Variable annuities are long-term investment vehicles that provide a way for individuals to accumulate tax-deferred savings for retirement. They are contracts between investors and insurance companies, whereby the investor makes a lump sum payment or series of payments in exchange for periodic income payments during retirement. The value of the investments within the annuity can fluctuate based on the performance of the underlying investment options. Living benefit riders are optional features that can be added to variable annuities for an additional cost. These riders provide guarantees and protections related to the annuity's income and withdrawal features, ensuring a level of financial security for the policyholder during retirement. The primary purpose of adding living benefit riders to variable annuities is to provide a guaranteed income stream, protection from market volatility, and financial security for retirees. These riders help address common retirement concerns, such as outliving one's savings or navigating market downturns. The Guaranteed Lifetime Withdrawal Benefit (GLWB) rider allows the annuity owner to withdraw a certain percentage of their investment each year, for as long as they live, regardless of market performance. This provides a predictable income stream throughout retirement. Withdrawal rates for GLWB riders typically range from 4% to 6% per year, depending on factors such as the annuity owner's age and the rider's specific terms. Some riders may also impose minimum age requirements before withdrawals can begin. The Guaranteed Minimum Income Benefit (GMIB) rider provides a guaranteed minimum income for life, regardless of the annuity's investment performance. The annuity owner must annuitize the contract to receive this income, meaning they give up control of the assets in exchange for regular income payments. The guaranteed income provided by a GMIB rider is calculated using a predetermined formula, which may consider factors such as the initial investment amount, age, and gender. The actual income payment could be higher if the annuity's investments perform well. The Guaranteed Minimum Withdrawal Benefit (GMWB) rider ensures the annuity owner can withdraw a set percentage of their initial investment each year, regardless of investment performance. If the account value falls due to poor market performance, the guarantee ensures the owner can still make withdrawals. Withdrawal percentages for GMWB riders typically range from 5% to 10% per year. The guarantee period may vary, with some riders providing lifetime guarantees, while others may only offer a fixed number of years. The Guaranteed Minimum Accumulation Benefit (GMAB) rider provides a guarantee that the annuity's account value will not fall below a certain amount after a specified time period, regardless of market performance. GMAB riders typically have time horizons ranging from 10 to 20 years. The minimum guaranteed amount is often expressed as a percentage of the initial investment or as a specific dollar amount. Variable annuities with living benefit riders often have mortality and expense risk charges, which compensate the insurance company for the risks they assume in providing the guarantees. Insurance companies may charge administrative fees for managing the variable annuity and the associated living benefit riders. Adding living benefit riders to a variable annuity typically involves additional fees that are specific to each rider. Investment options within variable annuities may have management fees, which are charged by the investment managers for their services. Surrender charges may apply if the annuity owner withdraws money from the annuity or cancels the contract before a specified time period has passed. Living benefit riders provide guaranteed income streams, ensuring retirees have a stable source of income throughout their retirement years. Variable annuities with living benefit riders allow investors to participate in market growth while still providing income guarantees. This offers the potential for higher returns compared to more conservative investment options. Investors can choose from a variety of living benefit riders to tailor their variable annuity to their specific needs and retirement goals. This customization provides flexibility in retirement income planning. Living benefit riders help protect retirees from outliving their savings by providing guaranteed income streams for life, regardless of market performance or fluctuations in account value. Variable annuities offer tax-deferred growth on the investment earnings, allowing investors to potentially accumulate more savings over time. Variable annuities are subject to market risk, meaning the account value may fluctuate based on the performance of the underlying investments. The income guarantees provided by living benefit riders may not keep pace with inflation, potentially eroding the purchasing power of the guaranteed income over time. Living benefit riders may have specific limitations, such as withdrawal restrictions or waiting periods, which can impact the policyholder's flexibility. Excessive withdrawals can negatively impact the guarantees provided by living benefit riders, potentially reducing the guaranteed income available during retirement. The long-term performance of the variable annuity and the guarantees provided by the living benefit riders will depend on factors such as market performance, fees, and the financial strength of the insurance company. Before selecting a variable annuity with living benefit riders, it is essential for investors to evaluate their financial goals and determine how these products fit within their overall retirement plan. It is crucial to research and select an insurance company with a strong financial rating and a positive reputation for managing variable annuities and living benefit riders. Investors should compare various living benefit riders, considering factors such as fees, guarantees, and restrictions to determine the best fit for their needs. Consulting with a financial advisor can help investors navigate the complex world of variable annuities and living benefit riders, ensuring they make well-informed decisions aligned with their retirement goals. Variable annuities with living benefit riders can provide valuable guarantees and protections for retirees, but it is essential for investors to understand the associated costs, risks, and benefits before committing to such an investment. A thorough understanding of these products will help investors make informed decisions and determine if a variable annuity with living benefit riders is the right fit for their retirement strategy. Investors must carefully weigh the potential benefits of variable annuities with living benefit riders against the associated costs and risks. While these products can provide valuable income guarantees and market protection, they may also come with higher fees and limitations compared to other investment options. Variable annuities with living benefit riders can play a valuable role in a comprehensive retirement plan by providing guaranteed income, market protection, and tax-deferred growth. However, they should not be considered a one-size-fits-all solution. Instead, investors should consider these products as one component of a diversified retirement portfolio designed to meet their unique financial needs and goals. Consult an insurance broker or financial advisor for expert guidance on variable annuities with living benefit riders. What Are Variable Annuities With Living Benefit Riders?

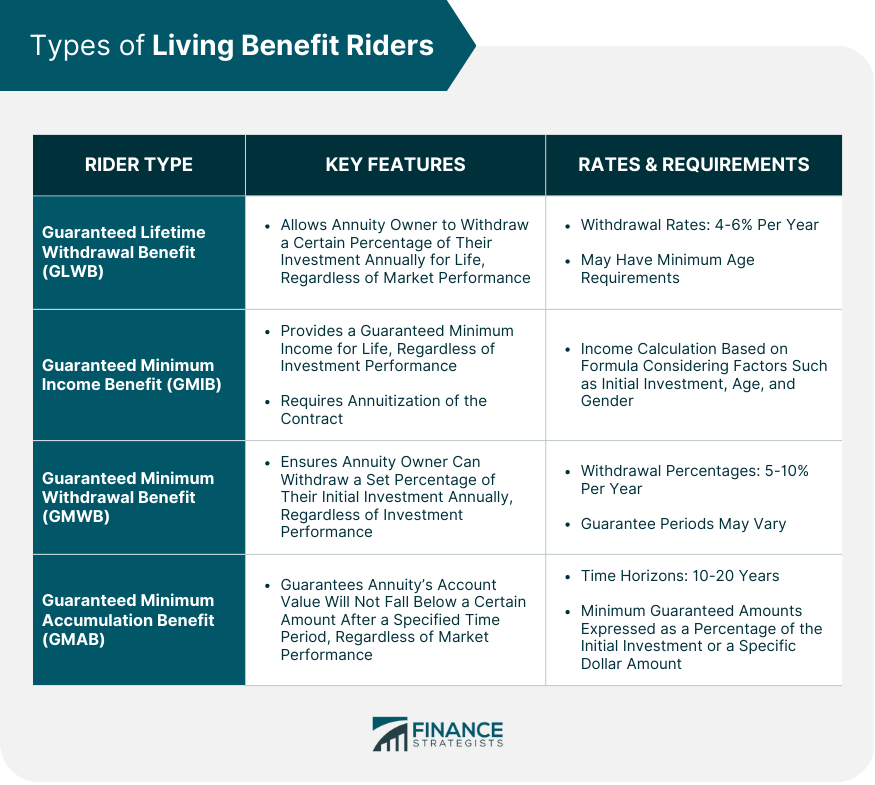

Types of Living Benefit Riders

Guaranteed Lifetime Withdrawal Benefit (GLWB)

Key Features

Withdrawal Rates and Age Requirements

Guaranteed Minimum Income Benefit (GMIB)

Key Features

Annuity Income Calculation and Rates

Guaranteed Minimum Withdrawal Benefit (GMWB)

Key Features

Withdrawal Percentage and Guarantee Periods

Guaranteed Minimum Accumulation Benefit (GMAB)

Key Features

Time Horizons and Minimum Guaranteed Amounts

Costs and Fees Associated With Living Benefit Riders

Mortality and Expense Risk Charges

Administrative Fees

Rider Fees

Fund Management Fees

Surrender Charges

Advantages of Variable Annuities With Living Benefit Riders

Income Guarantees

Market Participation and Growth Potential

Flexibility and Customization

Protection Against Outliving Savings

Tax-Deferred Growth

Considerations for Variable Annuities With Living Benefit Riders

Market Risk

Inflation Risk

Rider Limitations

Impact of Withdrawals on Guarantees

Long-Term Performance and Guarantees

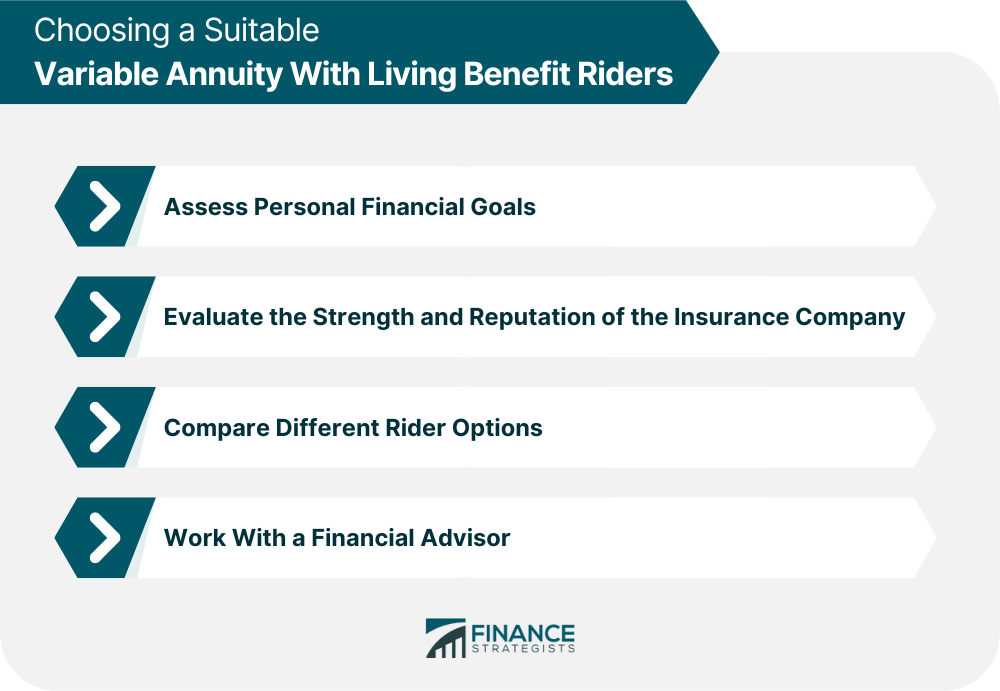

Choosing a Suitable Variable Annuity With Living Benefit Riders

Assess Personal Financial Goals

Evaluate the Strength and Reputation of the Insurance Company

Compare Different Rider Options

Work With a Financial Advisor

The Bottom Line

Variable Annuities With Living Benefit Riders FAQs

Variable annuities with living benefit riders are insurance contracts that provide investors with a combination of investment options and insurance protection. They offer a range of investment options, and the value of the annuity can fluctuate based on the performance of these investments. Additionally, living benefit riders can provide guarantees and protection against market volatility.

Living benefit riders are optional add-ons to variable annuities that provide guaranteed benefits to the annuity holder, even if the market performance is poor. These riders can provide a guaranteed minimum income benefit, a guaranteed minimum withdrawal benefit, or a guaranteed death benefit. The cost of the rider is usually a percentage of the annuity's account value, and the guarantee amount is determined by the annuity's underlying investments.

Variable annuities with living benefit riders can provide a range of benefits to investors. They offer tax-deferred growth potential, which can help to maximize investment returns over time. Additionally, living benefit riders can provide a level of protection against market volatility and guarantee a certain level of income, even if the annuity's investments perform poorly.

There are several risks associated with variable annuities with living benefit riders, including the possibility of losing principal due to poor investment performance, the cost of the rider reducing the overall investment returns, and the risk of the insurance company failing to meet its contractual obligations. Additionally, these annuities typically have high fees and surrender charges that can be costly if the investor needs to withdraw funds before the end of the annuity's term.

The fees for variable annuities with living benefit riders can vary depending on the insurance company and the specific annuity contract. Typically, several types of fees are associated with these annuities, including mortality and expense charges, administrative fees, investment management fees, and rider fees for living benefit guarantees.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.