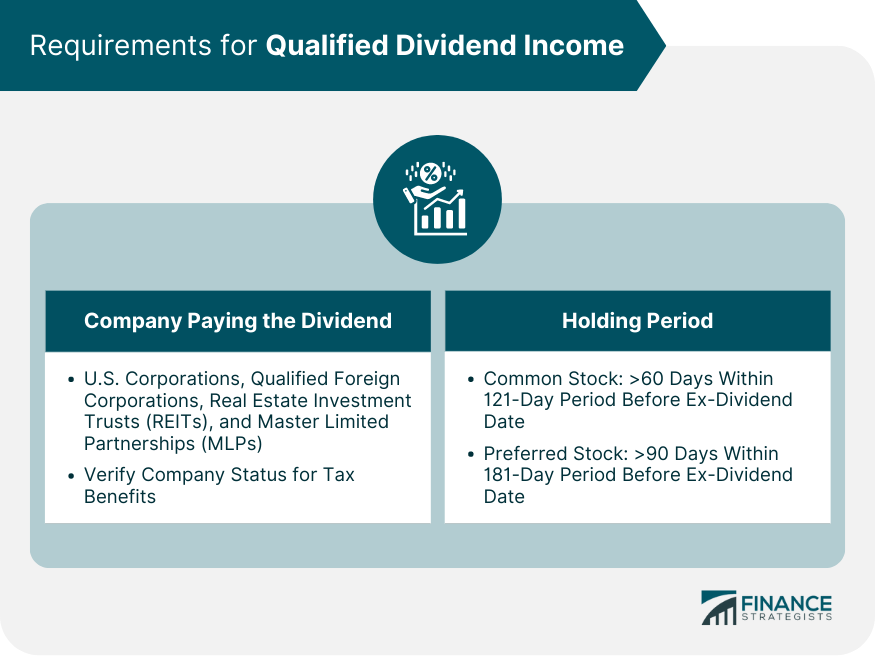

Qualified Dividend Income (QDI) refers to dividends that are received from a domestic corporation or a qualified foreign corporation and meet certain holding period requirements. These dividends are subject to a lower tax rate than ordinary income. The holding period for the dividend to be considered "qualified" is more than 60 days during the 121-day period that begins 60 days before the ex-dividend date. The ex-dividend date is the date after the dividend has been accounted for, and the stock seller will no longer receive the dividend payment. The tax rates for qualified dividends are 0%, 15%, or 20%, depending on the taxpayer's taxable income. These rates are typically lower than the rates for ordinary income. To be considered a qualified dividend, the payment must come from a U.S. corporation, a qualified foreign corporation, or certain entities such as Real Estate Investment Trusts (REITs) and Master Limited Partnerships (MLPs). Investors need to research and verify the status of the dividend-paying company to ensure they are receiving qualified dividends and enjoying the associated tax benefits. The holding period is critical for a dividend to be considered qualified. Investors must hold the underlying stock for a minimum period to benefit from the lower tax rate on qualified dividends. For common stock, the holding period is more than 60 days within the 121-day period that begins 60 days before the ex-dividend date. For preferred stock, the holding period is more than 90 days within the 181-day period that starts 90 days before the ex-dividend date. Adhering to these holding period requirements is essential for investors seeking to maximize their tax efficiency. At the end of the tax year, investors will receive a Form 1099-DIV from their brokerage firm, which outlines their dividend income. This form separates the total ordinary dividends (Box 1a) from the qualified dividends (Box 1b), allowing investors to easily identify and report their qualified dividend income on their tax return. In addition to Form 1099-DIV, investors can review their brokerage firms' dividend statements to identify qualified dividends. Brokerage firms typically provide this information on monthly or quarterly account statements, making it simple for investors to track their annual dividend income. While ordinary income is taxed at an individual's marginal tax rate, qualified dividends are taxed at long-term capital gains rates, which are typically lower. This advantage makes qualified dividends an attractive option for investors seeking income-generating investments. Non-qualified dividends, also known as ordinary dividends, are taxed at the investor's ordinary income tax rate. This distinction can result in a significant difference in an investor's tax liability, making it essential for individuals to understand the tax treatment of their dividend income. Investors can maximize their after-tax returns by investing in companies that pay qualified dividends. While focusing on qualified dividend income can be a beneficial strategy for investors, it is essential to concentrate on something other than dividend-paying stocks. Diversifying a portfolio with a mix of investment types, including growth stocks, bonds, and other income-producing assets, can help mitigate risks and provide a more balanced approach to investing. Dividend policies can be subject to change based on a company's financial health and other factors. T herefore, investors relying on qualified dividend income should regularly monitor their dividend-paying stocks to ensure they still provide the expected income and tax benefits. The performance of dividend-paying stocks and the amount of qualified dividend income they generate can be influenced by broader economic conditions and interest rate fluctuations. During periods of economic downturn or rising interest rates, companies may reduce or eliminate dividend payments, which can impact investors' income streams. Tax laws and regulations are subject to change, and any alterations to the preferential tax treatment of qualified dividends could impact investors' tax liabilities and overall returns. Staying informed about potential tax law changes and adjusting investment strategies accordingly can help investors maintain tax efficiency and protect their portfolios. Investors should diversify their portfolios across different industries and sectors to maximize qualified dividend income. Doing so can reduce their exposure to specific market risks while taking advantage of a broad range of dividend-paying companies. Dividend reinvestment plans (DRIPs) allow investors to maximize their qualified dividend income. By automatically reinvesting dividends into additional shares of the same stock, investors can benefit from the power of compounding, potentially increasing their future dividend income and overall returns. Investors should maintain long-term holding periods for their dividend-paying stocks to take advantage of the lower tax rates on qualified dividends. This strategy ensures that the dividends are qualified and promotes a long-term investment mindset, which can lead to better overall returns. Investing in dividend-paying stocks within tax-advantaged retirement accounts, such as Traditional IRAs, Roth IRAs, and 401(k)s, can further enhance the tax efficiency of qualified dividend income. By deferring taxes on the growth and income generated within these accounts, investors can potentially maximize their overall returns and enjoy a more comfortable retirement. Qualified Dividend Income offers investors the advantage of lower tax rates on dividends received from eligible corporations. To ensure dividends qualify, investors must meet specific requirements, including the company paying the dividend being a U.S. or qualified foreign corporation and adhering to the prescribed holding periods for common and preferred stocks. By accurately identifying and reporting qualified dividend income, investors can benefit from the tax advantages and potentially maximize their returns. However, it is important to consider potential risks associated with relying solely on dividend-paying stocks and the fluctuating dividend policies of companies. Economic conditions, interest rate fluctuations, and potential tax law changes can also impact qualified dividend rates and overall returns. Mitigating these risks can be achieved through diversification, long-term holding strategies, and tax-efficient investing in retirement accounts. By adopting these approaches and staying informed, investors can optimize their tax efficiency, protect their portfolios, and potentially enhance their qualified dividend income.What Is a Qualified Dividend Income?

Requirements for Qualified Dividend Income

Company Paying the Dividend

Holding Period

Identifying Qualified Dividend Income

Form 1099-DIV

Dividend Statements From Brokerage Firms

Tax Advantages of Qualified Dividend Income

Lower Tax Rates Compared to Ordinary Income

Comparison to Non-Qualified Dividends

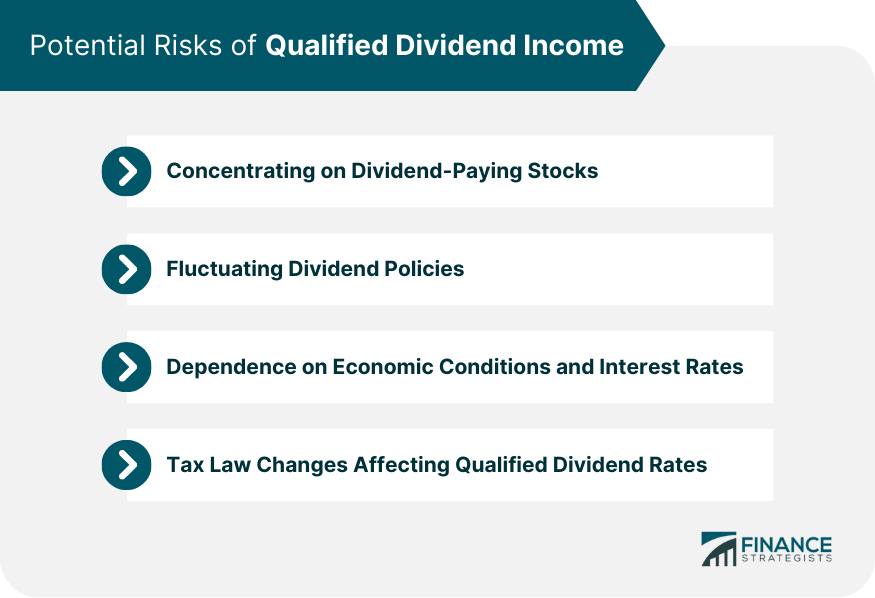

Potential Risks of Qualified Dividend Income

Concentrating on Dividend-Paying Stocks

Fluctuating Dividend Policies

Dependence on Economic Conditions and Interest Rates

Tax Law Changes Affecting Qualified Dividend Rates

Strategies for Maximizing Qualified Dividend Income

Diversification Across Industries and Sectors

Utilizing Dividend Reinvestment Plans (DRIPs)

Focusing on Long-Term Holding Periods

Tax-Efficient Investing in Retirement Accounts

Conclusion

Qualified Dividend Income FAQs

Qualified Dividend Income (QDI) refers to dividends received from shares in a U.S. corporation or a qualified foreign corporation that meet certain holding period requirements. These dividends are taxed at a lower rate than ordinary income.

Qualified Dividend Income is taxed at long-term capital gains rates, which are typically lower than ordinary income tax rates. The rates are 0%, 15%, or 20%, depending on your taxable income.

A U.S. corporation or a qualified foreign corporation must pay a dividend to be considered Qualified Dividend Income. The shares must be held for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

Qualified Dividend Income is reported on Form 1099-DIV provided by the payer of the dividends. This information is then reported on your federal tax return, typically on Schedule B (Form 1040) and Line 3a of Form 1040.

Yes, Qualified Dividend Income, like other types of income, can affect your eligibility for certain tax credits or deductions. For example, it can increase your Adjusted Gross Income (AGI), which could phase out certain deductions or credits. Always consult with a tax professional to understand the specific impacts on your tax situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.