Capital gains tax on inherited property is the tax paid on the profit made from selling the property that you've inherited. The tax isn't on the entire sale amount, but on the difference between the sale price and the property's stepped-up basis - its fair market value at the time of the original owner's death. This means if the property has appreciated over time, the stepped-up basis could significantly lower your capital gains tax. However, the rate of tax varies depending on whether the gain is short or long-term, and your tax bracket. Understanding these rules can help navigate potential tax implications, and professional advice may be beneficial in complex situations. The stepped-up basis is a crucial tax concept for inherited property. It refers to adjusting the value, or 'basis', of an asset to its fair market value at the time of the previous owner's death. This adjustment can significantly reduce potential capital gains taxes if the property has appreciated in value over time. Determining the cost basis of an inherited property involves establishing its fair market value at the time of the original owner's death. This valuation can be complex and might require professional assistance, such as an appraiser. Establishing the fair market value requires an appraisal. The appraised value at the time of the previous owner's death becomes the property's cost basis. If the property is sold for more than this amount, the difference is the capital gain. When calculating capital gains, it's essential to account for property improvements and selling expenses. Improvements made to the property, such as renovations, increase the cost basis. Selling expenses, such as realtor fees, decrease the realized gain. Once you've established the cost basis and accounted for improvements and selling expenses, you can calculate the capital gain or loss. If the property is sold for more than the cost basis, the difference is the capital gain and may be subject to tax. There are exceptions and exclusions to capital gains tax that can affect how inherited property is taxed. A surviving spouse often receives special tax treatment. They typically inherit the deceased spouse's property on a stepped-up basis, potentially reducing or eliminating capital gains tax if the property is sold. The primary residence exclusion allows individuals to exclude up to $250,000 (or $500,000 for married couples) of capital gains on the sale of their primary residence. This exclusion can also apply to inherited property if certain conditions are met. Trusts and estates often have special rules. For instance, property held in a trust may have a different cost basis calculation, while estate tax might be relevant for larger estates. One of the simplest ways to reduce capital gains tax is by holding onto your investments for more than one year. Long-term capital gains tax rates are usually lower than short-term rates, which apply to assets held for less than a year. Thus, holding investments longer can result in significant tax savings. Investing through tax-advantaged accounts like IRAs or 401(k)s can also provide tax savings. These accounts often offer tax-free growth or tax-free withdrawals in retirement, helping to minimize capital gains tax. This strategy, also known as tax-loss harvesting, involves selling securities at a loss to offset capital gains from other investments. It's important to be aware of the 'wash-sale rule,' which disallows a tax deduction for a security sold at a loss and re-purchased within 30 days. Gifting assets to family members in a lower tax bracket, or leaving assets to your heirs (who will receive a stepped-up basis), can also be a useful strategy to minimize capital gains tax. It’s crucial to understand the rules and potential implications of gifting and inheritance. For real estate investments, the IRS allows a significant exclusion on capital gains from the sale of a primary residence. Navigating the complexities of capital gains tax on the inherited property can be challenging. Professional help can be invaluable. Consulting a tax advisor is especially helpful when dealing with complex situations, such as large estates or properties with significant appreciation. Estate planners can provide strategic advice on reducing capital gains tax, such as setting up trusts or planning for the timing of property transfers. Real estate agents can provide insights on market trends and selling strategies, while appraisers can help determine the fair market value of the property. Capital gains tax on inherited property is assessed on the profit gained from the sale, with the property's stepped-up basis—its value at the time of the original owner's death—playing a significant role. Key elements in calculating the tax include establishing the property's fair market value, accounting for improvements and selling expenses, and determining the final capital gain or loss. Certain exceptions like those for spouses and primary residences can lower tax obligations. Also, strategies like proper estate planning and careful timing of the sale can help minimize capital gains tax. Staying informed about tax law changes is also essential to manage potential future impacts. Lastly, consulting professionals like tax advisors, estate planners, and real estate professionals can be instrumental in navigating this complex field effectively.Capital Gains Tax on Inherited Property Overview

Concept of Stepped-up Basis

Determining the Cost Basis of Inherited Property

Calculation of Capital Gains Tax on Inherited Property

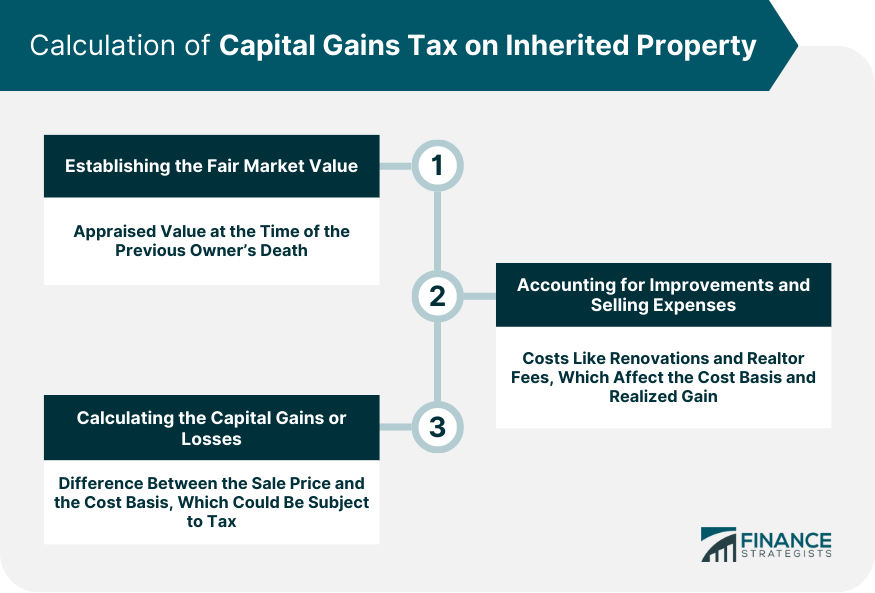

Establishing the Fair Market Value

Accounting for Improvements and Selling Expenses

Calculating the Capital Gains or Losses

Exceptions and Exclusions to Capital Gains Tax on Inherited Property

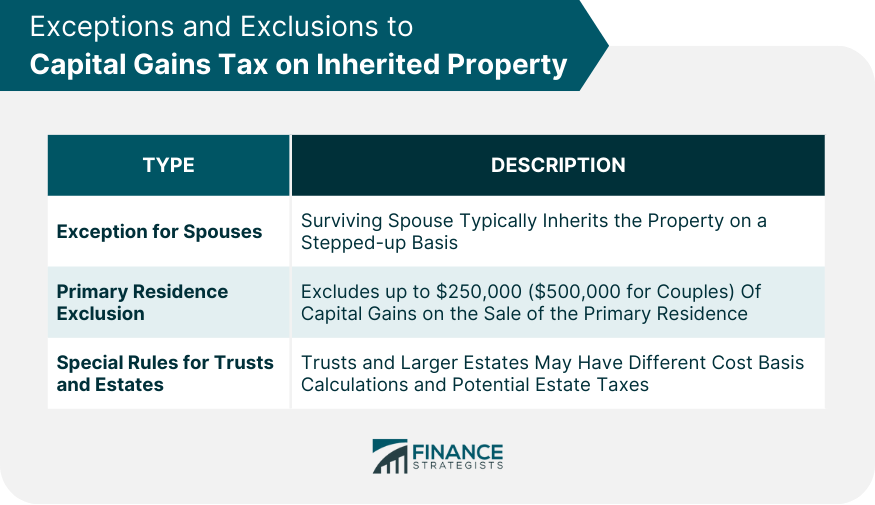

Exception for Spouses

Primary Residence Exclusion

Special Rules for Trusts and Estates

Strategies to Minimize Capital Gains Tax

Hold Investments Longer

Utilize Tax-Advantaged Accounts

Offset Capital Gains With Capital Losses

Gift and Inheritances

Real Estate Exemptions

Professional Help for Capital Gains Tax on Inherited Property

When to Consult a Tax Advisor

How Estate Planners Can Help

Utilizing Real Estate Agents and Appraisers

Conclusion

Capital Gains Tax on Inherited Property FAQs

The capital gains tax rate on an inherited property depends on whether the gain is long-term or short-term and the seller's tax bracket. Long-term capital gains tax rates range from 0% to 20%, while short-term gains are taxed as ordinary income.

The stepped-up basis refers to the revaluation of an inherited property's cost basis to its fair market value at the time of the original owner's death. This can significantly reduce the capital gains tax if the property has appreciated over time because any gain is calculated from this updated value, not the original purchase price.

There are exceptions and strategies that may help reduce or avoid capital gains tax on inherited property. For example, a surviving spouse often inherits the property on a stepped-up basis. There's also a primary residence exclusion, which can exclude a certain amount of gain if the property was your main home. Additionally, capital losses from other assets can offset capital gains.

Estate planning can include strategies to minimize potential capital gains tax on inherited property. This could involve setting up trusts, gifting property before death, or other plans designed to mitigate potential tax impacts.

It's advisable to seek professional advice if you're dealing with a complex situation like a large estate, significant property appreciation, or if you're unsure about how to calculate potential capital gains. Tax advisors, estate planners, and real estate professionals can all provide valuable assistance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.