Annuities are investment products issued by insurance companies designed to provide an income stream in the future. The truth about annuities is that they serve multiple purposes beyond just retirement, are accessible to average investors, and have a variety of fee structures. Understanding the truth has a significant impact on readers, empowering them to make informed decisions about whether annuities fit their financial goals. This concept takes on more importance considering the context of a volatile economy, where the certainty offered by annuities could be a crucial part of diversified financial planning. Many individuals believe that annuities are only relevant for those approaching retirement. This misconception arises because annuities are often discussed in the context of retirement planning. Annuities are not just for retirees. They can serve as a financial tool for anyone seeking to generate a steady income stream, manage risk, or diversify their investment portfolio. For instance, younger investors can use annuities to accumulate wealth over time, and they can be a tax-efficient way of saving more when one maxes out their regular retirement contributions. Another misconception is that annuities are too intricate for the average investor to comprehend or access. The basic concept of an annuity is simple: an individual makes an investment in the annuity, and then it pays out income at a later time. It’s as accessible as any other financial product. Sure, the terms and conditions can become complicated, but with due diligence or with the help of a financial advisor, investors can navigate these complexities. The belief that annuities always come with high costs and hidden fees is another widespread misconception. While it's true that some annuities can have high fees, it's not a rule. The cost varies depending on the type of annuity, the issuing insurance company, and the contract terms. Transparency in fees is a requirement, and all fees must be disclosed in the contract. Understanding the contract is key. This is where a trusted financial advisor can be invaluable, helping you dissect and understand the contract terms and the potential costs involved. Another prevailing thought is that annuities are a poor investment, primarily due to their perceived high costs and lower returns compared to riskier investments like stocks. Annuities are not for everyone, but they can be a sound investment in the right circumstances. The critical factor here is the guaranteed income stream they offer, which few other investment vehicles can match. Compared to other investment vehicles, annuities may provide lower returns. However, they also offer lower risk, and in the world of finance, lower risk typically means lower returns. It's about balance and understanding your own risk tolerance and investment objectives. Some people think that investing in an annuity means surrendering control over their money. This stems from the fact that annuity investments usually involve a commitment to keep the money invested for a certain period. While it's true that annuities come with certain terms and conditions, many annuities offer various withdrawal options, including free partial withdrawals. The key is to understand the terms of your annuity contract and ensure it aligns with your financial goals. Many fear that if the insurance company issuing the annuity goes bankrupt, they will lose their investment. In reality, several safeguards protect annuity owners. Each state in the U.S. has a guarantee association that offers protection to annuity owners, within limits, if the insurance company fails. Additionally, insurance companies are required to maintain reserves to meet their obligations. Annuities have long been a subject of debate and misconception in the world of financial planning. While they can be a valuable tool for retirement income, there are common misconceptions that can hinder individuals from considering annuities as part of their financial strategy. Let's address and overcome some of these misconceptions. One common misconception is that annuities lack flexibility. While some annuities have restrictions, there are various types available that offer flexibility in terms of withdrawal options, income customization, and even death benefit provisions. Another misconception is that annuities come with high fees. While certain annuity products may have fees associated with them, it's important to explore the full range of options available. There are low-cost annuities with transparent fee structures that can provide value and benefits to investors. Some individuals believe that annuities have limited growth potential compared to other investment vehicles. However, annuities offer tax-deferred growth, allowing your investments to potentially grow faster due to compounding over time. Concerns about inflation eroding the purchasing power of annuity income are common. However, many annuities offer inflation protection features such as cost-of-living adjustments, which can help ensure that your income keeps pace with inflation. Annuities are not a one-size-fits-all solution. They should be considered as part of a comprehensive financial plan, tailored to an individual's unique goals and circumstances. By understanding the truth about annuities and dispelling these common misconceptions, individuals can make informed decisions about incorporating annuities into their retirement income strategy. Consulting with a financial advisor can provide further guidance and help determine if annuities are suitable for your specific needs. "The Truth About Annuities" sheds light on common misconceptions surrounding annuities and provides clarity on their true value in financial planning. Annuities are not limited to retirement, as they offer income streams, risk management, and portfolio diversification. While some annuities have fees, low-cost options exist with transparent structures. Tax-deferred growth and inflation protection features address concerns about limited growth potential and the impact of inflation. Annuities are not a one-size-fits-all solution, requiring customization based on individual goals. Understanding the truth empowers individuals to make informed decisions, especially in uncertain economic times where annuities can play a significant role in diversified financial plans. Overcoming misconceptions allows individuals to fully explore the benefits and suitability of annuities, with guidance from financial advisors for personalized strategies.The Truth About Annuities Overview

Common Misconceptions About Annuities

Misconception I: Annuities Are Only for Retirement

Explanation of the Misconception

Counter-Arguments and Real Uses of Annuities

Misconception II: Annuities Are Too Complex and Inaccessible

Explanation of the Misconception

Simplification of Annuities and Accessibility

Misconception III: Annuities Are Expensive and Have Hidden Fees

Explanation of the Misconception

Discussion on Annuities' Costs and Fees

Importance of Transparency and Understanding the Contract

Misconception IV: Annuities Are a Bad Investment

Explanation of the Misconception

Evaluation of Annuities as an Investment Tool

Comparison With Other Investment Vehicles

Misconception V: Annuities Limit the Control Over My Money

Explanation of the Misconception

Discussion on Flexibility and Control in Annuities

Misconception VI: Annuities Will Not Survive if the Insurance Company Goes Bankrupt

Explanation of the Misconception

Safety Measures in Place for Annuities and the Role of State Guarantee Associations

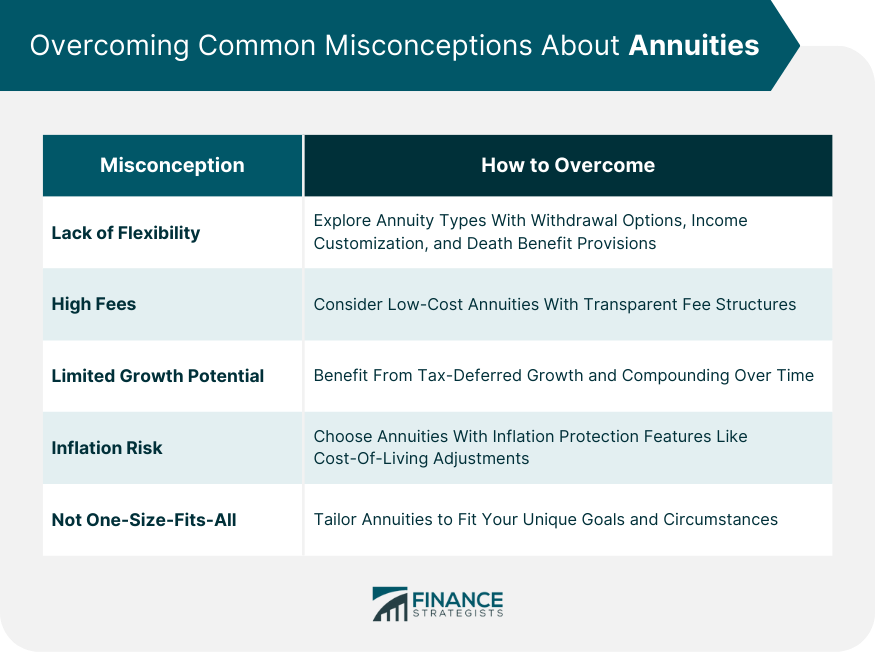

Overcoming Common Misconceptions About Annuities

Lack of Flexibility

High Fees

Limited Growth Potential

Inflation Risk

Annuities as a One-Size-Fits-All Solution

Conclusion

The Truth About Annuities FAQs

The truth about annuities is that they are not exclusively for retirement. While they're commonly used as part of retirement planning for their stable income, they can also serve various financial needs, such as wealth accumulation and risk management, at any stage of life.

Annuities can be complex, but the basic principle is straightforward: an investment that provides an income stream later. The truth about annuities is that, with due diligence or help from a financial advisor, anyone can understand and access them.

The truth about annuities is that their cost and fee structure varies. Some may have high fees, while others don't. Transparency is a requirement in annuity contracts, meaning all fees should be disclosed. A financial advisor can help understand these costs.

The truth about annuities is that they can be a good investment, depending on your financial goals and circumstances. They offer a guaranteed income stream, which few other investments can provide. However, like any investment, they should fit within your overall financial strategy.

The truth about annuities is that they are protected even if the issuing insurance company goes bankrupt. State guarantee associations offer protection to annuity owners within limits, and insurance companies are required to maintain reserves to meet their obligations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.