A lottery annuity is a type of financial arrangement chosen by winners of significant lottery prizes. It offers the winners an option to receive their total winnings in a series of payments over a set period, usually spanning 20 to 30 years, instead of claiming a single lump-sum payment. This annuity payout can serve as a reliable stream of income and acts as a long-term financial safety net for the winners, providing stability and economic security for a large portion of their lives. Once the winner opts for an annuity payout, the lottery organization invests the lump-sum prize in low-risk bonds or other financial vehicles to ensure the prize can generate the required yearly payments over the designated period. Each payment typically includes a portion of the original prize and interest earned. The payments are made annually and continue for the agreed-upon term, often until the winner's death. When a lottery annuity holder dies, the consequences for the remaining annuity payments can be multi-faceted and complex, involving both legal and financial considerations. Consider the following: The first critical step after the death of a lottery annuity holder is to inform the lottery organization. This task is generally handled by the executor or administrator of the deceased's estate, who carries the responsibility of managing and settling the deceased's affairs. This responsibility often extends to notifying other relevant entities about the death, such as banks, credit card companies, and government agencies. In the case of the lottery organization, the executor would likely need to provide a copy of the death certificate and potentially other legal documents to confirm their authority to act on behalf of the estate. Following the death of the annuity holder, the remaining lottery annuity payments usually form part of their estate. This means that the payments will have to go through probate - a legal process that takes place after someone dies. The probate process can be complex and lengthy, involving several stages. Firstly, all of the deceased's assets, including the remaining annuity payments, must be identified and accounted for. This process may involve locating financial records and getting property appraised. Secondly, any outstanding debts or taxes owed by the deceased need to be paid. Only after these debts have been settled can the remaining assets be distributed. How the remaining annuity payments are distributed will depend on the specifics of the deceased's will. If they left a will, they may have named beneficiaries who are to inherit the remaining payments. In this case, the executor of the estate would work to ensure the annuity payments are redirected to these individuals. However, if the deceased did not leave a will, the probate court will distribute their assets, including the annuity payments, according to state intestacy laws. These laws vary by state but typically prioritize spouses, children, and other close family members. Another important consideration is the tax implications that arise when a lottery annuity holder dies. Firstly, the value of the remaining annuity could be subject to federal estate tax, and possibly state estate tax, depending on the total value of the estate and the specific tax laws of the state. These taxes are generally due within nine months of the individual's death and can significantly reduce the amount ultimately received by the beneficiaries. Secondly, as the annuity payments continue to be distributed, they are treated as income for tax purposes. This means that whoever receives these payments will need to report them as income on their tax return and potentially pay income tax on them. Estate planning is crucial for lottery winners who opt for the annuity option. By devising a comprehensive estate plan, winners can ensure the continued payment of their annuity is distributed according to their wishes after their death. A will is the most basic tool in estate planning. A will allows lottery winners to specify how they want their assets, including remaining annuity payments, to be distributed after their death. Without a will, the estate is divided according to state laws, which may not align with the deceased's wishes. It's critical to consult with a lawyer while writing a will to ensure it is legally valid and aligns with your objectives. Trusts are another beneficial tool for managing lottery winnings, especially for large sums that are distributed over many years as an annuity. When a trust is established, it becomes the legal owner of the assets placed into it. Lottery winners can transfer their annuity payments to a trust, which allows them to control how and when the assets are distributed after their death. Trusts can also help avoid probate, maintain privacy, and potentially provide tax benefits. Life insurance can be a strategic tool in estate planning for lottery annuity winners. A life insurance policy can provide a tax-free payout to beneficiaries upon the holder's death, which can help cover estate tax liabilities that may arise from the remaining annuity payments. This can be particularly beneficial if the estate exceeds the federal estate tax exemption limit. Lottery winners may wish to donate a portion of their annuity payments to charity. Not only does this help to support causes they care about, but it can also provide significant tax benefits. Charitable donations can reduce the size of the taxable estate and potentially lower estate tax liabilities. Another strategy that lottery winners might consider is the formation of a Family Limited Partnership (FLP) or a Family Limited Liability Company (LLC). These entities allow for the pooling of family assets, including lottery winnings, into a single entity controlled by family members. This strategy could offer lottery winners a way to manage and control their assets during their lifetime and efficiently transfer wealth to the next generation upon death. Lottery winners could also consider making gifts to loved ones during their lifetime. Under federal law, individuals can make annual gifts up to a certain limit to as many recipients as they want without incurring gift taxes. Over time, this strategy can help reduce the size of the estate, potentially minimizing estate taxes upon the lottery winner's death. Given the complexity of estate planning, especially for lottery winners receiving annuity payments, it is strongly advised to consult with professionals. Estate planning attorneys, financial advisors, and tax professionals can provide expert guidance tailored to individual circumstances and goals. With their assistance, lottery winners can navigate the legal complexities and tax implications to devise a strategic estate plan that ensures their assets are managed and distributed according to their wishes. A lottery annuity offers winners the choice to receive their prize money in regular payments over time, providing them with a stable income stream and long-term financial security. However, when a lottery annuity holder passes away, several legal and financial considerations arise. The executor or administrator of the estate must inform the lottery organization about the annuity holder's death and navigate the probate process. This involves identifying all assets, settling debts and taxes, and distributing the remaining assets based on the deceased's will or state intestacy laws. Tax implications, including potential estate taxes and income taxes on annuity payments, need to be taken into account. To ensure a smooth distribution of the annuity after death, lottery annuity holders should engage in estate planning strategies such as creating a will, establishing a trust, considering life insurance, exploring charitable giving, forming family entities, and implementing gift strategies. Seeking professional consultation from estate planning attorneys, financial advisors, and tax professionals is highly recommended to navigate the complexities and develop a tailored estate plan aligned with the annuity winner's wishes.Overview of Lottery Annuities

What Happens When a Lottery Annuity Holder Dies?

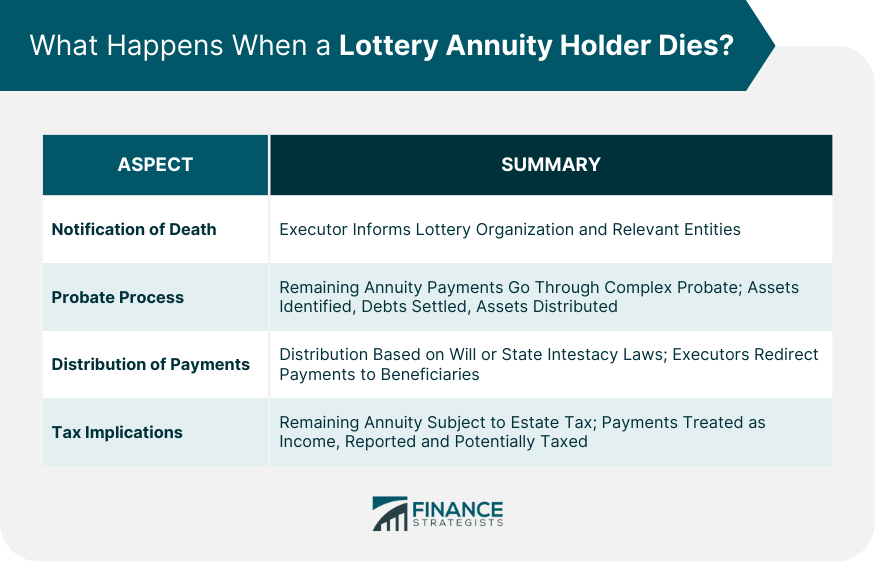

Notification of Death

Probate Process

Distribution of Remaining Payments

Tax Implications

Estate Planning Strategies for Lottery Annuity Holders

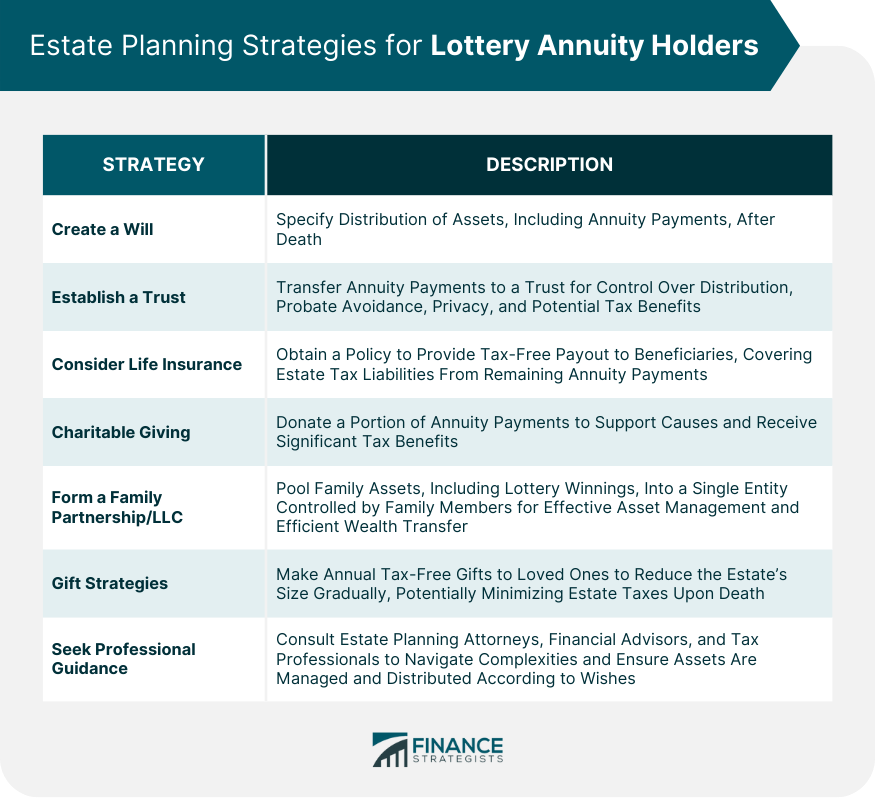

Create a Will

Establish a Trust

Consider Life Insurance

Charitable Giving

Form a Family Limited Partnership or Liability Company

Gift Strategies

Seek Professional Guidance

Final Thoughts

Lottery Annuity After Death FAQs

In the event of the annuity holder's death, the remaining annuity payments become part of their estate and go through the probate process to determine their distribution.

Yes, lottery annuity holders can include instructions in their will regarding the distribution of remaining annuity payments to beneficiaries of their choice.

Yes, there are tax implications involved. The remaining annuity value may be subject to federal and state estate taxes, and the annuity payments are considered income, which may require beneficiaries to report and potentially pay income tax on them.

Lottery annuity holders can engage in estate planning strategies such as creating a will, establishing a trust, considering life insurance, exploring charitable giving, forming family entities, and implementing gift strategies. Consulting with professionals in estate planning, finance, and tax can help ensure a well-crafted estate plan that aligns with their wishes.

If the lottery annuity holder did not leave a will, the probate court will distribute their assets, including the annuity payments, according to state intestacy laws. These laws prioritize spouses, children, and other close family members as potential recipients of the remaining payments.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.