Investment-linked annuities are financial products that combine the features of insurance and investment. These annuities provide investors with the opportunity to generate returns based on the performance of underlying investments, while also providing a guaranteed income stream during retirement. They offer an alternative to traditional annuities, which provide fixed payments based on a predetermined interest rate. Investment-linked annuities are designed to help investors achieve their long-term financial goals, such as funding retirement, by offering the potential for higher returns than traditional annuities. These products allow investors to participate in the growth of the financial markets, while still providing the security of a guaranteed income stream. This makes them an attractive option for those looking to balance risk and reward in their retirement planning. Traditional annuities provide a fixed income stream based on a predetermined interest rate. In contrast, investment-linked annuities offer the potential for higher returns based on the performance of underlying investments. While this introduces an element of risk, it also allows investors to benefit from the growth of the financial markets. This added growth potential makes investment-linked annuities an appealing option for investors seeking more than just a fixed income stream. Variable annuities invest in a range of subaccounts, which are similar to mutual funds. Investors can choose from a variety of investment options, such as stocks, bonds, and money market instruments, allowing them to tailor their investment strategy based on their risk tolerance and financial goals. The performance of variable annuities is directly linked to the performance of the underlying subaccounts. As the value of the subaccounts increases, the value of the annuity contract also increases, potentially leading to higher annuity payments during retirement. However, if the subaccounts perform poorly, the value of the annuity contract may decrease, resulting in lower payments. Variable annuities typically come with higher fees and charges compared to traditional annuities. These fees may include management fees, administrative fees, mortality and expense risk charges, and surrender charges. Investors should carefully review the fee structure of a variable annuity before investing. Indexed annuities are tied to the performance of a specific market index, such as the S&P 500. The participation rate determines the percentage of the index's gain that the annuity will receive. For example, if the participation rate is 80% and the index gains 10%, the annuity will be credited with an 8% gain. Indexed annuities often come with caps and floors, which limit the potential gains and losses. Caps set a maximum percentage that the annuity can gain in a given period, while floors establish a minimum return, providing a level of downside protection. There are various crediting methods used by indexed annuities, such as point-to-point, monthly sum, and monthly average. Each method calculates the index's performance differently, which can impact the annuity's credited interest. Investors should carefully review the crediting method used by an indexed annuity before investing. Investors should assess their risk tolerance before investing in an investment-linked annuity. Variable annuities expose investors to market risk, while indexed annuities offer some level of downside protection. The investment horizon refers to the length of time an investor plans to hold the investment before needing to access the funds. Investment-linked annuities are generally better suited for long-term investors who have a longer time horizon before they require income during retirement. This allows them to benefit from potential market gains and ride out market fluctuations. Investors should consider their specific financial goals when selecting an investment-linked annuity. These goals may include generating a higher income during retirement, preserving capital, or providing a legacy for heirs. Different annuity products may be more suitable for achieving certain goals, so it is important to align the chosen product with the investor's objectives. Investment-linked annuities tend to have higher fees and charges compared to traditional annuities. Investors should carefully review the fee structure of the annuity, including management fees, administrative fees, and surrender charges, to ensure they understand the potential costs and how they may impact their investment returns. Guarantees and riders are optional features that can be added to investment-linked annuities to provide additional benefits or protections. Some common riders include guaranteed minimum income benefits, guaranteed minimum withdrawal benefits, and guaranteed minimum accumulation benefits. While these riders can enhance the annuity's features, they often come with additional costs that should be carefully considered. Investment-linked annuities offer the potential for higher returns compared to traditional annuities, as they allow investors to participate in the growth of the financial markets. This added growth potential can help investors achieve their long-term financial goals, such as funding retirement. Investment-linked annuities offer tax-deferred growth, meaning that investment gains are not taxed until they are withdrawn. This allows investors to benefit from compounding growth over time, potentially leading to higher overall returns. Like traditional annuities, investment-linked annuities provide a guaranteed income stream during retirement. This can help investors ensure that they have a reliable source of income to cover their living expenses during their retirement years. Investment-linked annuities typically include death benefits, which provide a payout to the investor's beneficiaries upon their death. This can help provide financial security for the investor's loved ones and ensure that the investor's legacy is preserved. Investment-linked annuities offer investors the opportunity to diversify their investment portfolios by providing exposure to a range of underlying investments, such as stocks, bonds, and money market instruments. This diversification can help reduce overall portfolio risk and improve long-term returns. Investment-linked annuities are more complex than traditional annuities due to their investment components and variable features. Investors must carefully review and understand the product's features, fees, and risks before investing. Investment-linked annuities tend to have higher fees and charges compared to traditional annuities, which can erode investment returns and reduce the overall effectiveness of the product. Investors in investment-linked annuities are exposed to market risk, meaning that their returns may be impacted by fluctuations in the financial markets. This introduces an element of uncertainty, as poor market performance may result in lower annuity payments. Investment-linked annuities often come with surrender charges, which are fees assessed for withdrawing funds before a specified period. These charges can limit the liquidity of the investment, making it less accessible for investors who may need to access their funds earlier than planned. Surrender charges are fees assessed when an investor withdraws funds from an investment-linked annuity before a specified period has passed. These charges can be substantial and may result in a significant reduction of the investor's principal if they need to access their funds early. Investment-linked annuities are regulated by various government and industry organizations, such as the Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA), and state insurance departments. These organizations are responsible for ensuring that investment-linked annuity products are transparent, fair, and comply with all relevant regulations. Regulatory bodies provide investor protection by ensuring that annuity providers are financially stable, disclose all relevant information about their products, and maintain fair business practices. Additionally, some countries have investor compensation schemes in place that may provide limited financial protection to investors in the event of a provider's insolvency. Annuity providers are required to provide investors with detailed information about their investment-linked annuity products, including fees, charges, investment options, risks, and guarantees. This information is typically provided in a prospectus or other disclosure documents that must be reviewed by investors before making an investment decision. Investors can start by identifying insurance companies and financial institutions that offer investment-linked annuities. This can be done through online research, seeking recommendations from friends and family, or working with a financial advisor. Once potential providers have been identified, investors should compare the features, fees, and performance of various investment-linked annuity products to determine which best aligns with their financial goals and risk tolerance. Investors should also evaluate the financial strength and reputation of the annuity provider, as this can impact the provider's ability to meet its obligations and provide a reliable income stream during retirement. Investors may benefit from working with an insurance broker who can provide guidance on selecting an investment-linked annuity product, evaluating providers, and integrating the annuity into their overall financial plan. Investment-linked annuities can be an effective tool in retirement planning, providing a balance of growth potential and guaranteed income. Investors should consider how these products fit into their overall investment strategy and risk tolerance. Investment-linked annuities offer a balance between risk and reward, allowing investors to participate in market growth while still providing a guaranteed income stream. Investors should carefully evaluate their risk tolerance and investment objectives when incorporating investment-linked annuities into their retirement plans. Investors should develop a withdrawal strategy for their investment-linked annuities, taking into consideration factors such as required minimum distributions, tax implications, and the need for ongoing income during retirement. Investment-linked annuities offer tax-deferred growth, which can provide significant tax advantages over time. However, withdrawals from investment-linked annuities are generally taxed as ordinary income, which may impact an investor's overall tax strategy during retirement. Case studies of successful investment-linked annuity investments can provide valuable insights into the strategies and factors that have contributed to positive outcomes, such as appropriate risk management, diversified investment portfolios, and effective withdrawal strategies. Analyzing case studies of less successful investment-linked annuity investments can help investors identify potential pitfalls and learn valuable lessons. Common issues may include inadequate diversification, failure to account for fees and charges, or unrealistic expectations regarding investment returns. Investment-linked annuities offer a unique combination of growth potential and guaranteed income, making them an attractive option for many investors. However, they also come with higher fees, increased complexity, and market risk. Investors should carefully weigh the pros and cons of these products before making an investment decision. By understanding the features, fees, risks, and potential benefits of investment-linked annuities, investors can make more informed decisions about whether these products are suitable for their financial goals and risk tolerance. Investors should regularly reevaluate their investment strategies and make adjustments as needed to ensure that their investment-linked annuities continue to align with their long-term financial goals and changing market conditions. Working with a financial advisor can be helpful in this process, as they can provide guidance on optimizing investment strategies and navigating the complexities of investment-linked annuities.What Are Investment-Linked Annuities?

Purpose and Benefits

Comparison With Traditional Annuities

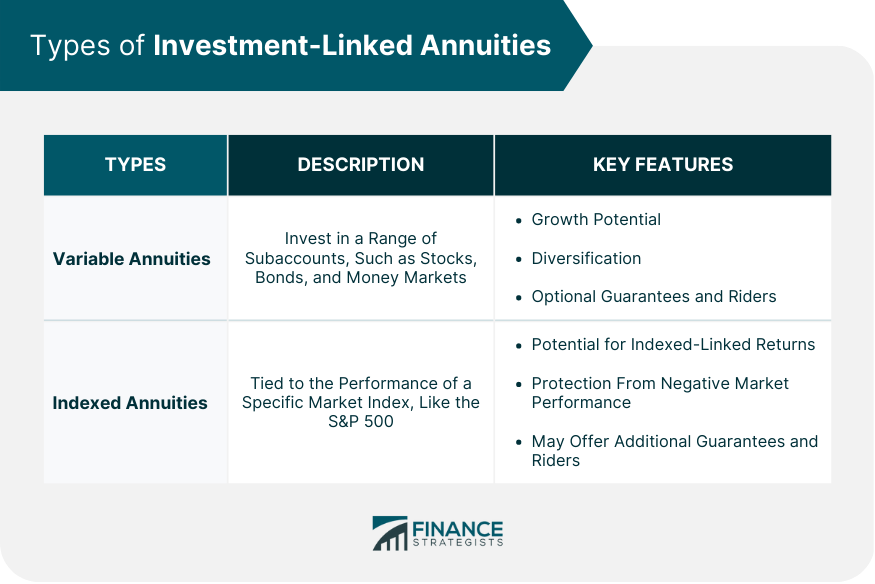

Types of Investment-Linked Annuities

Variable Annuities

Subaccounts

Performance

Fees and Charges

Indexed Annuities

Participation Rates

Caps and Floors

Crediting Methods

Factors to Consider When Choosing an Investment-Linked Annuity

Risk Tolerance

Investment Horizon

Financial Goals

Fees and Charges

Guarantees and Riders

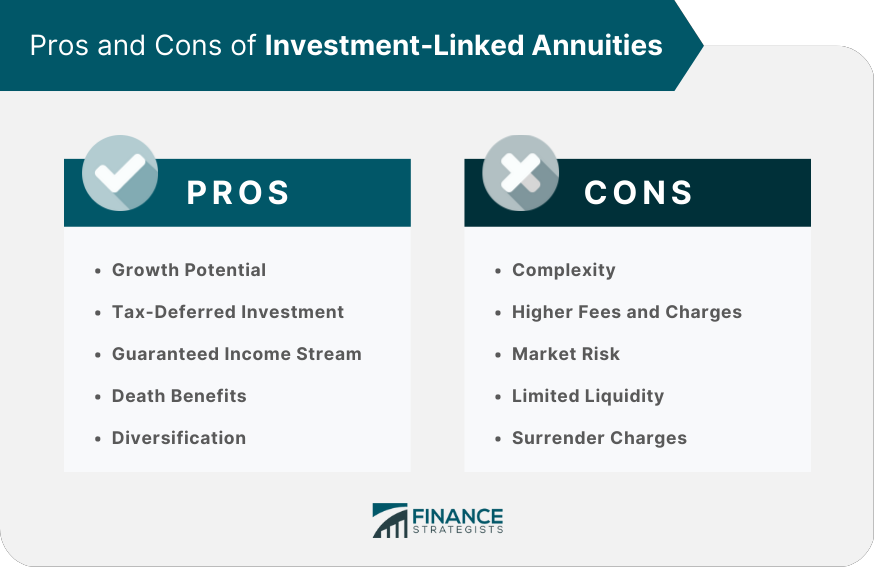

Pros of Investment-Linked Annuities

Growth Potential

Tax-Deferred Investment

Guaranteed Income Stream

Death Benefits

Diversification

Cons of Investment-Linked Annuities

Complexity

Higher Fees and Charges

Market Risk

Limited Liquidity

Surrender Charges

Regulation and Oversight

Regulatory Bodies

Investor Protection

Disclosure Requirements

How to Purchase Investment-Linked Annuities

Identifying Providers

Comparing Products

Assessing Financial Strength and Reputation

Working With an Insurance Broker

Investment-Linked Annuities in Retirement Planning

Integrating Investment-Linked Annuities Into a Retirement Plan

Balancing Risk and Reward

Withdrawal Strategies

Tax Implications

Case Studies

Successful Investment-Linked Annuity Investments

Common Pitfalls and Lessons Learned

The Bottom Line

Investment-Linked Annuities FAQs

Investment-linked annuities are financial products that combine the features of insurance and investment, offering the potential for higher returns based on the performance of underlying investments while providing a guaranteed income stream during retirement. Unlike traditional annuities, which provide fixed payments based on a predetermined interest rate, investment-linked annuities allow investors to participate in the growth of the financial markets.

There are two main types of investment-linked annuities: variable annuities and indexed annuities. Variable annuities invest in a range of subaccounts, such as stocks, bonds, and money market instruments, while indexed annuities are tied to the performance of a specific market index, like the S&P 500.

When selecting an investment-linked annuity, consider your risk tolerance, investment horizon, financial goals, fees and charges associated with the product, and any guarantees or riders available. It's also important to assess the financial strength and reputation of the annuity provider.

The advantages of investment-linked annuities include growth potential, tax-deferred investment, guaranteed income stream, death benefits, and diversification. However, disadvantages include their complexity, higher fees and charges, market risk, limited liquidity, and surrender charges.

To increase the likelihood of success with your investment-linked annuity, carefully evaluate your risk tolerance, investment horizon, and financial goals, and work with a financial advisor or insurance broker to select the most suitable product. Regularly reevaluate your investment strategy, make adjustments as needed, and monitor the performance of your annuity to ensure it continues to align with your long-term objectives.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.