Bankruptcy is a legal term that often induces fear and confusion in the minds of individuals and businesses struggling with mounting debts. It is essentially a legal recourse designed to provide those in financial distress an opportunity to eliminate or repay their debts under the protection of the federal bankruptcy court. Despite its intimidating reputation, bankruptcy can provide a much-needed fresh start. However, an aspect that often worries people contemplating bankruptcy is the fate of their personal assets – homes, cars, savings, and more. Understanding the distinctions between different types of assets – exempt and non-exempt – and their fate post-bankruptcy filing is a critical aspect of this legal process. This understanding not only alleviates fear and misconceptions but also helps individuals make more informed decisions. In the realm of bankruptcy, assets are divided into two categories—exempt and non-exempt. The differentiation between these categories has significant implications on what one can retain after filing for bankruptcy. Exempt assets are a lifeline for those going through bankruptcy. These are assets that the law protects from being seized by creditors. The rationale behind this protection is to ensure that individuals aren't left destitute and have the basic means to restart their lives post-bankruptcy. In contrast, non-exempt assets are vulnerable. These can be sold off or liquidated to repay the outstanding debts to creditors. The term 'common exempt assets' is a broad umbrella, and the exact assets that fall under this category can vary depending on the specifics of the bankruptcy code, the type of bankruptcy filed, and the laws of the state in which one resides. A place to call home is fundamental. Recognizing this, most bankruptcy laws include a homestead exemption, protecting an individual's primary residence. This exemption ensures that people don't end up homeless due to bankruptcy. However, the specifics can vary. For instance, certain states have a cap on the value or acreage that can be exempted. Transportation is a basic necessity for most people, whether it's for commuting to work or running errands. Therefore, bankruptcy laws often protect a person's motor vehicle under a specific exemption. However, the protection usually extends up to a certain value limit, beyond which the vehicle may be considered a non-exempt asset. Everyday household items and furnishings, such as clothing, furniture, kitchen appliances, and bedding, are generally exempted under bankruptcy laws. The underlying rationale is that these items are deemed necessary for maintaining a basic standard of living. However, the protection typically doesn't extend to high-value or luxury items. Personal effects and jewelry, especially items of sentimental value, can often be retained by an individual during bankruptcy. However, as with other categories, there is typically a monetary cap to the exemption, and extremely valuable pieces may fall into the non-exempt asset category. The 'tools of trade' exemption is aimed at those who are self-employed or own a small business. This exemption protects equipment, tools, or inventory essential for a person's livelihood. The cap on this exemption varies, with more generous allowances typically for those whose livelihood directly depends on these items. Protecting the future is as important as managing the present. This principle is embodied in the exemptions related to retirement accounts and insurance policies. Under the federal Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, most tax-exempt retirement accounts are safe from bankruptcy proceedings. This protection ensures that people facing bankruptcy won't be left without means to support themselves in their old age. Life insurance policies, particularly term life policies that don't accumulate cash value, are generally safe in bankruptcy. However, the cash value of whole or universal life insurance policies may also be exempt, depending on the specific bankruptcy rules. While exemptions aim to protect a bankrupt individual's ability to start afresh, non-exempt assets are there to provide some relief to creditors. Here are some common examples of non-exempt assets. Luxury items, such as expensive artwork, high-end electronics, or designer clothing, typically don't make the cut for exemptions. These items are often seen as non-essential, and their sale could contribute significantly to debt repayments. Additional real estate holdings, whether they are vacation homes or rental properties, generally fall into the non-exempt category. The belief is that while one needs a place to live (hence the homestead exemption), additional properties are not essential and can be liquidated to repay debts. Financial investments, excluding retirement accounts, are usually considered non-exempt. This includes any stocks, bonds, mutual funds, or other investment accounts. The assumption is that these assets can be sold off and the proceeds used to pay off creditors. The type of bankruptcy you file—Chapter 7 or Chapter 13—also influences what you can keep. Both have different implications for your assets. In Chapter 7, also known as 'liquidation' bankruptcy, the bankruptcy trustee can sell your non-exempt assets to repay your creditors. However, if all your assets fall into the exempt category, you won't lose anything. Hence, Chapter 7 bankruptcy is often preferred by those with fewer assets. Chapter 13 bankruptcy, also referred to as 'reorganization' bankruptcy, involves developing a repayment plan to pay off your debts over time, typically three to five years. One of the major advantages of Chapter 13 is that you can keep all your assets while you repay your debts. Bankruptcy is governed by both federal and state laws, and these can vary significantly. This impacts the list of exempt and non-exempt assets. Federal law outlines a set of bankruptcy exemptions. However, many states have opted out of these federal exemptions, choosing instead to define their own. Some states provide an option to choose between federal and state exemptions. Given the variation across states, it's crucial to familiarize yourself with the exemption laws specific to your state. Legal professionals or comprehensive resources can provide this localized insight. The bankruptcy trustee is a pivotal figure in the bankruptcy process, with specific duties and responsibilities related to your assets. In bankruptcy proceedings, the trustee serves as the representative of the creditors. In Chapter 7 bankruptcy, they'll liquidate your non-exempt assets to repay the creditors. In Chapter 13 bankruptcy, they manage the collection and distribution of your payments to the creditors. The trustee examines your assets to classify them as exempt or non-exempt. They can contest any asset's status if they believe it's been incorrectly classified. While the prospect of losing your assets can be daunting, there are strategies that can maximize what you retain through bankruptcy. Navigating the intricacies of bankruptcy alone can be overwhelming. A bankruptcy attorney can provide expert advice, helping you protect as many assets as possible. The timing of your bankruptcy filing can have a significant impact on what you can keep. Recent asset acquisitions might be scrutinized more heavily, so strategic planning is important. In some circumstances, it might be legal and advantageous to convert non-exempt assets into exempt ones before filing for bankruptcy. For example, you might use cash (a non-exempt asset) to pay down your mortgage (an exempt asset). Mistakes made during the bankruptcy process can significantly impact its benefits and consequences. It's mandatory to accurately report all assets when filing for bankruptcy. Concealing or misrepresenting assets is fraud and can result in severe penalties, such as dismissal of your case or even criminal charges. Sometimes people rush to sell off their assets to pay debts before filing for bankruptcy, only to discover later those assets could have been exempt. Therefore, understanding your exemption rights before making significant financial decisions is critical. Bankruptcy, while often perceived as a challenging ordeal, can serve as a pathway to a financial reset. Common exempt assets—often protected to ensure individuals aren't left destitute—include a primary residence, motor vehicles, household goods, personal effects, and tools of trade. Retirement accounts and certain life insurance policies also typically enjoy protection. Nonetheless, the process can be complex. Variations exist depending on the type of bankruptcy filed (Chapter 7 or Chapter 13), as well as specific state laws. Further, non-exempt assets, such as luxury goods, additional real estate properties, and non-retirement investments, can be liquidated for debt repayment. Therefore, it's vital to sidestep common missteps like inaccurate asset reporting and unnecessary asset liquidation. Consult with a financial advisor or a bankruptcy attorney to understand the nuances of your situation and make well-informed decisions.Understanding Bankruptcy

Types of Assets You Can Keep After Filing Bankruptcy

Concept of Exempt and Non-exempt Assets

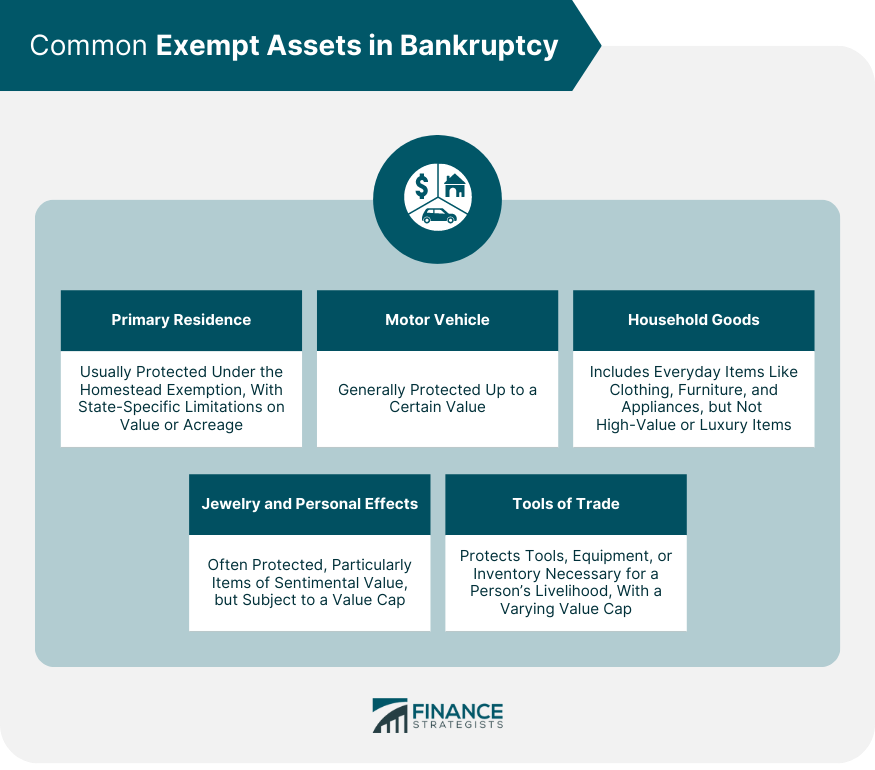

Common Exempt Assets in Bankruptcy

Homestead Exemption: Primary Residence

Motor Vehicle Exemption

Household Goods and Furnishings

Jewelry and Personal Effects

Tools of Trade

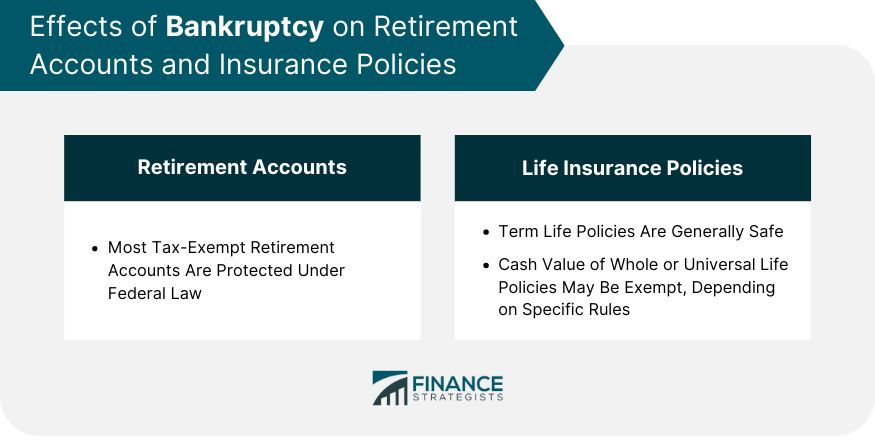

How Bankruptcy Affects Retirement Accounts and Insurance Policies

Federal Protection for Retirement Accounts

Life Insurance Policies: Cash Value and Term Policies

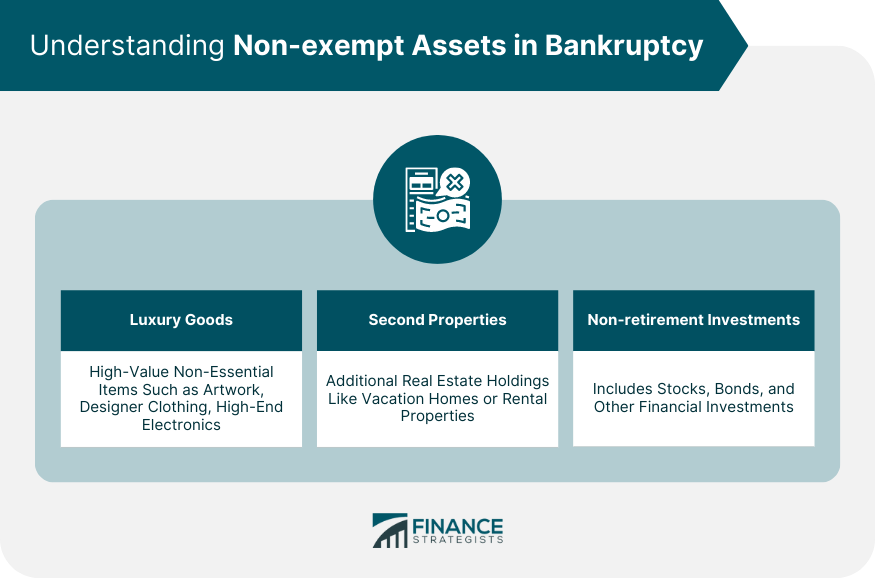

Understanding Non-exempt Assets in Bankruptcy

Luxury Goods

Second Properties

Stocks, Bonds, and Non-retirement Investments

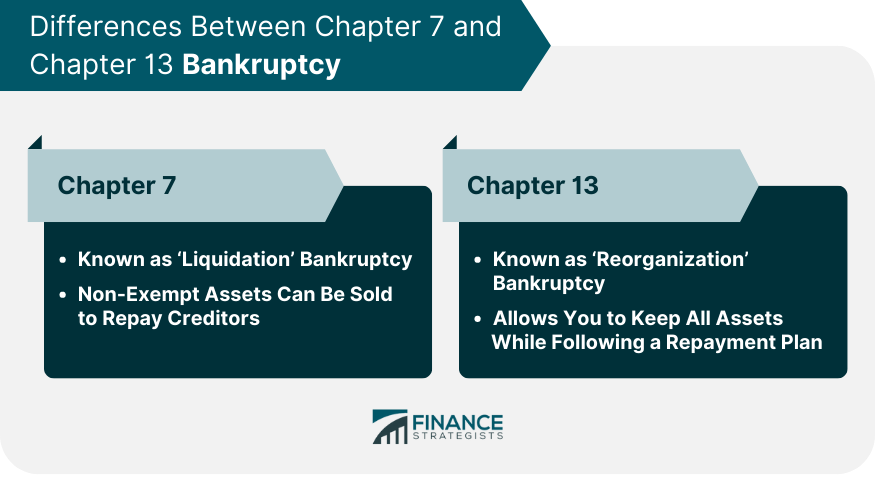

Differences Between Chapter 7 and Chapter 13 Bankruptcy

Chapter 7 Bankruptcy

Chapter 13 Bankruptcy

How Exemptions Vary by State

Federal vs State Exemptions

Understanding State's Specific Exemption Laws

Role of the Bankruptcy Trustee

Duties and Responsibilities of a Bankruptcy Trustee

Interaction Between the Trustee and Your Assets

Strategies to Protect Assets

Consult With a Bankruptcy Attorney

Time Bankruptcy Filing

Convert Non-exempt Assets Into Exempt Assets

Common Mistakes to Avoid When Filing Bankruptcy

Inaccurate Asset Reporting

Unnecessary Asset Liquidation

Bottom Line

What Can You Keep After Filing Bankruptcy? FAQs

You can typically keep exempt assets like your primary residence, car, household items, personal effects, retirement accounts, and certain insurance policies.

Exempt assets are protected by law from seizure in bankruptcy, ensuring you aren't left destitute. Non-exempt assets can be liquidated to repay your debts.

In Chapter 7 bankruptcy, non-exempt assets can be sold to repay creditors, while in Chapter 13, you can keep all assets while following a repayment plan.

Yes, bankruptcy exemptions can significantly vary by state. Some states allow you to choose between federal and state exemptions.

Avoid inaccuracies in asset reporting and unnecessary asset liquidation. Both can lead to adverse outcomes. It's advisable to consult with a bankruptcy attorney.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.