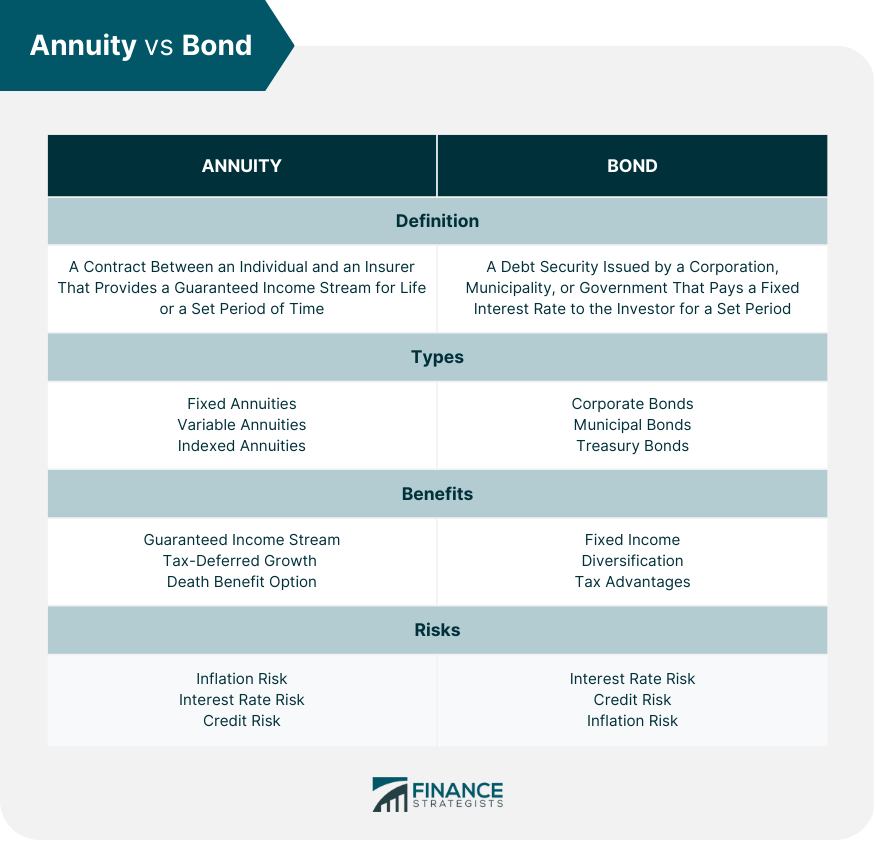

When it comes to investing, two common options are annuities and bonds. An annuity is a financial product which provides a guaranteed income stream for a set period or for the rest of the investor's life. Bonds are debt securities offered by corporations, municipalities, or governments, which pay investors a fixed interest rate over a set period of time. It is essential to know the differences between annuities and bonds because they have different risk and return profiles, fees, and tax implications, and are suitable for different investment goals and time horizons. By gaining a clear understanding of these two options, investors can make decisions about which product is best suited to their needs and financial goals. Here are some features of an annuity: The basic concept of an annuity is that the investor pays a sum of money to an insurance company or other financial institution, which then pays out a fixed amount of money to the investor on a regular basis. There are several types of annuities available in the market: These are annuities that provide a guaranteed fixed interest rate for a set period. This type of annuity is often compared to a certificate of deposit (CD) as they both provide a fixed rate of return. One significant advantage of a fixed annuity is that the investor is guaranteed a fixed income stream regardless of market conditions. However, a significant disadvantage of a fixed annuity is that the interest rate is often lower than other types of annuities, which means that investors may not be able to keep up with inflation. Variable annuities allow the investor to invest in a range of sub-accounts, which are similar to mutual funds. The value of the sub-accounts can fluctuate based on market conditions, which means that the investor may have the potential to earn higher returns. They are often sold as a way to invest for retirement as they provide the investor with the ability to grow their investment over time. However, one significant disadvantage of variable annuities is that they often have high fees, which can significantly reduce the investor's returns. These annuities that provide returns based on the performance of a stock market index, such as the S&P 500. Indexed annuities have become increasingly popular in recent years as they offer the potential for higher returns than fixed annuities without the risks associated with variable annuities. The interest rate is often based on a percentage of the increase in the stock market index over a set period. A disadvantage of indexed annuities is that the return is often capped, which means that the investor may not be able to fully take advantage of the potential gains in the stock market. Annuities offer several benefits to investors: An annuity provides a guaranteed income stream for a set period or the rest of the investor's life. This can be particularly beneficial for retirees who want a stable source of income to supplement their retirement savings. Annuities also offer tax-deferred growth, which means that the investor does not have to pay taxes on the earnings until they withdraw the money. This can be advantageous for investors who are in a high tax bracket and are looking for a way to reduce their tax liability. If the investor dies before the end of the annuity term, their beneficiary will receive a payout based on the value of the annuity. This can provide peace of mind to investors who are concerned about leaving something behind for their loved ones. Despite the benefits that annuities offer, there are also several risks involved: Inflation risk refers to the risk that the value of the annuity income stream will not keep up with inflation, which can erode the purchasing power of the investor over time. The purchasing power of the income stream will decline over time, which can significantly impact the investor's standard of living. Investors can mitigate inflation risk by choosing an annuity that provides a cost of living adjustment (COLA) feature, which adjusts the income stream based on changes in the consumer price index (CPI). When interest rates rise, the value of the fixed income investments that insurance companies use to fund annuities also increases. This means that the insurance companies can offer higher interest rates on new annuity contracts, which can make existing annuities less valuable. Investors can choose a variable annuity or an indexed annuity, which provides the potential for higher returns based on market conditions. Credit risk is the risk that the insurance company or other financial institution that provides the annuity may default on its obligations to pay the investor. Credit risk can be mitigated by choosing a reputable insurance company or financial institution with a strong credit rating. It is essential to know the following features to understand a bond: A bond is a debt security issued by a corporation, municipality, or government that pays a fixed interest rate to the investor for a set period. When an investor purchases a bond, they are essentially lending money to the issuer, who then uses the funds to finance their operations or projects. There are several types of bonds available in the market: These are issued by corporations to raise capital. Corporate bonds are often used to finance mergers and acquisitions, research and development, and other capital expenditures. One significant advantage of corporate bonds is that they often offer higher yields than other types of bonds, which means that investors have the potential to earn higher returns. A disadvantage of corporate bonds is that they also carry a higher credit risk, which means that there is a higher likelihood that the issuer may default on the bond. Municipal bonds are issued by state and local governments to finance public projects, such as schools, hospitals, and infrastructure. Municipal bonds are often tax-exempt, which means that investors do not have to pay federal taxes on the interest income earned from the bonds. They offer a lower credit risk than corporate bonds, which means that they are considered a safer investment. However, they often offer lower yields than other types of bonds, which means that investors may not be able to earn as much return on their investment. These are bonds issued by the U.S. government to finance its operations. Treasury bonds are often considered the safest investment because they are backed by the full faith and credit of the U.S. government. Investing in bonds can offer several benefits to investors. One of the primary benefits of bond investing is that it provides a fixed income stream to the investor. Bonds pay a fixed interest rate to the investor for a set period, which means that investors have a stable source of income to supplement their retirement savings. This is particularly beneficial for retirees who are looking for a regular source of income to cover their living expenses. Bonds can help investors spread their risk across different sectors of the economy. Investing in bonds from different sectors, such as corporate, municipal, and Treasury bonds, can help mitigate the risks associated with any single sector. Diversification can help investors reduce the overall volatility of their portfolio and potentially increase their returns. Bonds offer tax-exempt interest income on municipal bonds or tax-deferred interest income on certain types of bonds. Municipal bonds issued by state and local governments are often tax-exempt. Investors do not have to pay federal taxes on the interest income earned from the bonds. Some types of bonds, such as savings bonds, also offer tax-deferred interest income, which means that investors do not have to pay taxes on the interest until they redeem the bonds. Despite the benefits that bond investing offers, there are also several risks involved. When interest rates rise, the value of existing bonds decreases because investors can earn a higher rate of return elsewhere. Conversely, when interest rates decline, the value of existing bonds increases because investors are willing to pay more for the bonds to earn the fixed interest rate. The issuer may not be able to pay back the principal or interest owed to the investor. The credit risk associated with a bond depends on the creditworthiness of the issuer. Bonds issued by companies or governments with weak credit ratings are considered to be riskier than those with strong credit ratings. Inflation risk is the risk that the value of the bond income stream will not keep up with inflation, which can erode the purchasing power of the investor over time. For example, if an investor purchases a bond that pays a fixed interest rate of 3% per year, but the inflation rate is 4% per year, the real value of the bond income stream will decrease by 1% per year. Choosing between an annuity and a bond requires careful consideration of several factors An investor's investment goals will dictate the type of investment that is most appropriate for their needs. For instance, an investor who is looking for a guaranteed income stream for life may be better suited for an annuity, while an investor who is looking for a fixed income stream for a set period may be better suited for a bond. It is essential to consider investment goals carefully before making a decision to ensure that the investment aligns with the investor's needs and financial objectives. Time horizon refers to the length of time that they plan to hold the investment. An investor who is approaching retirement may have a shorter time horizon than an investor who is just starting their career. Annuities are generally better suited for investors with a longer time horizon because they provide a guaranteed income stream for life or a set period. Bonds may be more suitable for investors with a shorter time horizon because they provide a fixed income stream for a set period. An investor with a low risk tolerance may be more comfortable with the guaranteed income stream provided by an annuity, while an investor with a higher risk tolerance may be more comfortable with the potential higher yields offered by certain types of bonds. It is important to consider risk tolerance carefully when choosing between annuity and bond to ensure that the investment aligns with the investor's risk preferences. An annuity is a contract between an individual and an insurer that provides a guaranteed income stream for life or a set period of time While a bond is a debt security issued by a corporation, municipality, or government that pays a fixed interest rate to the investor for a set period. One of the main differences between annuity and bond is that annuities provide a guaranteed income stream, while bonds offer a fixed income stream. Annuities come in different types, such as fixed, variable, and indexed. Bonds also come in different types, such as corporate, municipal, and Treasury bonds. Annuities offer benefits such as tax-deferred growth, death benefit options, and a guaranteed income stream. On the other hand, bonds offer benefits such as fixed income, diversification, and tax advantages. When choosing between annuity and bond, investors should consider several factors, such as investment goals, time horizon, and risk tolerance. To make an informed investment decision, it is important to work with an insurance broker who can help identify the most suitable annuity or bond investment for an investor's needs. An insurance broker can explain the different types of annuities and bonds available.Overview: Annuity vs Bond

What Is an Annuity?

Definition

Types of Annuity

Fixed Annuities

Variable Annuities

Indexed Annuities

Benefits of Annuities

Guaranteed Income Stream

Tax-Deferred Growth

Death Benefit Option

Risks of Annuity

Inflation Risk

Interest Rate Risk

Credit Risk

What Is a Bond?

Definition

Types of Bond

Corporate Bonds

Municipal Bonds

Treasury Bonds

Benefits of Bond Investing

Fixed Income

Diversification

Tax Advantages

Risks of Bond Investing

Interest Rate Risk

Credit Risk

Inflation Risk

Factors to Consider in Choosing Between Annuity and Bond

Investment Goals

Time Horizon

Risk Tolerance

Final Thoughts

Annuity vs Bond FAQs

The main difference between annuity and bond investments is that annuities provide a guaranteed income stream, while bonds offer a fixed income stream.

Annuities come in different types such as fixed, variable, and indexed, while bonds come in different types such as corporate, municipal, and Treasury bonds.

Annuities offer benefits such as tax-deferred growth, death benefit options, and a guaranteed income stream, while bonds offer benefits such as fixed income, diversification, and tax advantages.

The risks associated with annuity investments include inflation risk, interest rate risk, and credit risk, while bond investments are subject to interest rate risk, credit risk, and inflation risk.

The factors to consider when choosing between annuity and bond investments include investment goals, time horizon, and risk tolerance. It is also recommended to work with an insurance broker to identify the most suitable investment for your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.