Offshore banking refers to the practice of keeping money in a bank located outside one's home country. These banks are often situated in jurisdictions that offer particular financial advantages, such as enhanced privacy, tax incentives, protection from local economic or political instability, or better interest rates. The primary objective of offshore banking is asset protection and financial diversification. In regions undergoing political turmoil or economic uncertainty, offshore banks present a sanctuary for one's assets, isolating them from local disruptions. Moreover, many people leverage offshore accounts to optimize their tax liabilities legally, given the favorable tax treatments provided by some offshore jurisdictions. Additionally, offshore banks can offer financial privacy, though this has been tempered in recent years by international regulations and agreements aimed at countering money laundering and tax evasion. Opening an offshore bank account might seem like a daunting task, replete with endless paperwork and legal hoops. However, while the process requires due diligence, it's more straightforward than many anticipate. The first step in the process isn't about the bank but rather where the bank is located. Here's what you need to consider: Political and Economic Stability: The stability of a country can significantly influence your decision. After all, the primary purpose of offshore banking for many is to ensure their assets are safe. Countries with a track record of political and economic stability are often the preferred choices. Regulatory Environment: Different countries have varied regulations concerning offshore banking. Some might offer significant tax advantages but might also have stringent compliance requirements to prevent money laundering or other illicit activities. Understanding these regulations and ensuring compliance is crucial. Banking Facilities: Not all offshore banking jurisdictions offer the same facilities. Some might have a robust digital banking infrastructure, while others might be better suited for businesses rather than individual accounts. Your needs should dictate your choice. Once you've chosen a jurisdiction, the next step is selecting the right bank. Here's how to approach this: Reputation: A bank's reputation isn't just about its name or size. Investigate its history, see how it fared during economic downturns, and check if it has been involved in any controversies or legal tussles. Services Offered: Offshore banks often provide a range of services, from personal and business accounts to investment and wealth management services. Ensure the bank you're considering offers the services you require. Customer Reviews: While official documentation will provide a bank's formal stance, customer reviews can give insights into actual user experiences. Look out for feedback on customer service, ease of transaction, and other real-world user concerns. Proper documentation ensures smooth transactions, legal compliance, and secure banking: Personal Identification: Just like with domestic banks, offshore banks need to verify your identity. This will usually involve submitting a passport copy, a driver's license, or other government-issued IDs. Proof of Address: This could be a recent utility bill, a lease agreement, or any official document showing your current residential address. Bank Reference: Many offshore banks require a reference from your current bank to vouch for your credibility. This document should ideally state the duration of your association with the bank and confirm you as a client in good standing. When you operate an offshore bank account, you're venturing into an international realm of banking. Here's what to expect: Checks: Offshore banks usually provide checkbooks, allowing you to make payments in the currency of the account. But remember, cashing or depositing these checks abroad can sometimes attract higher fees or longer clearing times than domestic checks. Debit/Credit Cards: These can be used globally. They might come with benefits tailored for international travelers or business persons, like competitive foreign exchange rates or fewer foreign transaction fees. Online Banking: Offshore banks typically offer state-of-the-art online banking platforms. These allow for international wire transfers, viewing of real-time account balances, and management of multiple currency accounts. It's crucial to ensure that their online platforms use strong encryption and security measures to protect your financial data. Fees and Transfer Speeds: Given their international nature, transaction fees can sometimes be higher, especially for wire transfers or currency conversions. However, many offshore banks provide faster international transfer services compared to standard banks, especially if transferring between branches of the same bank. Multi-Currency Operations: This can be advantageous for those dealing with international business or investments, as it allows for efficient currency management and potential hedging against currency fluctuations. Offshore banking has long been associated with discretion: Legacy of Privacy: Historically, many sought offshore accounts because of the high degree of confidentiality they offered. Certain jurisdictions became renowned for ensuring the utmost secrecy, making it nearly impossible for third parties to access account details. Changing Landscape: In recent years, international initiatives, like the Common Reporting Standard (CRS), have sought to bring transparency to the global financial system. As a result, many offshore jurisdictions have begun sharing financial data with foreign tax authorities, especially concerning significant account holders or large transactions. Consent and Data Sharing: While data sharing has become more common, many offshore banks still require explicit consent from account holders before releasing information unless mandated by international agreements. Navigating the regulatory landscape of offshore banking: Robust Regulations: Offshore jurisdictions aim to protect their reputation and prevent illicit activities, ensuring that the banks within their territories adhere to international standards. Documentation and Due Diligence: Offshore banks often have rigorous know-your-customer (KYC) processes. Prospective account holders must provide detailed documentation about their financial standing, source of funds, and business operations, if applicable. Monitoring and Reporting: Banks continuously monitor transactions to identify suspicious activities. Large transactions, or those that seem irregular, might require additional documentation or justification to ensure compliance with anti-money laundering (AML) norms. Global Initiatives: This might include adhering to the standards set by bodies like the Financial Action Task Force (FATF) or participating in information exchange mechanisms under the CRS. Designed specifically for individuals, personal banking services in offshore jurisdictions provide a suite of offerings tailored to meet diverse financial needs and goals. Savings Accounts: Offshore banks provide savings accounts where individuals can deposit funds and earn interest. These accounts may come with benefits like higher interest rates or accounts in multiple currencies. Credit Cards: Offshore credit cards might offer unique perks, especially tailored for international travel or purchases. They might also offer competitive currency conversion rates, making them favorable for use in multiple countries. Fixed Deposits: For those looking for more stable returns, offshore fixed deposits or term deposits might be an attractive option. Depending on the jurisdiction, these might offer better interest rates than those in the individual's home country. Loans: Offshore banks also provide personal loan facilities, though the terms and conditions might vary from those offered by domestic banks. It's essential to understand the interest rates, repayment terms, and any associated fees. Offshore corporate banking services cater to the diverse needs of businesses operating internationally. Business Accounts: These are foundational for companies operating abroad. They enable easy international transactions, payroll processing for overseas employees, and efficient cash flow management. Trade Finance: For businesses engaged in international trade, offshore banks provide services like letters of credit, bill discounting, and export and import financing. This ensures smooth trade operations and financial stability. Merchant Banking: Especially relevant for larger corporations or those in the e-commerce sector, merchant banking services facilitate large-scale, complex transactions and offer tailored financial solutions. Taking advantage of the distinctive advantages offered by offshore jurisdictions, these services aim to enhance the wealth of individuals or corporations. Fund Management: Many offshore banks have dedicated teams to manage investment funds. These could be mutual funds, hedge funds, or other types of pooled investment vehicles, potentially offering diversified portfolios. Brokerage Services: For those looking to invest in international stock markets or commodities, offshore banks often offer brokerage services. This provides investors with a platform to buy and sell assets. Investment Advisory: Beyond transactional services, offshore banks often have teams of investment advisors. They offer bespoke advice, taking into account the investor's risk appetite, financial goals, and market conditions. Offshore trust and estate planning services are sought after for asset protection and succession planning. Asset Protection: Offshore trusts can be a powerful tool in protecting assets from creditors, lawsuits, or other financial threats. By transferring assets to a trust in a stable jurisdiction, owners can ensure their wealth remains safeguarded. Estate Planning: For high-net-worth individuals concerned about the transfer of their wealth, offshore trusts and estate planning services offer structured solutions. This can lead to minimizing estate or inheritance taxes and ensuring that assets are distributed as per the individual's wishes. Beneficiary Provisions: Offshore banks, through their trust services, can also ensure that specific provisions are made for beneficiaries, be it education, healthcare, or other financial needs. This structured approach ensures that wealth benefits future generations in an intended manner. Offshore banking allows individuals and businesses to manage their assets in banks outside their home country, capitalizing on benefits like enhanced privacy, tax incentives, and potential protection from local instabilities. The primary intent behind such banking is the protection and diversification of assets. While the idea might seem complex, the process, from selecting the right jurisdiction and bank to the actual operation of the account, is more straightforward with proper guidance. Jurisdictions are chosen based on stability, regulatory environment, and the banking facilities they offer. However, it's vital to recognize the evolving nature of offshore banking, especially regarding confidentiality amidst international regulations. Moreover, the variety of services - from personal and corporate banking to investment and estate planning - emphasizes the versatility and depth of offshore banking, tailored to meet diverse financial objectives.What Is Offshore Banking?

How Offshore Banking Works

Opening an Offshore Bank Account

Choose a Jurisdiction

Select a Bank

Complete Documentation

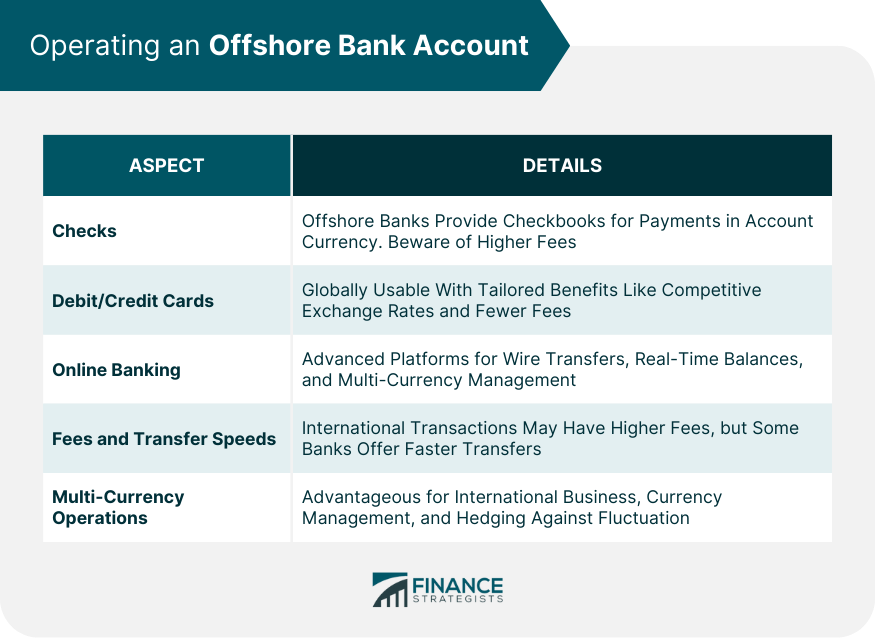

Operating an Offshore Bank Account

Confidentiality and Privacy Measures

Regulatory Framework and Compliance

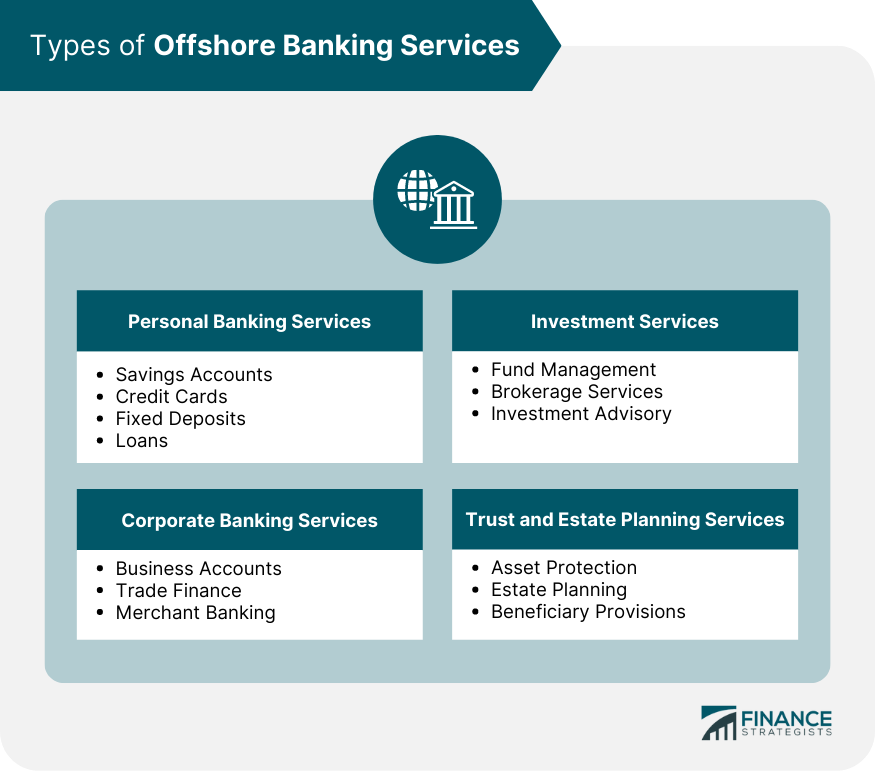

Types of Offshore Banking Services

Personal Banking Services

Corporate Banking Services

Investment Services

Trust and Estate Planning Services

Conclusion

How Does Offshore Banking Work? FAQs

Offshore banking refers to the practice of keeping money in a bank located outside one's home country.

Choosing a jurisdiction for offshore banking is based on factors like the country's political and economic stability, its regulatory environment, and the banking facilities it offers. It's essential to select a location that aligns with your financial goals and risk appetite.

To open an offshore bank account, one needs to select a jurisdiction, choose a reputable bank within that jurisdiction, and then complete the necessary documentation, which includes personal identification, proof of address, and possibly a reference from a current bank.

Offshore banks often offer enhanced privacy, with certain jurisdictions legally bound not to share account details without the account holder's consent. However, with global initiatives like the Common Reporting Standard, many offshore areas now share financial data with foreign tax authorities.

Yes, offshore banking jurisdictions often have strict regulatory measures to deter activities like money laundering or terrorism financing. Account holders must provide detailed documentation to demonstrate the legitimacy of their funds, and banks monitor transactions for suspicious activities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.